Seven Trends Indian Diamantaires Say Will Reshape Diamond Trade Beyond 2026

National Jeweler’s roundup finds Indian diamantaires expect tariff shifts, price volatility and stricter traceability rules to redraw sourcing and manufacturing economics beyond 2026.

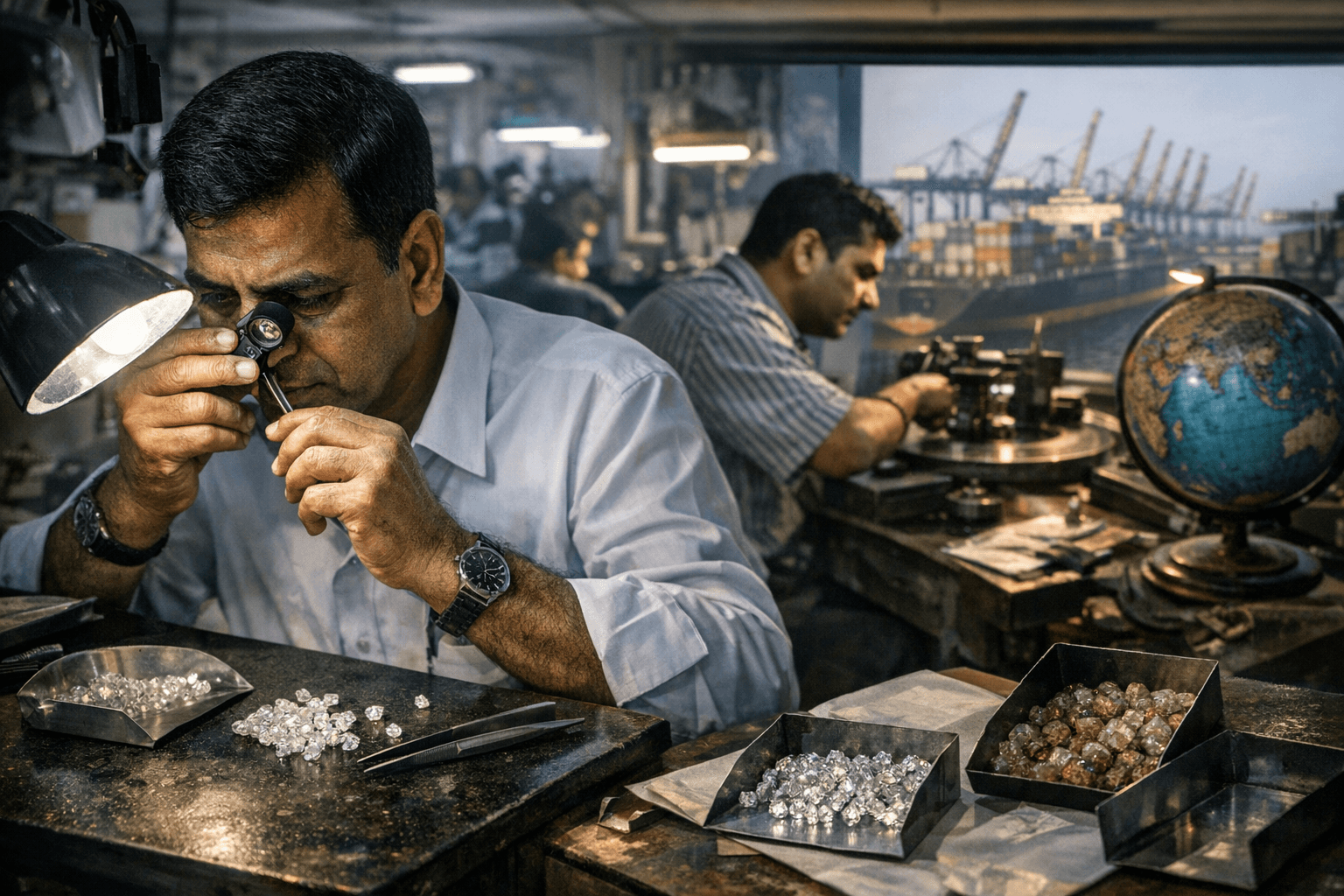

National Jeweler’s Feb. 25 roundup assembled seven trends Indian diamantaires and industry observers say will reshape how diamonds are bought, cut, sold and priced after 2026. These are not abstract forecasts but practical pressures, tariffs that change sourcing routes, price swings driven by major producers, and new compliance expectations that will alter margins and design choices for makers and retailers alike.

