Taprooms and Brewpubs Help Craft Beer Defy Wider Sales Decline

Craft beer’s volume fell, but taprooms and brewpubs kept the value story alive, pushing 2024 retail sales to $28.8 billion even as production slid 3.9%.

Taprooms and brewpubs are proving that craft beer’s strongest margin may no longer sit in the package aisle. Brewers Association figures show U.S. craft brewers produced 23.1 million barrels in 2024, down 3.9% from 2023, even as retail dollar value rose 3% to an estimated $28.8 billion and employment climbed to 197,112. That split tells the story clearly: when beer is paired with food, service, and a place to stay awhile, breweries can still win even as the broader market softens.

The pressure on packaged beer was visible by mid-2025. The Brewers Association estimated craft volume was down 5% year over year, with 9,269 craft breweries operating in June 2025, down 1% from June 2024. In the association’s midyear survey, taprooms and brewpubs outperformed distribution-focused breweries by 1 to 2 percentage points in the first half of the year, while 49% of respondents reported production growth and 47% reported declines. That near-even split underscores how uneven the market has become, with one model holding steadier because it controls more of the customer experience.

Matt Gacioch of the Brewers Association said the sector’s challenges were being driven by retail and wholesale rationalization, tougher competition for limited shelf space, and consumers tightening their spending. In practice, that leaves breweries leaning hard on off-premise packages with fewer places to win and lower prices in the chain. The breweries pulling ahead are the ones turning the taproom into the main business, not the afterthought.

The full-year 2025 numbers, released in April 2026, sharpen that picture. Craft beer production fell 5.1% to 21.86 million barrels, retail dollar sales dropped 3.6% to $27.8 billion, and the sector lost about 8,000 jobs, ending at 189,000. Operating craft breweries fell to 9,578, while openings totaled 300 and closures 481, the second straight year closures outpaced openings. Even so, craft’s share of total beer retail dollar sales held at 24.6%, and volume share edged up from 13.2% to 13.3%.

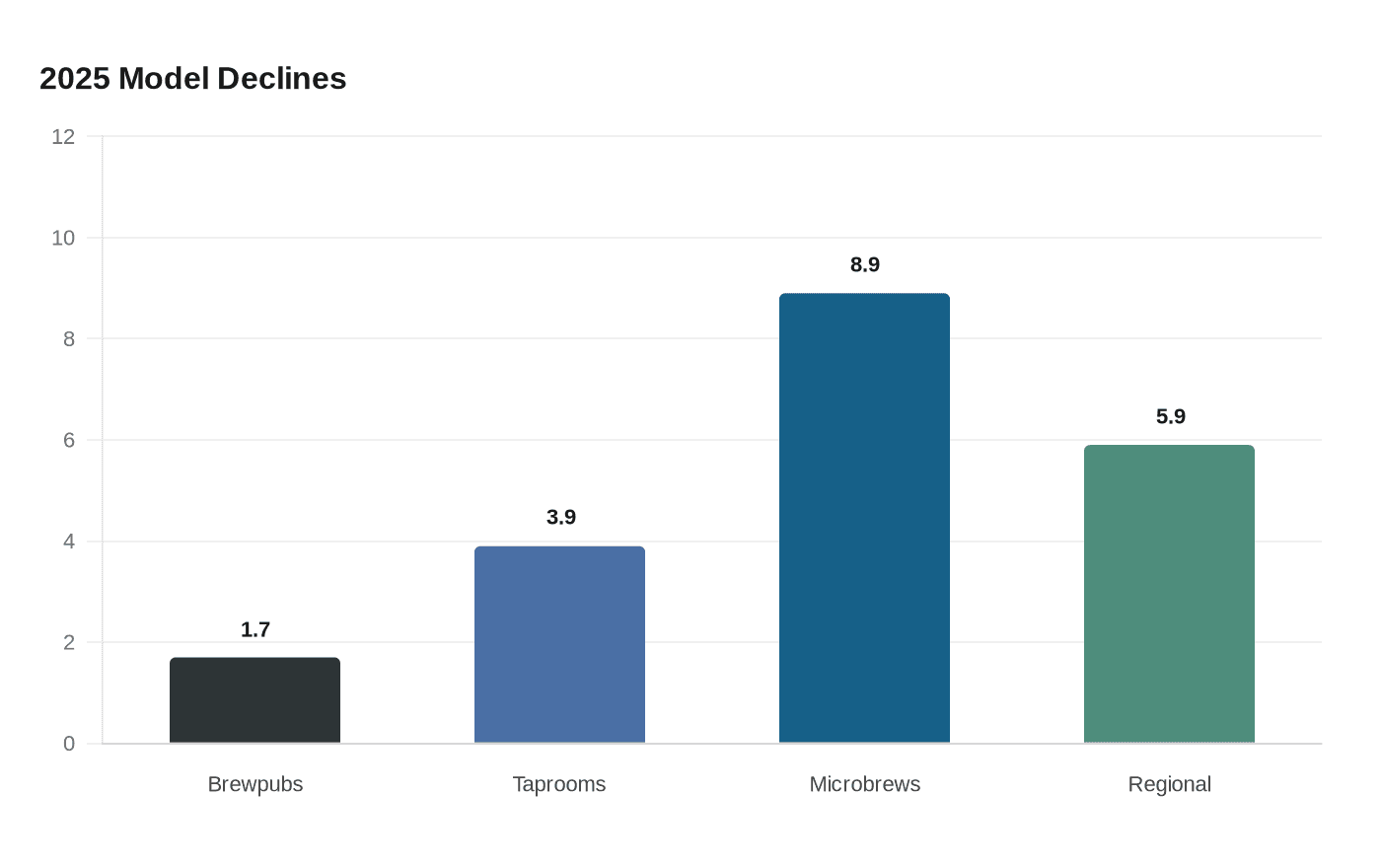

Brewpubs were the least affected business model in 2025, declining just 1.7%, compared with taprooms down 3.9%, microbreweries down 8.9%, and regional breweries down 5.9%. That is the operational lesson for the industry: the margin is shifting toward hospitality, food, and on-site reasons to visit. Beer still matters, but the breweries best positioned now are the ones that give customers a place to drink it, eat with it, and spend more time there.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?