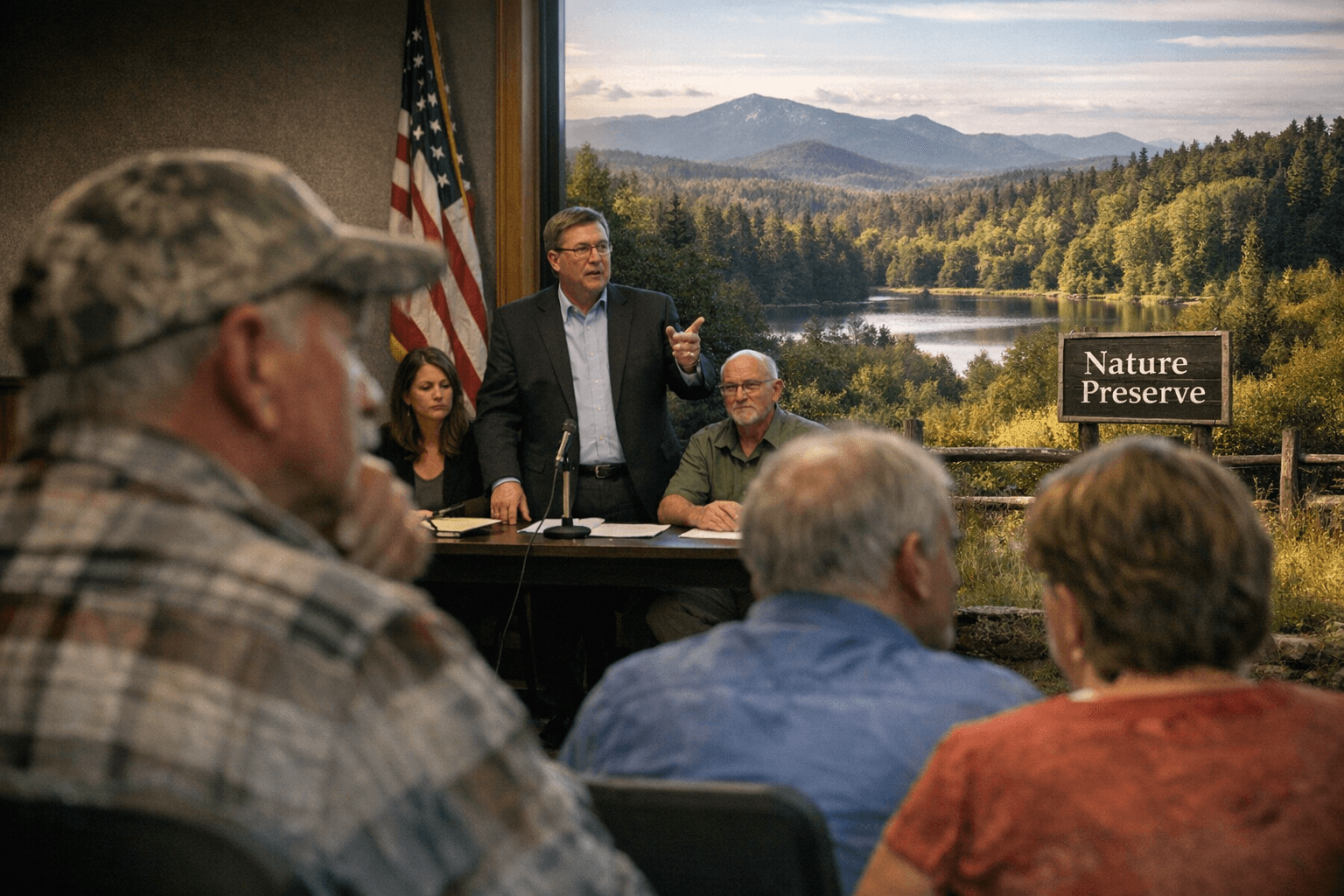

Local Debate Over Tax-Exempt Land Holdings Raises Budget Questions

A local columnist argued that large national land-conservation nonprofits operating in Adams County, particularly The Nature Conservancy, hold significant acreage and financial resources while that land is removed from property tax rolls. The column estimated roughly $750,724 in annual lost property tax revenue from about 20,000 acres and raised questions about fairness for county taxpayers and the funding of schools and local services.

A local opinion piece put the spotlight on land owned by national conservation nonprofits in Adams County and the fiscal effects of their tax-exempt status. The columnist traced the legal basis for exemptions to a 1924 state constitutional amendment and to Ohio Revised Code 5709.09, and used county acreage figures to produce an estimate of foregone property tax revenue.

The writer estimated that approximately 20,000 acres owned locally by The Nature Conservancy would generate about $750,724 annually in property taxes if privately owned. That estimate included an allocation of roughly $462,547 to local schools and about $204,871 toward county expenses. Those figures frame the column’s core argument: that the current tax treatment produces measurable revenue losses for school districts, townships and county government at a time when local budgets are under pressure.

The columnist contrasted those local effects with The Nature Conservancy’s national financial profile, noting reported 2023 donations, investment income, payroll and asset figures to underline the organization’s overall capacity. At the same time, the piece acknowledged that the Conservancy has made targeted, modest investments in the county, including a December announcement of $100,000 in grants and scholarships and small township payments such as one example of $268. The column framed those outlays as limited compared with the value of tax-exempt acreage.

For Adams County residents, the debate touches on how property tax policy intersects with land conservation, local revenue needs and public services. School districts rely heavily on property taxes for classroom funding; counties and townships depend on them for infrastructure, emergency services and other essential functions. When large blocks of land are removed from the tax base, remaining taxpayers may face greater pressure to shoulder service costs or to accept cuts.

Policy options in play include voluntary payments in lieu of taxes, expanded targeted grants, state-level changes to nonprofit tax law, or local agreements that balance conservation goals with revenue needs. Any change would involve state constitutional and statutory considerations that shaped existing exemptions, as well as local political choices about priorities and fairness.

The column invited local readers to weigh whether current tax rules strike the right balance between conserving natural lands and maintaining equitable funding for schools and government services. The discussion is likely to prompt county officials, school leaders and residents to examine the scale of exempt holdings, the fiscal trade-offs involved, and possible steps to address perceived gaps between nonprofit capacity and local budget impacts.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?