Rio Tinto Diamond Unit Posts $79M 2025 EBITDA Loss Despite $332M Revenue

Rio Tinto's diamond arm posted $332 million in 2025 revenue but still logged an underlying EBITDA loss of $79 million as Diavik output surged ahead of mine closure.

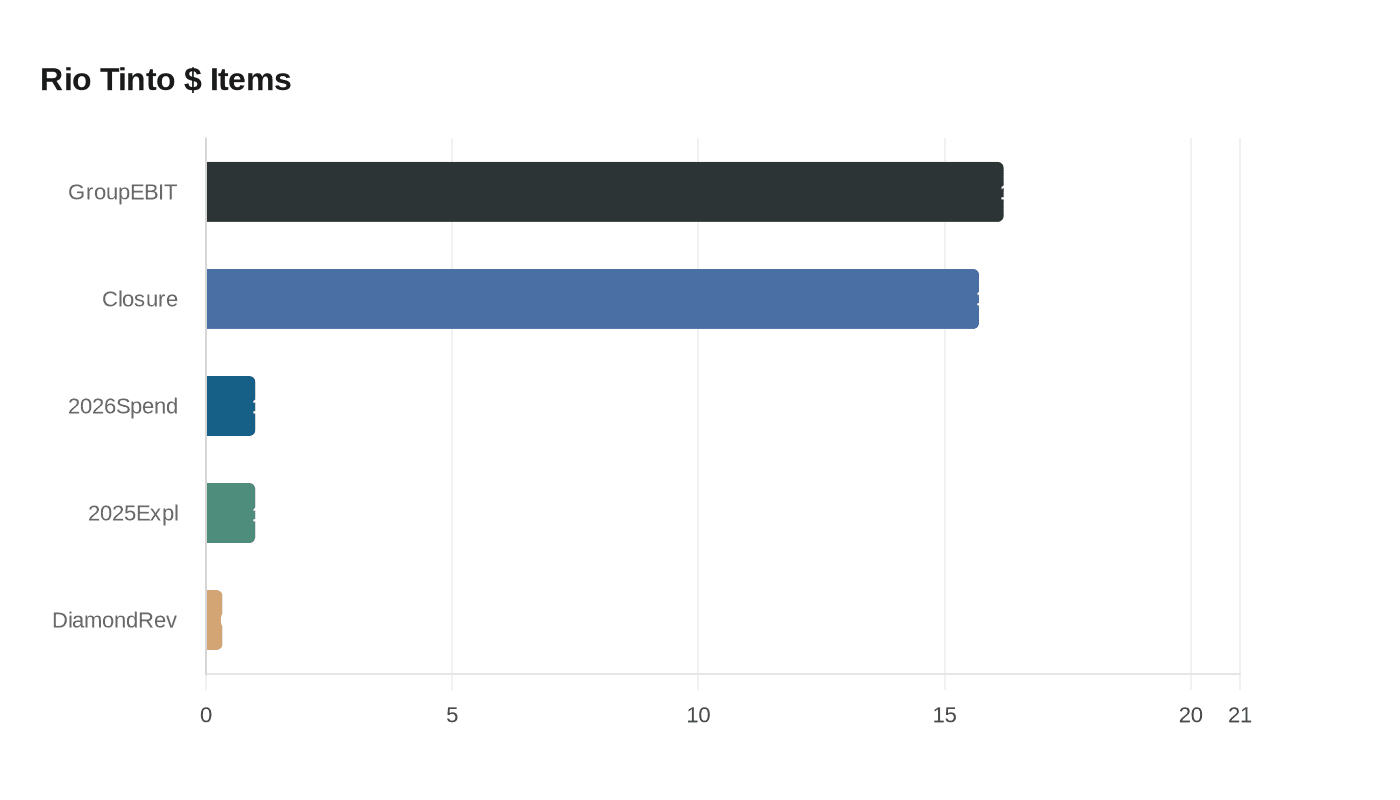

Rio Tinto's diamond unit posted $332 million of revenue for the 12 months of 2025, a 19% increase year-on-year, yet recorded an underlying EBITDA loss of $79 million, an improvement from a $115 million loss in 2024. Diamond production at the Diavik mine in Canada rose 61% to 4.4 million carats in 2025, the highest recent output as Rio Tinto mined new underground ore.

The production jump reflected mining of the A21 underground deposit, which produced more diamonds than prior zones and whose output was ramped up in the last quarter of 2024. That surge in yield helped top-line sales even as unit economics left the diamond business in the red; the A21 underground section is expected to be depleted at the end of the first quarter of 2026, at which point Diavik will reach its end of life.

Rio Tinto plans material closure activity as that life‑of‑mine timetable arrives. The company expects to spend approximately $1 billion in 2026 on closure activities related to Diavik, the Argyle diamond mine in Australia (Argyle ceased production in 2020), and "a few other projects unrelated to diamonds." Management signals that this $1 billion 2026 commitment is part of a multi‑year pattern, with ongoing closure spend expected at about $1 billion per year on a cash basis in coming years.

Corporate financial context widens the picture beyond diamonds. Group underlying EBITDA was $16.2 billion, down 19% versus 2023, with lower realised prices reducing earnings by $2.7 billion. Unit costs rose to $23.0 per tonne, $1.5 higher than 2023, and the Pilbara operations delivered an FOB EBITDA margin of 65%, down from 69% a year earlier. Rio Tinto underscored its operational priorities with the statement: "We remain focused on cost control, in particular maintaining discipline on fixed costs."

Rio Tinto's broader cost narrative also touches metals that drove group improvements and offsets. Lower operating cash unit costs benefited underlying EBITDA by $0.6 billion, helped by easing raw‑material prices for aluminium inputs such as caustic, coke and pitch and by higher bauxite volumes. Higher copper volumes cut Copper C1 net unit costs by 27%. Those gains were partially offset by slightly lower volumes in Pilbara and the Iron Ore Company of Canada, and by lower volumes in diamonds and titanium dioxide feedstocks, which the company says led to fixed cost inefficiencies.

The company has provisioned for the coming wave of closure work. "All these amounts are fully provided for within our provision for closure costs of $15.7 billion," Rio Tinto notes, while also projecting exploration and evaluation expenditure of about $1.0 billion in 2025 and signaling an effective tax rate on underlying earnings near 30% for the period. With A21 slated to be exhausted at the end of Q1 2026 and Diavik identified as the company's only remaining diamond resource, Rio Tinto is moving from a production phase that delivered 4.4 million carats in 2025 into a closure and rehabilitation phase costly enough to be covered by a multibillion‑dollar provision.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?