The End of "Quiet" Property Gifts in India

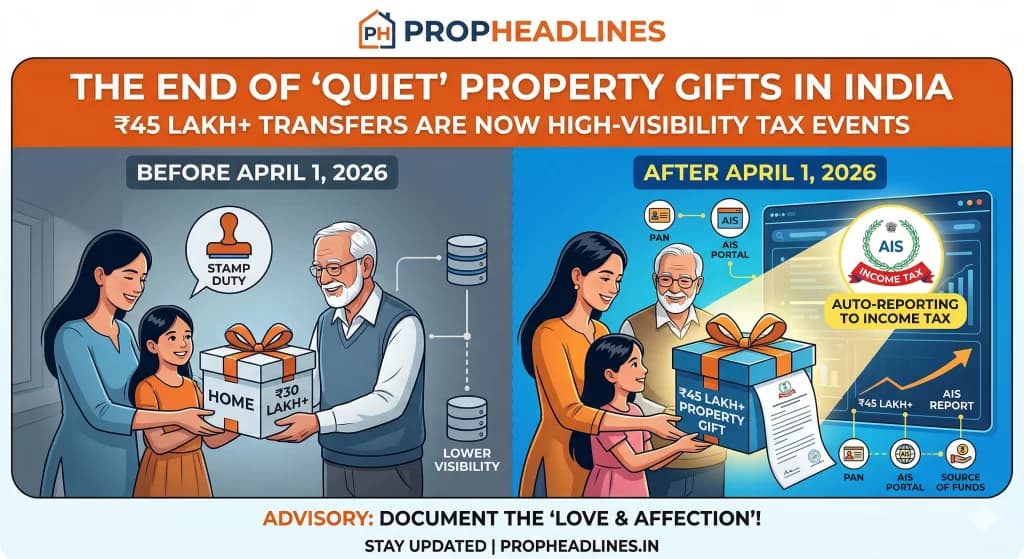

India's new Rule 237 makes every property gift above ₹45 lakh auto-visible to the tax department, ending the era of quiet family transfers.

For generations, gifting property within the family occupied a comfortable grey zone in India's tax landscape. A parent transferring a flat to a child, a grandparent signing over a plot, a spouse adding a name to a registered property: these were private acts, legally permissible, and practically invisible to the Income Tax Department unless someone went looking. Rule 237 of the newly enacted Income-tax Rules, 2026, effective from April 1, 2026, changes that calculation entirely. The era of the quiet property gift is over.

What Rule 237 Actually Does

The mechanism behind this shift is the Statement of Financial Transactions, or SFT, the reporting instrument that sub-registrars and registrars file with the tax department when high-value property transactions occur. Under the old regime, the SFT obligation was straightforward: report property sales above ₹30 lakh. Gifts were simply not on the list.

Rule 237 rewrites that mandate in two significant ways. First, it raises the reporting threshold from ₹30 lakh to ₹45 lakh. On its face, this looks like breathing room, a concession to rising property values across urban India. But the second change is where the real transformation lies: for the first time, gifts and Joint Development Agreements (JDAs) are now mandatory reporting events, sitting alongside ordinary purchases and sales.

"The reporting limit going up to ₹45 lakh might look like relief, but adding 'Gifts' to the list is the real sting," says a senior consultant at Buffet Invest. "Any gift deed with a stamp duty value of ₹45 lakh or more will now automatically populate in your Annual Information Statement (AIS). There is no hiding it anymore."

The reporting obligation falls on the Inspector-General appointed under Section 3 of the Registration Act, 1908, or the Registrar or Sub-Registrar appointed under Section 6 of that Act. In practice, the moment a gift deed is registered and its stamp duty value meets the threshold, the transaction flows directly into the recipient's AIS, visible to the department without any additional trigger.

