Embracer Posts 26% Nine-Month Sales Drop to $1.3B, Cites Market Pressures

Embracer reported SEK 11,975m (~$1.3bn) in nine-month sales, a 26% drop year-on-year, with mobile revenue hit hard after the Easybrain divestment and a SEK 586m fall in UA spend.

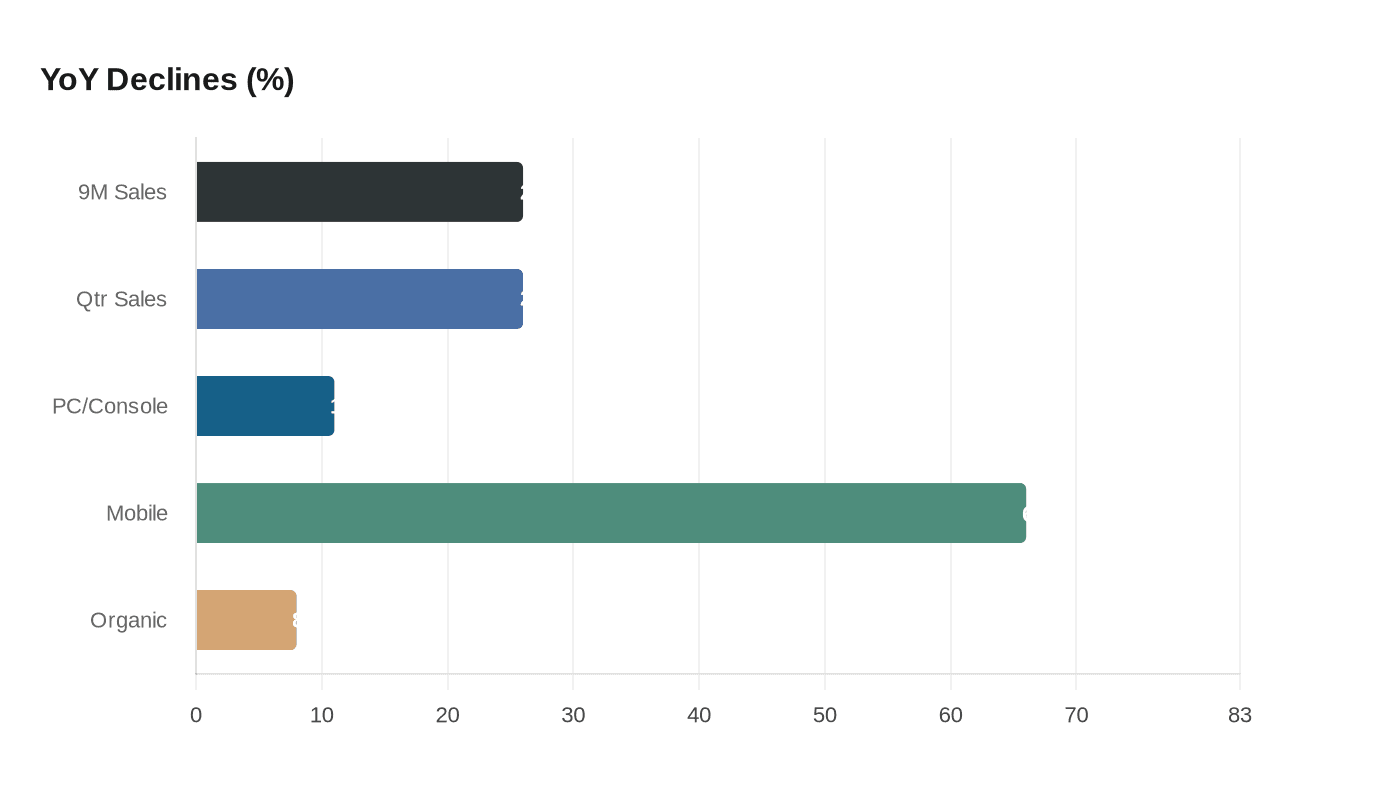

Embracer Group posted nine-month net sales of SEK 11,975 million (about $1.3 billion) for the period ending December 31, 2025, a decline of 26% year-on-year that management ties to adverse foreign exchange, negative organic growth and the divestment of mobile studio Easybrain. The company’s materials show total game development projects fell to 87 and total game developers to 4,739 for Apr–Dec 2025, underscoring a smaller development slate alongside the lower top line.

The quarter ended December 31, 2025, produced net sales of SEK 5,176 million (commonly reported as SEK 5.1 billion, about $569.2 million), down 26% year-on-year, with PC/console sales of SEK 1,900 million (down 11%) and mobile at SEK 566 million (down 66%). Embracer’s KPI table lists quarter EBIT at SEK 663 million and adjusted EBIT at SEK 528 million, with an EBIT margin of 13% and an adjusted EBIT margin of 10% for Oct–Dec 2025. CEO Phil Rogers said, "Total net sales were SEK 5.2 billion, an 8% organic drop year-over-year ... Our Adjusted EBIT was SEK 528 million."

For the nine-month period Embracer reported a small net loss of SEK 20 million, an improvement from the roughly SEK 1.5 billion loss in the corresponding period a year earlier, and an Apr–Dec 2025 EBIT of SEK 250 million versus negative SEK 1,107 million the prior year. Wnhub also reported a line showing "Net profit: SEK 477 million ($53.1 million), contrasting with a net profit of SEK 806 million ($89.9 million) from the previous year," though the Wnhub excerpt does not explicitly label which period that SEK 477 million covers.

Marketing and user-acquisition moves explain part of the shift in mix. CFO Müge Bouillon said, "total marketing spend was SEK 419 million, or 8% of net sales, down 7 points year on year, largely driven by the impact of divestments, which accounted for a five-point reduction. The non-user acquisition cost marketing of SEK 165 million decreased slightly by SEK 42 million year on year, while user acquisition cost investments dropped by SEK 586 million to SEK 254 million, driven by the Easybrain divestment. The user acquisition cost in the prior year included SEK 471 million related to Easybrain."

Embracer also disclosed strategic restructuring: management divested several non-strategic and unprofitable third-party publishing and work-for-hire businesses whose combined trailing twelve-month adjusted EBIT was around SEK -178 million, and company reporting now fully excludes Coffee Stain following its spin-out. Rogers credited core IPs and seasonal promotions for the quarter’s uplift, saying, "From a business perspective, our Q3 results were driven by our core IPs within PC/console and seasonal strength within Entertainment & Services and Mobile. Kingdom Come: Deliverance was the main driver," and noting the franchise "has now surpassed five million copies in its first year of release" after its third expansion.

Cash flow and investment lines show continued build activity: cash flow from operating activities for Apr–Dec 2025 was SEK 1,011 million while net investments in intangible assets totaled SEK 2,262 million. Rogers concluded by flagging the pipeline and priorities, stating management is "excited by our near-term and our longer-term pipeline, with a range of major projects based on our core IPs launching over the coming 3 years" and that "Execution discipline will be critical to converting this pipeline into significantly higher profitability and cash generation.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?