Coffee Prices Surge 2.48% to $293 Per Pound Amid Supply Concerns

Arabica futures bounced 2.48% to 293¢/lb on April 8, still near 90-day lows, signaling café and grocery price pressure within the next quarter.

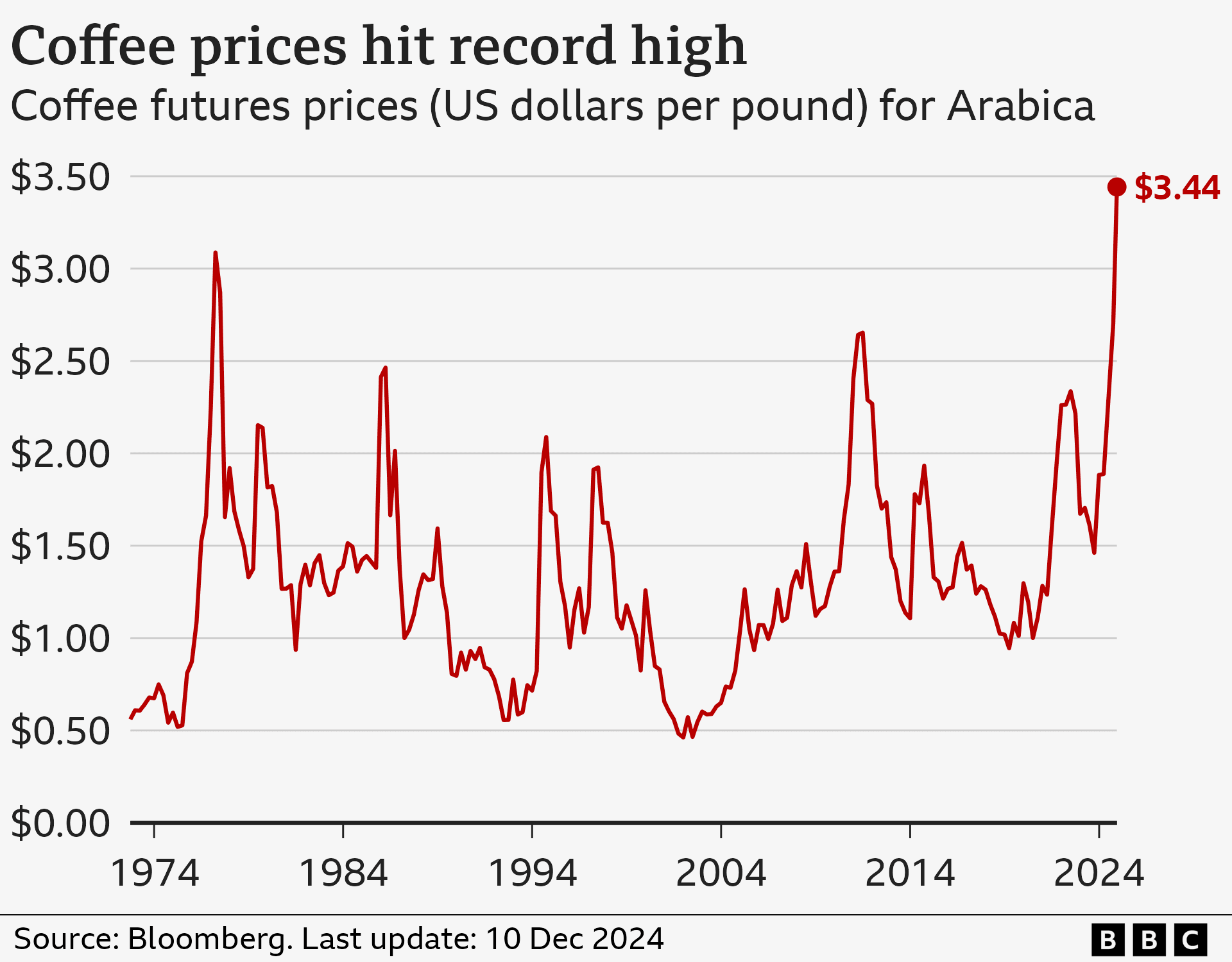

Arabica coffee futures logged a 2.48% single-session surge on April 8, pushing the benchmark to 293.18 cents per pound and snapping a slide that had shaved more than 12% off the commodity's value over the prior four weeks. That kind of two-percent-plus day is the sort of move roasters and green-bean buyers track obsessively: it's enough to shift import cost calculations for anyone carrying unhedged spot exposure, and it echoes down the supply chain to the café counter and grocery aisle within 60 to 90 days.

The 30/90-day range puts Wednesday's print in sharp relief. Over the past four weeks alone, coffee lost 12.31%. Zoom out to three months and the picture gets wilder: arabica futures had surged toward and above $4 per pound when additional U.S. tariffs on Colombian coffee triggered a breakout to new highs, before collapsing after signs of tariff relief emerged. The 90-day low sat at roughly 286 cents, reached the session immediately before the April 8 bounce. A swing from above 400 cents to 286 cents inside a single quarter is not a market making orderly price discovery; it is one reacting to geopolitical shock as much as crop fundamentals.

The proximate catalyst for the earlier collapse was diplomatic. Arabica futures on the ICE exchange fell more than 6% intraday and closed nearly 2% lower at around $3.60 per pound after the U.S. removed tariffs on Brazilian coffee following a meeting between President Trump and Brazilian President Lula. The April 8 rebound suggests the market is already second-guessing whether that relief holds, or responding to fresh origin signals.