The Urban Reality: When ₹45 Lakh Is Barely a Starting Point

The ₹45 lakh threshold sounds substantial until you look at actual market conditions. In high-value markets like Bangalore, even a 2BHK in a prime locality easily crosses the ₹45 lakh mark, turning every family transfer into a "high-visibility tax event." The same applies across Mumbai, Delhi, Hyderabad, and Pune, where residential property values have climbed steeply over the past decade. For wealthy families in these cities, virtually any meaningful property gift will now land inside the reporting window.

This is not a rule aimed at the margins. It is directed squarely at the segment of Indian property gifting that has historically involved the most value: urban real estate transferred between generations as part of inheritance planning, wealth structuring, or estate management.

The "Relative" Shield: Still Standing, But Now Under a Spotlight

One of the most important clarifications for families navigating this new landscape is that the underlying tax exemption remains intact. Transfers to "specified relatives," which include a spouse, parents, and children, remain tax-exempt under Section 56(2)(x). A parent gifting a flat to an adult child does not owe tax on that transaction simply because it is now reported.

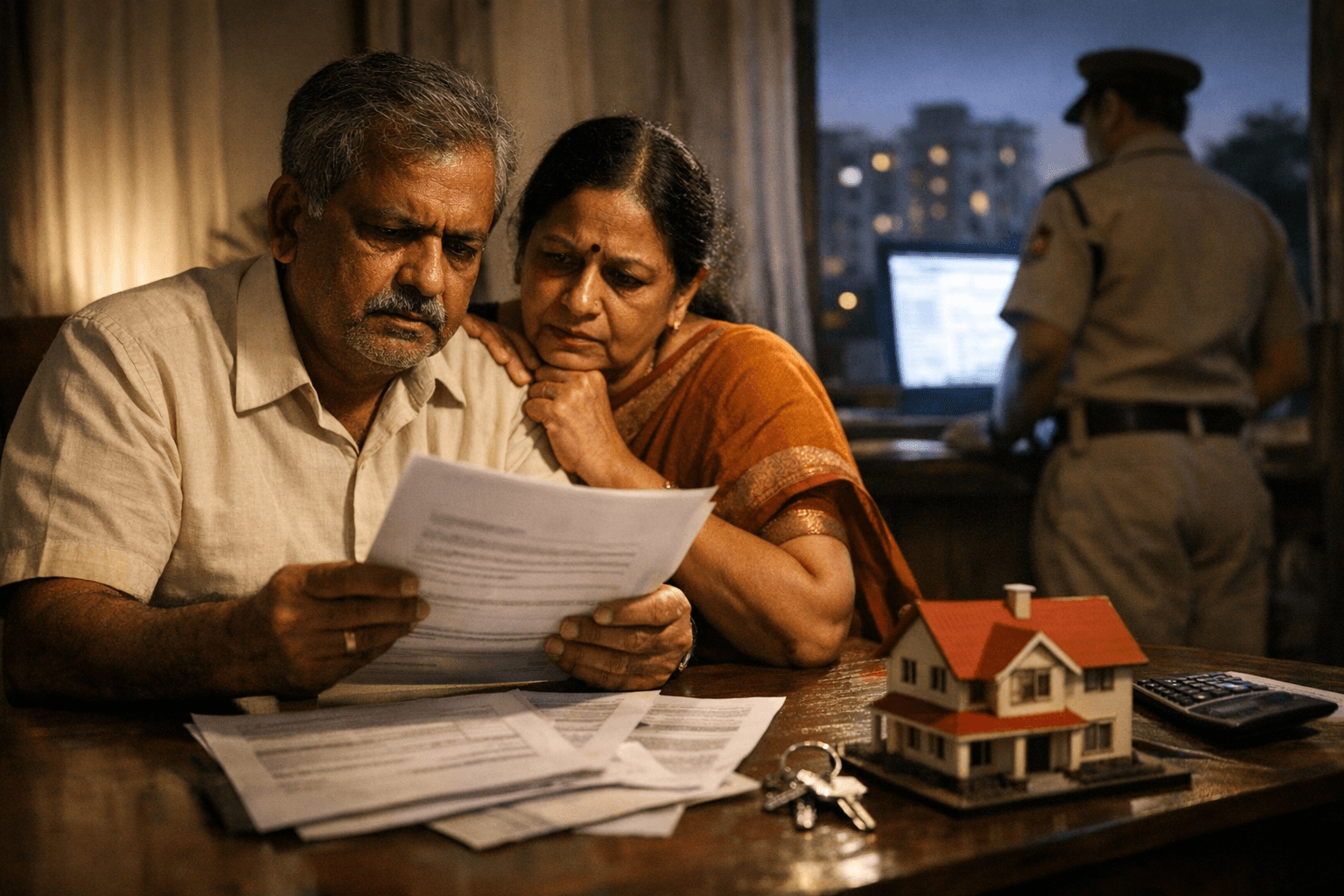

But the nature of scrutiny has changed fundamentally. Because these transfers now auto-populate in the AIS, the Income Tax Department has sight of every qualifying gift without needing to audit or investigate. The burden shifts to the taxpayer to ensure that the paper trail behind the gift is clean, consistent, and defensible. A mismatch between what the sub-registrar reports and what appears in the donor's or recipient's ITR history becomes an automated flag, not a matter of chance discovery.

The exemption is a shield, but it now needs to be actively carried, not passively assumed.

JDAs Enter the Transparency Net

Joint Development Agreements add another dimension to Rule 237's reach. A JDA is a contract between a landowner and a developer to develop a property, with the landowner contributing land and the developer contributing construction in exchange for a negotiated share of the developed units. These arrangements have been common in urban real estate for decades, often structured to manage tax timing and asset visibility.