1. evolving tariff and trade policy will reroute sourcing and margins

Indian diamantaires flagged changing tariff regimes and trade agreements as a direct, near-term force on where rough is bought and where polishing happens. Higher or reworked duties raise landed costs for stones imported into India and can prompt companies to shift sourcing hubs, reprice contracts, or reconfigure finished‑goods routing to customer markets. For manufacturers that operate on thin polishing margins, even small tariff differentials will dictate whether a parcel is cut in Surat, Antwerp or rerouted through intermediary ports.

2. price volatility driven by producer moves and index swings

Price dynamics have turned more consequential: an early‑year surge in diamond sales by a leading producer and a simultaneous 1.3% drop in the 1‑carat Rapaport Price Index in January illustrate the double pulls diamantaires must manage. When producers increase offtake, polished prices can tighten; when price indices slide, retailers face margin compression and inventory risk. That volatility forces Indian cutters and traders to shorten inventory cycles, hedge more actively, and rework contracts to reflect daily index movements.

3. traceability and ESG requirements will become operational costs, not optional marketing

Industry observers in the roundup emphasized that traceability demands are moving from boutique marketing claims to baseline compliance. Buyers, especially international chains and high‑net‑worth clients, are requesting verifiable chains of custody, which adds tagging, reporting and sometimes third‑party audits to the cost of polishing and distribution. For diamantaires accustomed to paper invoices, that means investing in digital ledgering and supplier verification; for the consumer, it will increasingly show up as price premiums for fully traceable stones.

4. lab‑grown diamonds will force clearer product segmentation

Indian diamantaires expect the market for lab‑grown stones to accelerate, compelling manufacturers to sharpen how they position natural versus synthetic assortments. The trend is not simply substitution; it is segmentation: lab‑grown offers lower price points and different design logics, thin pavé, knife‑edge settings and fashion‑forward three‑stone pieces, while naturals will be curated toward certificate-backed, investment-grade presentations. Retailers and cutters who fail to segregate inventory, grading practices and marketing risk blurring value propositions for both categories.

5. digitization of trading platforms will shorten deal cycles and widen buyer pools

Deal sourcing is moving online in ways that change the day‑to‑day of a diamantaire: curated B2B platforms, digital tenders and instant auctions speed transactions and bring new buyers into Surat and Mumbai markets. That reduces the advantage of longstanding personal networks and raises the importance of real‑time clarity, high‑resolution imagery, consistent grading reads, and rapid logistics. Firms investing in digital storefronts and remote‑viewing capabilities are poised to win faster turnover and broader customer reach.

6. consolidation, credit pressures and changing supplier relationships

Several diamantaires cited tighter access to working capital and a wave of consolidation among mid‑sized cutters as a structural shift. As banks and trade financiers apply stricter risk criteria, smaller polishing units face pressure to join larger groups or specialize in niche services, precision cutting of melee, for example, rather than compete on general inventories. For buyers and designers, this means negotiating with fewer, larger suppliers but also gaining steadier compliance and capacity at scale.

7. automation and skills reshaping India’s polishing advantage

The final trend is a technological and human one: automation is raising yield per worker on repetitive tasks, while complex cuts and bespoke commissions still demand trained hands. Indian centers will bifurcate, highly automated lines for standardized melee and simple solitaires, and boutique ateliers preserving artisanal expertise for branded, designer and investment pieces. That split will influence what stones are economical to cut in India and which are more profitable to send to specialty workshops abroad.

These seven trends, compiled from the perspectives of Indian diamantaires and industry observers, together sketch a trade in transition: more regulated, faster, and more segmented. The practical consequence is clear for anyone who designs, buys or sells diamonds, supply lines, pricing mechanics and the skills that create value are all being retooled beyond 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?