Luxury Shifts From Flash to Quiet Value as Craftsmanship Takes Center Stage

The luxury market's top 2% of customers now account for half of all global spending, as craftsmanship and longevity replace logo-chasing across every tier.

The numbers are in, and they tell a story that anyone paying attention already knew was coming. After a year of creative resets, pricing recalibration, and operational discipline, the global luxury business, which barely managed to hold its ground by the ends of its well-manicured nails in 2025, is on track to show growth. But the shape of that growth matters as much as the headline figure, and it tells you everything about where fashion is actually headed.

The Market Has Stopped Pretending

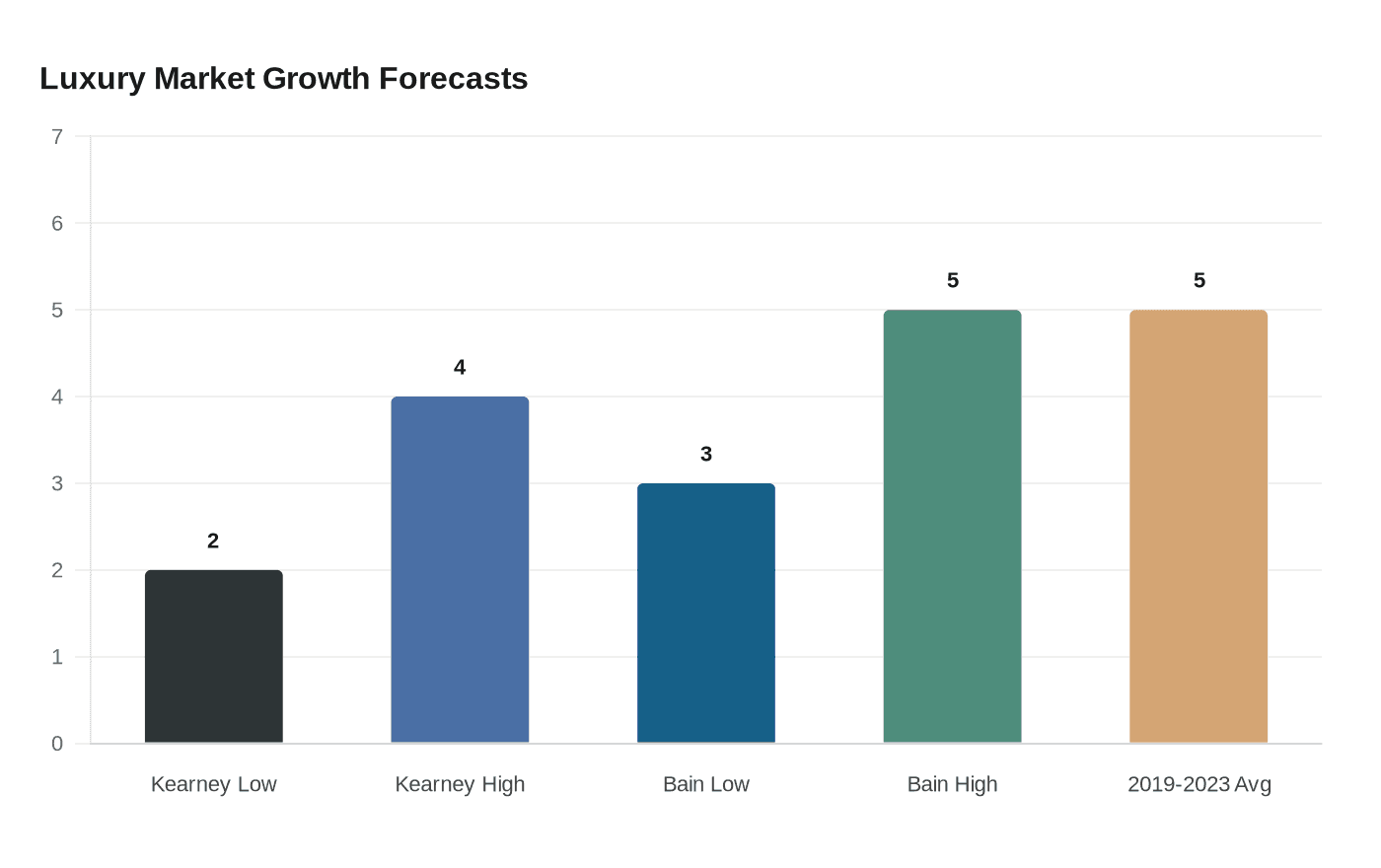

After years of aggressive price increases, creative upheaval, and a consumer base that has been quietly editing its spending, the global luxury market is finally finding its footing. That's the central finding of Kearney's 2026 Global Luxury Industry Outlook, which forecasts 2% to 4% growth for the year. That's a more conservative call than some rivals: Kearney's estimate sits slightly below Bain & Company's projection of 3% to 5% growth this year. The gap matters less than what's driving it. The sector grew at an average annual rate of about 5% between 2019 and 2023, before declining in 2024 and remaining flat in 2025. The era of posting double-digit growth on the back of price hikes alone is over.

Nora Kleinewillinghoefer, Kearney's global lead for fashion and luxury, frames it plainly: "Luxury isn't entering a downturn. It's entering a normalization phase. The brands that will win in 2026 won't rely on scale or price increases alone; they'll earn relevance through creativity, clearer value, and deeper consumer engagement."

Craftsmanship Over Clout

This is the sentence that should be pinned above every buying desk and design studio right now: for these buyers, luxury doesn't mean price point, brand name, and trendiness as much as it means superior execution, materials, and longevity. The Kearney report found that consumers are abandoning brand loyalty in favor of researching the quality of an item's manufacturing, meaning understanding the craftsmanship that goes into what they buy, and even the sourcing of the materials.