For landowners entering into Joint Development Agreements, mandatory SFT reporting means the "possession" and "transfer of rights" are tracked from day one. This closes a gap that sophisticated property owners have used to defer or minimise the visible footprint of high-value transactions. The moment rights are transferred under a JDA and the stamp duty value meets ₹45 lakh, the transaction enters the system.

Data-driven AI tools will now flag "gift loops," which are patterns where property is moved between parties to obscure wealth. For anyone who has relied on layered or circular gifting structures to reduce taxable visibility, the compliance landscape has materially tightened.

What to Do If You Are Planning a Property Gift

The rule change does not make family property gifting inadvisable. It makes sloppy gifting inadvisable. For anyone planning a property transfer this financial year, three practices are now non-negotiable.

- Register a formal gift deed: Do not rely on oral agreements. An unregistered or informally documented gift creates gaps that the department can exploit, particularly when the AIS record and the recipient's documentation do not align.

- Verify donor capacity: Ensure the person gifting the property has filed ITRs consistent with the property's value. Investors in projects who planned to gift plots to children must ensure the donor has a clear, tax-paid trail for the original purchase.

- Monitor your AIS regularly: Ensure the value reported by the Sub-Registrar matches your own records. A discrepancy between the registered stamp duty value and your declared figures generates "Mismatch Notices" that require formal response.

The Broader Signal

Rule 237 is not an isolated amendment. It sits within a broader architecture of financial transparency that the government has been building systematically, using AIS as its central instrument. The SFT framework now links property registrars, banks, mutual fund houses, and other financial institutions into a single information ecosystem visible to the department. Property gifting is the latest category to be absorbed into that system.

For the real estate and tax planning community, the practical message is unambiguous: the era in which a property gift was a private family matter, shielded by exemptions and low administrative visibility, has ended. Compliance is no longer optional; it is automated. Families who plan their transfers carefully, with proper documentation, verified ITR histories, and formally registered deeds, will find the new rules manageable. Those who assumed that "family gift" and "tax event" were mutually exclusive categories will be finding out otherwise through their AIS inbox.

Know something we missed? Have a correction or additional information?

Submit a Tip