Why gifting stock for college can trigger surprise taxes

Gifting stock can sound smarter than writing a check, but for college money it can quietly shift a tax bill onto the student or family. Cash or a 529 contribution is often cleaner when the goal is tuition.

A grandparent sitting on a winning stock position may think they have found the perfect graduation gift: give the shares, skip the cash outlay, and help with tuition at the same time. The catch is that appreciated stock carries its built-in gain with it, so a gift that feels elegant on paper can create an unexpected tax problem for the student, the parent, or the family selling the shares later.

How the tax surprise starts

The Internal Revenue Service treats gifted appreciated property differently from cash. In most cases, the recipient takes over the donor’s basis, which means the gain inside the stock does not disappear just because the shares changed hands. If the student later sells, that built-in gain can become taxable, turning a generous graduation gift into a future tax bill.

If the stock has gone up a lot, the family may be better off selling it first, paying the tax once at the donor level, and then giving cash for tuition or other education costs.

Why college costs make this a real decision

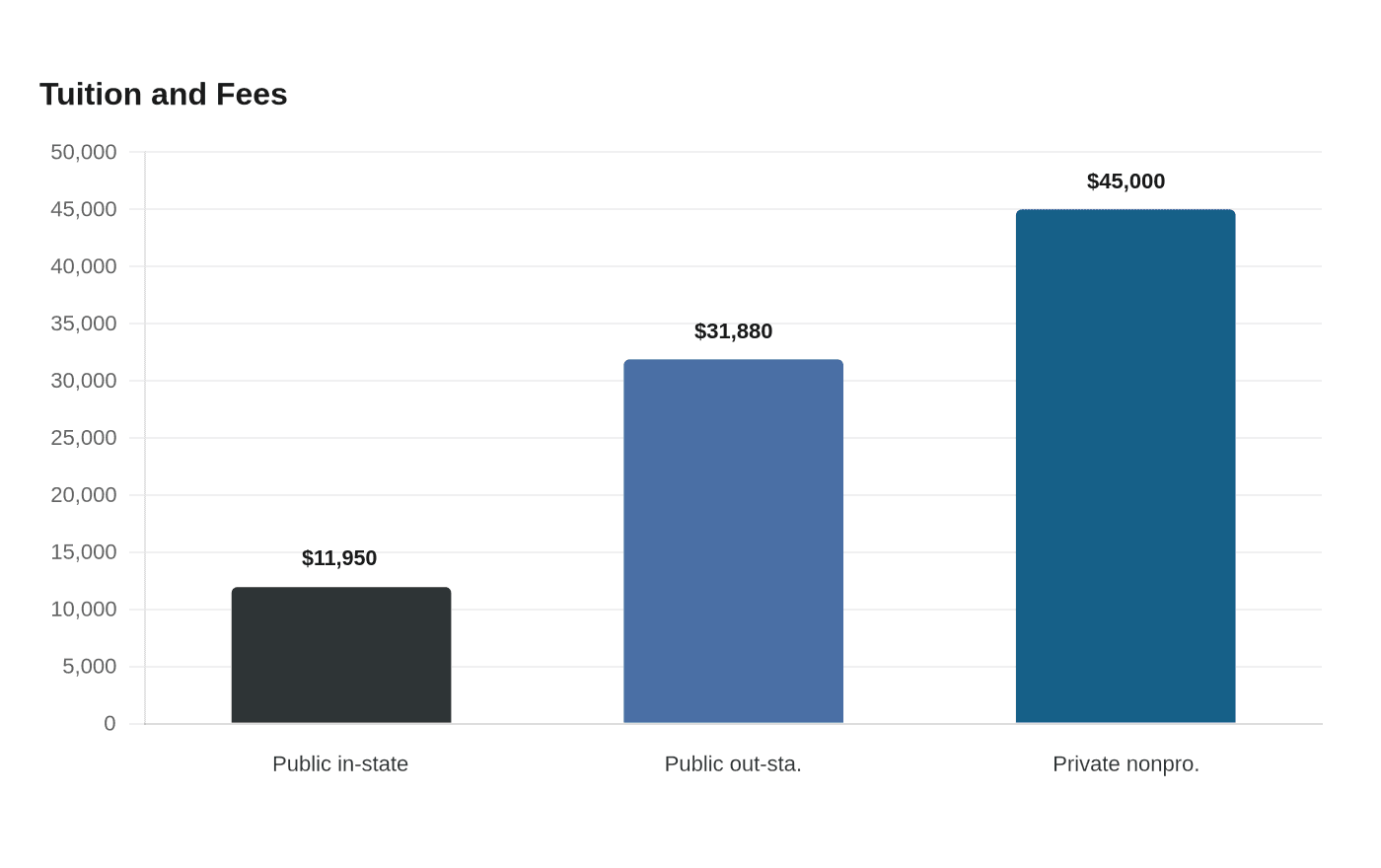

Average published tuition and fees in 2025-26 are $11,950 at public four-year in-state schools, $31,880 at public four-year out-of-state schools, and $45,000 at private nonprofit four-year schools, College Board data show. Average published tuition and fees at public four-year in-state institutions also rose by $340 from 2024-25 to 2025-26.

Total cost of attendance includes tuition and required fees, books and supplies, room, board, and other expenses. So a gift that only looks large enough to cover “college” may actually be covering just one piece of the package.

When gifting stock can make sense, and when it does not

Stock can be a smart gift when the family has already thought through who should carry the tax. The 2026 annual gift-tax exclusion is $19,000 per recipient under IRS guidance, and it applies per child, not as a single family-wide amount. The basic exclusion amount for estate and gift tax is $15 million in 2026 under the One Big Beautiful Bill Act signed July 4, 2025, so many families will never owe gift tax itself.