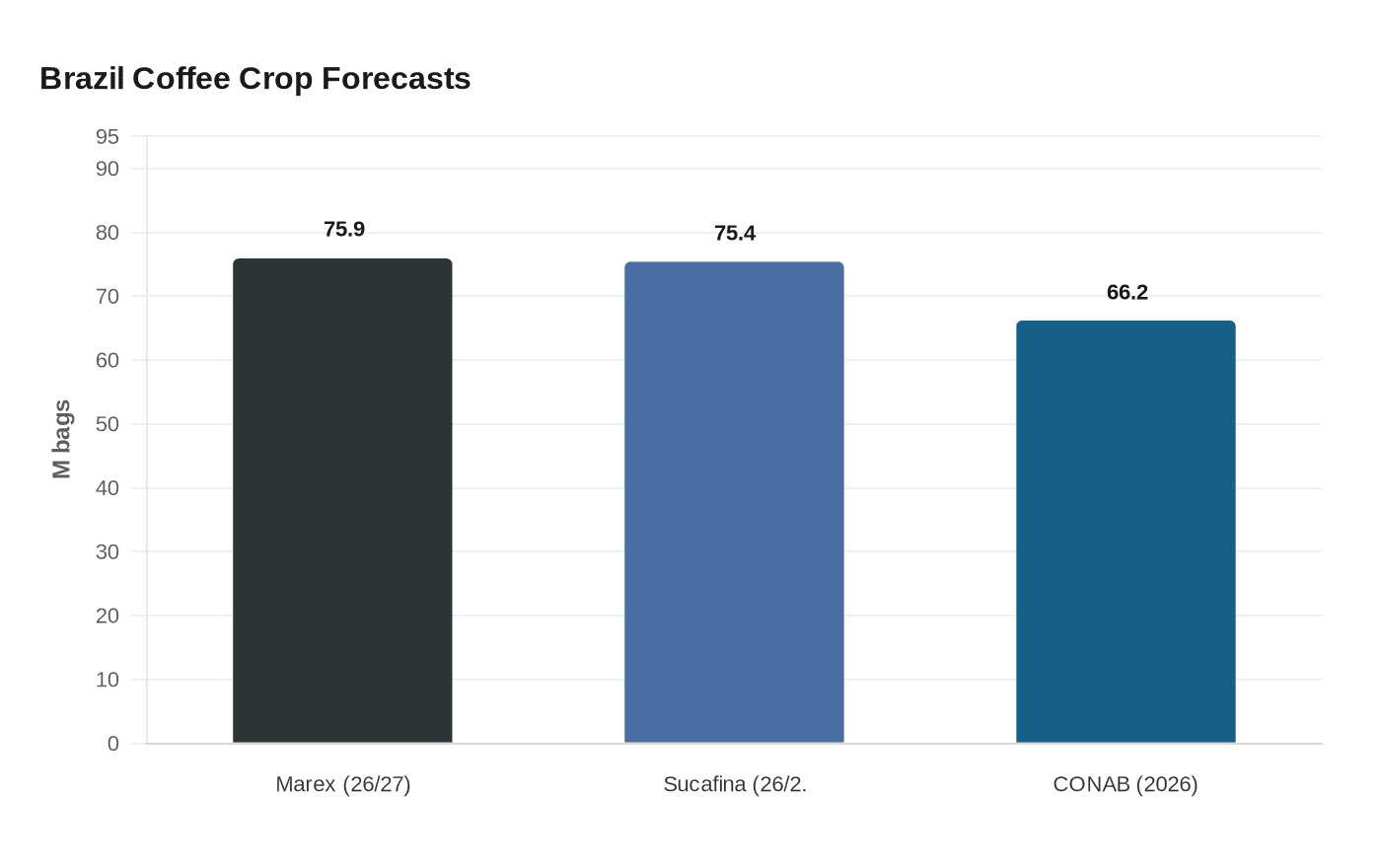

On March 19, Marex Group projected a record 2026/27 Brazilian coffee crop of 75.9 million bags, even higher than Sucafina's forecast of 75.4 million bags, a 15.5% increase year-over-year. CONAB's February data placed Brazilian 2026 production at a record 66.2 million bags, up 17.2% compared to the prior year, with arabica totaling 44.1 million bags. That supply wall has been the gravitational force pulling prices lower throughout the quarter; any weather disruption capable of threatening those estimates is the variable with the most immediate market consequence.

The key driver to watch is Brazilian weather. The Southern Hemisphere frost window opens in May and June, and any cold front threatening Minas Gerais arabica trees would be enough to reignite a sharp reversal. Brazilian real strength or weakness compounds the picture, since currency moves directly affect dollar-denominated export competitiveness and speculative positioning. Tariff policy between Washington and Brasília remains an open variable capable of overriding weather signals entirely.

For anyone standing at a café register or navigating the coffee aisle, the transmission lag is real but not long. The average cost of a regular cup of coffee rose from $3.46 to $3.57 in the year ending October 2025, and Starbucks CEO Brian Niccol acknowledged the company cannot rule out price hikes in 2026. USDA data showed prices for nonalcoholic beverages running 5.6% above year-earlier levels through February 2026, driven in significant part by elevated global coffee costs.

At 293 cents, arabica sits deep in the lower quartile of its 90-day range, which makes the bounce ambiguous: it could be a technical recovery in an ongoing downtrend, or it could be the first foothold of a sustained move back toward origin-risk pricing. The Brazilian frost season will likely deliver the answer before June does.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?