This isn't a niche behavior. What the report found was shifts in consumer buying habits towards durability and quality craftsmanship over trend. On the runway side, brands are listening: recent runway shows are featuring more essential pieces focused on customer interest in craftsmanship and long-term wearability, revealing that labels are paying attention to the shifting interests of their customers.

McKinsey's State of Fashion 2026 report reinforces the same signal. Among high-net-worth individuals, higher product quality and craftsmanship and better in-store service are among the top factors that would encourage them to buy more from luxury brands in the year ahead. The luxury slowdown is prompting a phase of strategic renewal, with brands reducing their reliance on price-led growth and refocusing on creativity and craftsmanship to rebuild client trust.

Three Buyers, Not One

The old model of a single luxury consumer archetype is dead. Katie Thomas, lead of the Kearney Consumer Institute, puts it directly: "There isn't just one stereotypical luxury consumer. Our research identified three discrete profiles: aspirational consumers who selectively participate in the category, selective splurgers who balance restraint with continued engagement, and traditionalists, who spend freely and live a full luxury lifestyle. But the market continues to fragment spend across categories, from traditional luxury houses to wellness and food and beverage."

The spending concentration tells the starkest story: the top 2% of luxury customers account for half of all global spending. Younger consumers remain active in the category but are increasingly purchasing through resale channels. As Thomas notes, Gen Z "has the least amount of money — it's not atypical to want more affordable things until you have the money to buy the nicer thing." What's notable is that younger consumers aren't abandoning luxury brands entirely — they're finding them on the resale market. After all, a Chanel bag on The RealReal is still a Chanel bag.

The Old Money Aesthetic Finds Its Moment

As trend saturation and logo-heavy branding lose their appeal, quiet luxury fashion has emerged as a defining force shaping luxury fashion 2026, rooted in refinement rather than recognition, emphasizing craftsmanship, restraint, and longevity over visibility. This is the runway confirmation of what Kearney is quantifying in spreadsheets. Quiet luxury refers to a design philosophy that prioritizes subtlety, premium materials, and expert construction without overt branding; unlike traditional luxury, which often relies on logos or bold identifiers, quiet luxury communicates value through fabric choice, tailoring, and understated silhouette.

The brands winning this conversation right now are the ones with the deepest craft credentials. The top old money luxury brands defining timeless style in 2026 are Loro Piana, Brunello Cucinelli, Hermès, Patek Philippe, The Row, Goyard, Delvaux, Canali, Valextra, and Charvet. What unites them isn't heritage for heritage's sake but a tangible commitment to construction: in high-level circles, a loud logo is seen as a sign of "new money" insecurity. True status in 2026 is signaled by the cut of a shoulder or the quality of a stitch that only another member of the club would recognize.

The cost-per-wear calculation is driving even aspirational buyers toward this thinking. Affluent buyers now view a $5,000 Loro Piana coat as a "savings" compared to five $1,000 trend-based coats that will be dated in 12 months. That's not rationalization; it's math.

What to Wear, How to Think About It

The wardrobe shift playing out right now is concrete and specific. Wool, silk, cashmere, linen, and cotton are taking priority over synthetic materials even in casual pieces, reflecting both sustainability concerns and the superior performance of natural fibers in terms of comfort, breathability, and longevity.

In tailoring, the silhouette has evolved with precision. Tailoring remains central to 2026 style, but the silhouette has shifted from the oversized borrowed shapes of recent years toward more defined structures. Shoulders are returning, not the aggressive power shoulders of the 1980s, but gently structured shapes that create definition without feeling costume-like or restrictive. The new blazers fit cleanly through the shoulders with a slight taper at the waist, creating shape while maintaining ease of movement. Brands like The Row, Khaite, and Toteme demonstrate this evolution with blazers that feel polished and deliberate without returning to the rigid construction of traditional suiting.

In accessories, the bag conversation has moved decisively away from hype. Micro bags and nylon totes are being replaced by structured leather bags sized for actual daily use, reflecting a return to accessories as long-term investments rather than trendy additions. Brands known for leather craftsmanship, including Métier, Valextra, and legacy houses like Hermès, are gaining ground over logo-heavy options that feel more about status than substance.

The Industry's Structural Reset

The upheaval isn't only consumer-side. Kearney recorded 11 creative director changes across major luxury brands, around three times the historical average. That's not coincidence; it's course correction. As all shoppers, from high-net-worth individuals to those making entry-level luxury buys, become more critical of what their purchases are worth, company leaders are refining their value propositions: some are streamlining product assortments to reduce decision fatigue while others are emphasizing exceptional craftsmanship and heritage storytelling to reinforce exclusivity.

The era of luxury fashion shoppers is exhausted by big European luxury brands and their aggressive price hikes. Post-pandemic years have finally alienated aspirational consumers in the UK, US, and elsewhere. The space that aggressive pricing created is being filled quickly: Ralph Lauren and Burberry are winning back the trust of aspirational customers by offering better value for money.

AI is also maturing inside these companies, and not just as a marketing gimmick. The initial AI push was to start investing in AI tools and figure out what they could be used for later, but this appears to be coalescing into something more practical, as AI is finding places it can be integrated into company infrastructure, rather than the near-directionless initial push. The key guardrail, as IMD's analysis notes, is that brands must avoid "over-automation that risks eroding craftsmanship and emotional connection."

The Brands That Will Actually Win

For now, the market is stabilizing. The question for 2026, the Kearney report concludes, is which brands have used the reset to actually learn something, and which ones just waited it out.

The answer is visible in fabric weight, seam construction, and the absence of a logo. Selective splurging is the new middle: many consumers are not exiting luxury, but reallocating spend toward fewer, higher-conviction purchases. For those brands built on genuine craft, that's not a threat. It's their entire argument, finally validated by the market.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?