But gift tax is not the same as capital gains tax. A stock transfer can still leave the recipient with the embedded gain, and for a child or young adult, that can be especially awkward. A child’s unearned income above $2,700 may be subject to the kiddie tax under IRS Topic 553, which means dividends, interest, or realized gains can be taxed under rules that are different from the parent’s.

The FAFSA wrinkle most families miss

If the student is filing the FAFSA, investments are generally reported at their current market value as of the day the FAFSA is submitted. That means stock held in a student’s name can affect the aid calculation at the exact moment the form is filed.

A stock gift that sits in a student account may be less useful than cash that has already been deployed into a tuition payment or a 529 plan, especially if the goal is to avoid distorting the aid picture.

Why a 529 is often the cleaner middle ground

If the goal is college savings rather than a stock transfer for its own sake, a 529 plan is usually the more direct tool. A 529 plan is a state-maintained qualified tuition program for higher education expenses under IRS Topic 313. Qualified expenses can include tuition and other education costs, making the account a more targeted vehicle than an ordinary brokerage gift.

Families generally cannot contribute stock directly into a 529 plan. If the plan is the destination, the stock usually needs to be sold first and the cash moved into the account. That creates a chance to decide who recognizes the capital gain and whether the sale should happen in the parent’s account, the grandparent’s account, or somewhere else in the family’s tax picture.

The simplest way to decide

A good graduation gift starts with one question: who should carry the tax? If the answer is “nobody if we can help it,” then appreciated stock is often the wrong first move. If the answer is “the donor can handle the gain and we want the money to go directly toward tuition,” selling first and gifting cash is usually simpler.

- If the shares have a large embedded gain, compare the tax cost of selling first with the risk of handing the gain to the student.

- If the student may qualify for aid, remember FAFSA treats investments at current market value on the day it is filed.

- If the family wants a dedicated college bucket, selling the stock and funding a 529 is usually cleaner than transferring shares and hoping for the best.

- If the gift is meant for a child with little or no earned income, keep the $2,700 kiddie tax threshold in view.

A few practical guardrails help:

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?