World Nuclear Fuel Cycle Conference Highlights Strategic Shift Toward Growth

Monaco’s fuel-cycle conference turned reactor optimism into a supply-chain test. Conversion, enrichment and HALEU now look like the real gatekeepers of growth.

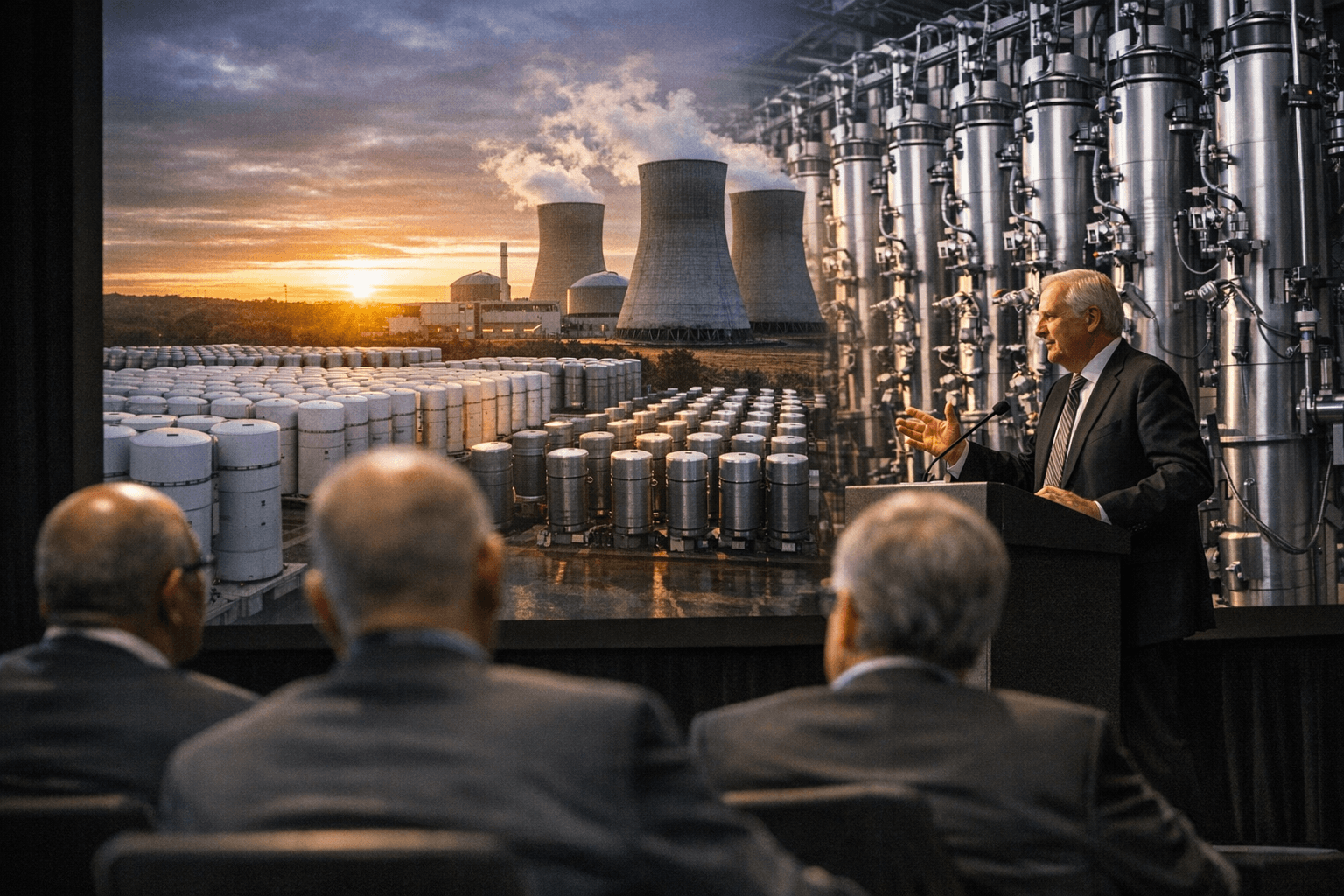

The loudest message in Monaco was not about reactor designs or ribbon-cuttings. World Nuclear Fuel Cycle 2026 opened with the industry treating the fuel cycle itself as the strategic asset, the part of nuclear that decides whether growth can actually be built, fueled and run.

Held 14-16 April at Le Méridien Beach Plaza and co-organized by the World Nuclear Association and the Nuclear Energy Institute, the conference was framed as a premier international forum for senior executives in the commercial fuel cycle. The tone matched the moment. World Nuclear News described the sector as entering a period of major change, with existing nuclear capacity now the bedrock for growth that could be unprecedented.

Sama Bilbao y León, the director general of the World Nuclear Association, put the new hierarchy plainly: “Governments all over the world recognise that energy security - and the security of fuel supplies - is more important than ever.” She also warned that much of the industry’s momentum is still only ambition, not yet executed projects. That is the difference Monaco kept returning to. The next wave of nuclear buildout will not be decided by speeches about decarbonization, but by whether mining, conversion, enrichment, fabrication, logistics and waste handling can all line up at once.

The scale of the opportunity, and the pressure behind it, is already visible. The International Energy Agency says the world had nearly 420 operating nuclear reactors at the end of 2024, 63 reactors totaling 71 GW were under construction, and 2025 is set to be a record year for nuclear generation. New units are coming online or advancing in China, India, Korea, Europe and elsewhere, but the fuel system has to keep pace if those projects are going to move from promise to power.

That is why the concrete news out of the conversion segment mattered so much. Solstice Advanced Materials said its Metropolis Works plant in Illinois is expected to produce more than 10,000 tonnes of uranium hexafluoride in 2026, about 20% above planned 2024 output. ConverDyn is also exploring a sister plant, described as Metropolis 2.0. FluxPoint Energy, meanwhile, says it is developing what it expects will be the first new uranium conversion facility in the United States in 70 years. Those are not abstract market signals. They are the industrial steps that determine whether utilities can actually secure feedstock.

The same logic runs through advanced fuel. The U.S. Department of Energy has been building a domestic HALEU supply chain through enrichment and deconversion contracts, and its HALEU Availability Program was established in 2020 to secure supplies for civilian research, demonstration and commercial use. Without that parallel buildout, advanced reactors stay mostly on paper.

Monaco’s real story was not that nuclear wants to grow. It was that the industry is now treating conversion, enrichment and fabrication as the choke points that decide whether growth becomes physical reality. The conference followed WNFC 2025, which warned of supply-demand gaps unless investment decisions came soon, and WNFC 2024, which focused on competitiveness under geopolitical strain. This year, the message sharpened: the fuel cycle is where the next phase of nuclear expansion will be won or lost.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?