January BPI Jumps 14 Points, Below-Premium Hits 50, Cautionary Outlook

January BPI jumped 14 points to 39, moving the industry from contractionary to cautionary as below-premium climbed to 50, signaling shifts in ordering and inventory decisions.

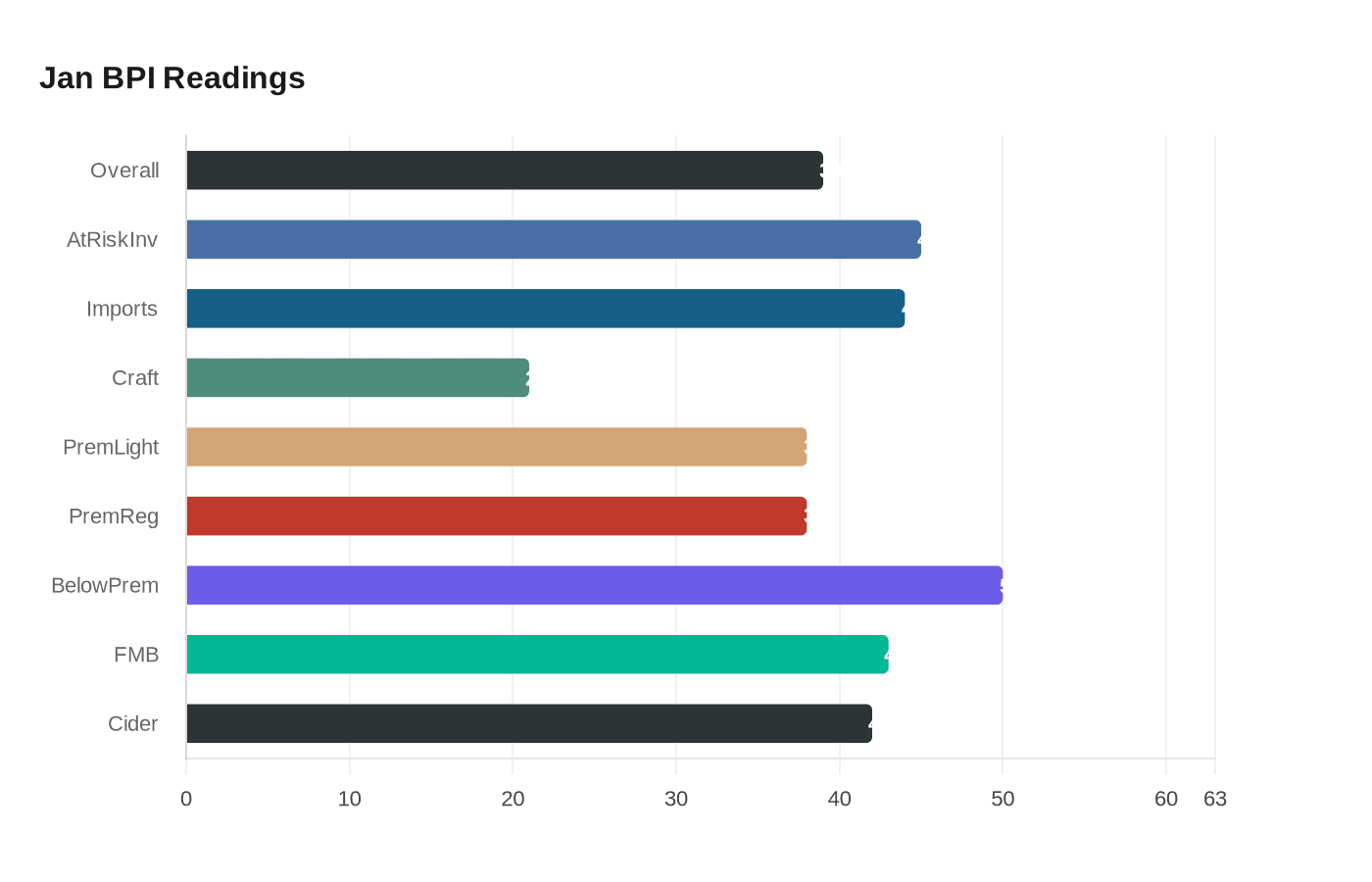

The Beer Purchasers’ Index rose sharply in January, marking the biggest month-to-month gain since last summer but still sitting below expansionary territory. The National Beer Wholesalers Association’s January BPI increased 14 points from December to 39, and combined with an at-risk inventory reading of 45, pushes the industry into a cautionary posture heading into the year.

BPI readings come from distributor purchase surveys and act as a forward-looking gauge for beer demand: readings above 50 indicate expansion and readings below 50 indicate contraction. The January uptick was broad-based; every segment posted higher month-over-month readings except cider. Notable on- and off-premise implications center on below-premium brands, which reached a BPI of 50 for the first time in over a year. That parity with the expansion threshold suggests shoppers and outlets are leaning on value-priced options more than they had through much of last year.

Segment-level detail shows mixed movement versus year-ago and month-ago baselines. Imports registered 44, down 17 points from January 2025 but up 8 points versus December 2025. Craft checked in at 21, down 5 points year-over-year but 7 points ahead of last month. Premium lights and premium regular both read 38, with each 14 points higher than December but 11 and 7 points lower than January 2025 respectively. Below premium stood at 50, 6 points below January 2025 but 10 points above December. FMB/seltzer hit 43, 3 points lower year-over-year and 12 points higher month-over-month. Cider slipped to 42, an 11-point gain from January 2025 but 2 points lower than December 2025.

For taproom operators, small breweries, and retailers, the practical signal is clear: demand pressure is easing off the depths of late 2025, but the market is not out of contraction. Monitor SKU counts and keg turns closely, prioritize rotating stock to avoid dated inventory, and stagger orders rather than chasing large replenishments. Below-premium momentum means draft lines and off-premise displays may need more shelf space for value packs and single-serve formats, while craft producers should watch wholesaler order patterns and promotional windows to protect taproom margins.

January’s movement removes some of the near-term urgency of the year-end slump but does not restore a full expansion narrative. Track the next BPI readings and at-risk inventory trends to see whether below-premium strength broadens into sustained demand or simply represents a short-term reallocation of consumer spend.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?