Boston Beer Posts Lower Sales, Keeps Strong Cash Position Amid Pressure

Boston Beer’s volume slipped again, but $164.1 million in cash and no debt give it room to keep pushing Samuel Adams, Twisted Tea and Sun Cruiser.

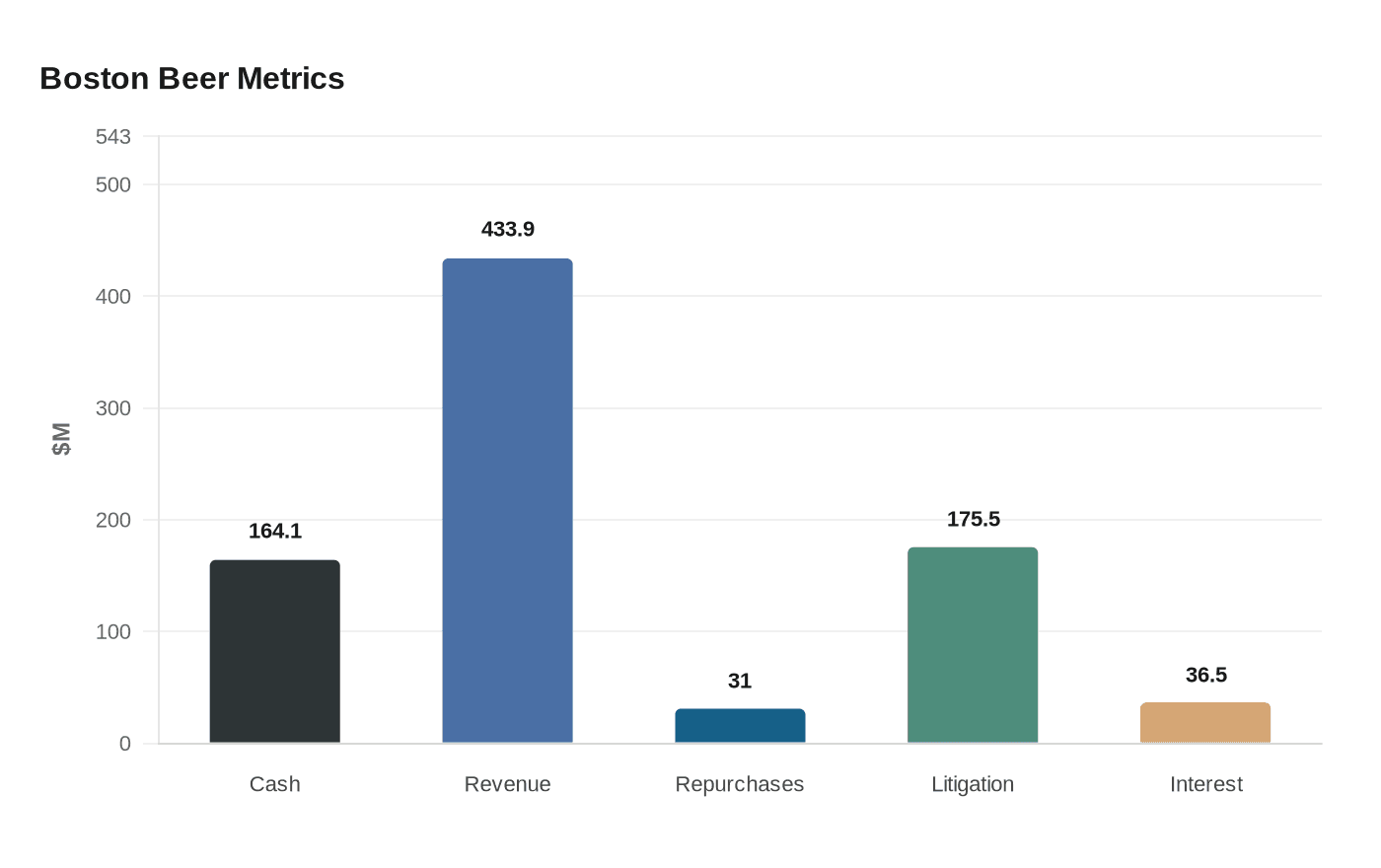

Boston Beer finished the quarter with softer sales, but the bigger story for drinkers is that the company still has plenty of room to keep backing the brands people actually buy. The Boston brewer ended Q1 2026 with $164.1 million in cash, no debt and enough balance-sheet strength to keep spending on summer support, even as shipment and depletion trends stayed under pressure.

For the quarter ended March 28, 2026, shipment volume came in at about 1.6 million barrels, down 6.9% from a year earlier. Depletions fell 4%, with declines in Twisted Tea, Truly, Samuel Adams and Hard Mountain Dew partly offset by gains in Sun Cruiser, Angry Orchard and Dogfish Head. Boston Beer said the shipment drop was also tied to tough comparisons, since distributors had built inventory for Sun Cruiser and Truly Unruly innovation in the first quarter of 2025. Distributor inventories averaged about 4.5 weeks on hand at quarter end, down from 5 weeks a year ago.

The headline revenue line was weaker too. Net revenue fell 4.4% to $433.9 million, while gross margin improved to 49.3%, up 100 basis points from the prior year. That margin gain matters because it shows Boston Beer still found some operating efficiency even while freight costs rose by $2.5 million, a reminder that logistics and inflation are still squeezing brewers even when the taproom chatter is all about shelf resets and package innovation.

The company also kept returning cash to shareholders. Boston Beer repurchased $31 million in stock between Dec. 29, 2025, and April 24, 2026, a sign management still sees value in its own shares. That kind of flexibility is unusual in a beer market where many smaller brewers are fighting just to preserve distribution and keep trucks moving.

The biggest distortion in the quarter was a non-recurring legal charge. Boston Beer recorded a pre-tax litigation expense of $175.5 million and related pre-judgment interest of $36.5 million after a verdict entered April 6, 2026. That pushed GAAP diluted loss per share to $13.88, including $15.52 per share in litigation expenses, even though non-GAAP diluted earnings per share was $1.64. Management modestly narrowed full-year guidance because of a tougher cost environment, along with tariff and commodity headwinds, while saying savings initiatives should help offset some of the pressure.

Jim Koch said the total beer and RTD category showed early signs of improvement in the quarter and estimated the category was flat in volume, versus a 4% decline for full-year 2025. He also said beyond beer outperformed traditional beer in measured off-premise channels by about 3%, with Twisted Tea and Sun Cruiser growing depletions and Angry Orchard and Dogfish Head logging four straight quarters of growth. Truly remained under pressure, while Samuel Adams and Hard Mountain Dew stayed soft. For consumers, the takeaway is straightforward: Boston Beer is still feeling the volume squeeze, but it is not acting like a brewer on the ropes.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?