Baker City former adviser charged in $1.6 million fraud scheme

Jeffrey Thomas Higgins, a former Baker City adviser, is accused of a 17-year fraud that prosecutors say cost clients more than $1.6 million.

A former Baker City investment adviser is accused of stealing client stock shares, reselling them and routing the money into his own bank account in a long-running scheme prosecutors say produced more than $1.6 million in losses.

Jeffrey Thomas Higgins, 54, made his first federal-court appearance Thursday and was released pending further proceedings after being charged by information with investment fraud. The case is being investigated by the FBI, and Assistant U.S. Attorneys Bryan Chinwuba and Andrew T. Ho are prosecuting it.

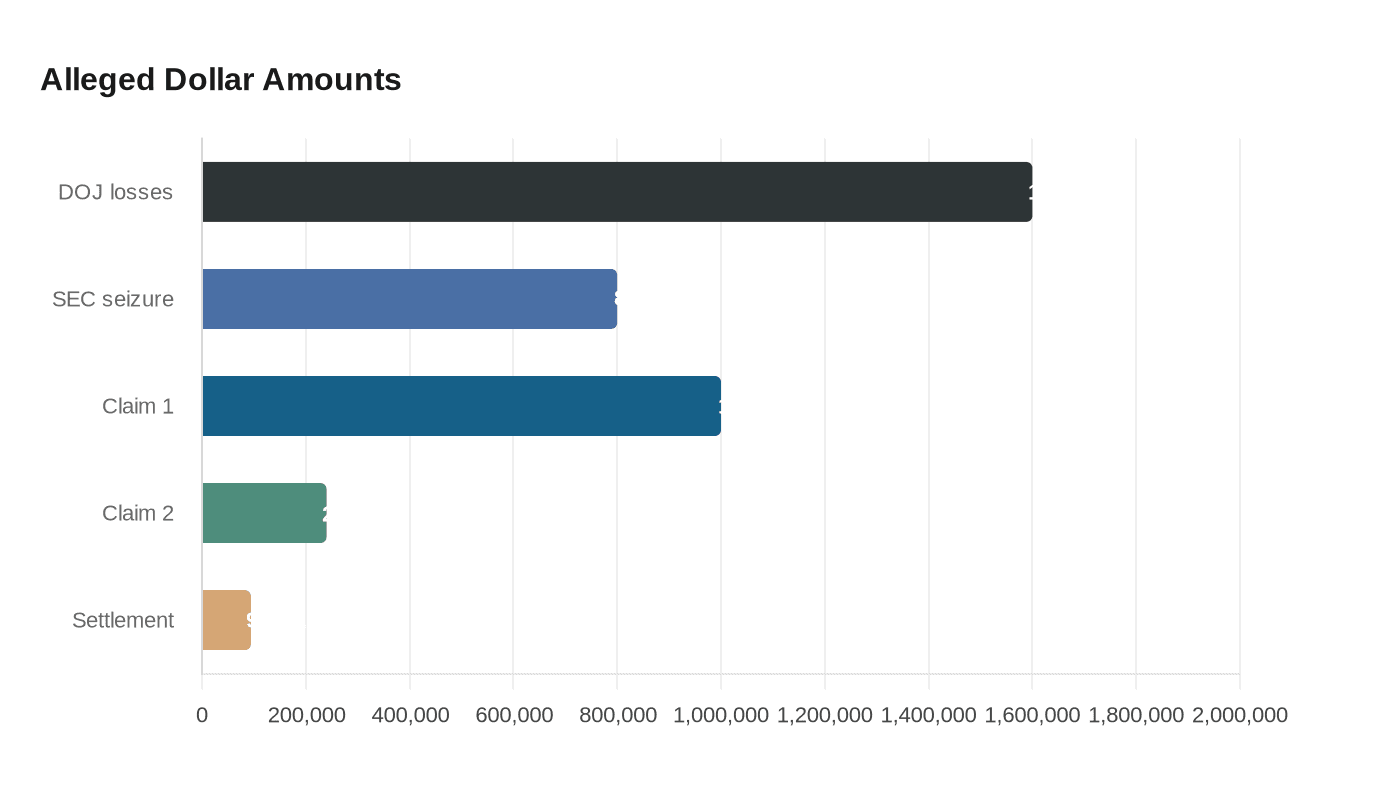

Federal prosecutors say Higgins worked as an investment adviser in Baker City from December 2007 through June 2024, while the alleged misconduct stretched from about 2007 until June 2024. They say he told investors he was buying stocks for them at steep discounts, sometimes as much as 91 percent below market value, when in fact he was buying the shares at market price, then selling them without the clients’ knowledge. Prosecutors allege he used the proceeds for himself and created fictitious annual statements to make the investments appear profitable. Accurate purchase documents were mailed to a post office box he controlled, according to public reporting.

The criminal case is unfolding alongside a separate civil enforcement action. On April 6, the Securities and Exchange Commission filed a complaint alleging Higgins misappropriated more than $800,000 in securities from 12 clients between September 2017 and February 2024 through a sham program he called Cumulus. The SEC says Higgins, while acting as a registered representative and investment adviser representative at a dually registered firm, used falsified documents and signatures to divert securities to his personal brokerage account and sent fictitious annual reports from a personal Hotmail account. Regulators say the arrangement collapsed when he could not meet a client withdrawal request.

The SEC complaint also says Higgins admitted to firm leadership in June 2024 that he had been misappropriating securities since about 2007. Public records show Western International Securities discharged him June 21, 2024, and FINRA barred him effective July 1, 2024 after he failed to cooperate with an investigation. Public reporting has also tied seven customer disputes to his discharge, including claims seeking $1 million and $240,000, plus one earlier arbitration that settled for $94,211.

For Baker County investors who ever dealt with Higgins, the warning signs in this case are straightforward: account statements that do not match trade confirmations, promises of unusually deep discounts, and documents that arrive with no clear paper trail. Investors can verify an adviser’s registration through FINRA’s BrokerCheck system and report concerns to the SEC, FINRA or the FBI as the federal case moves ahead.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip