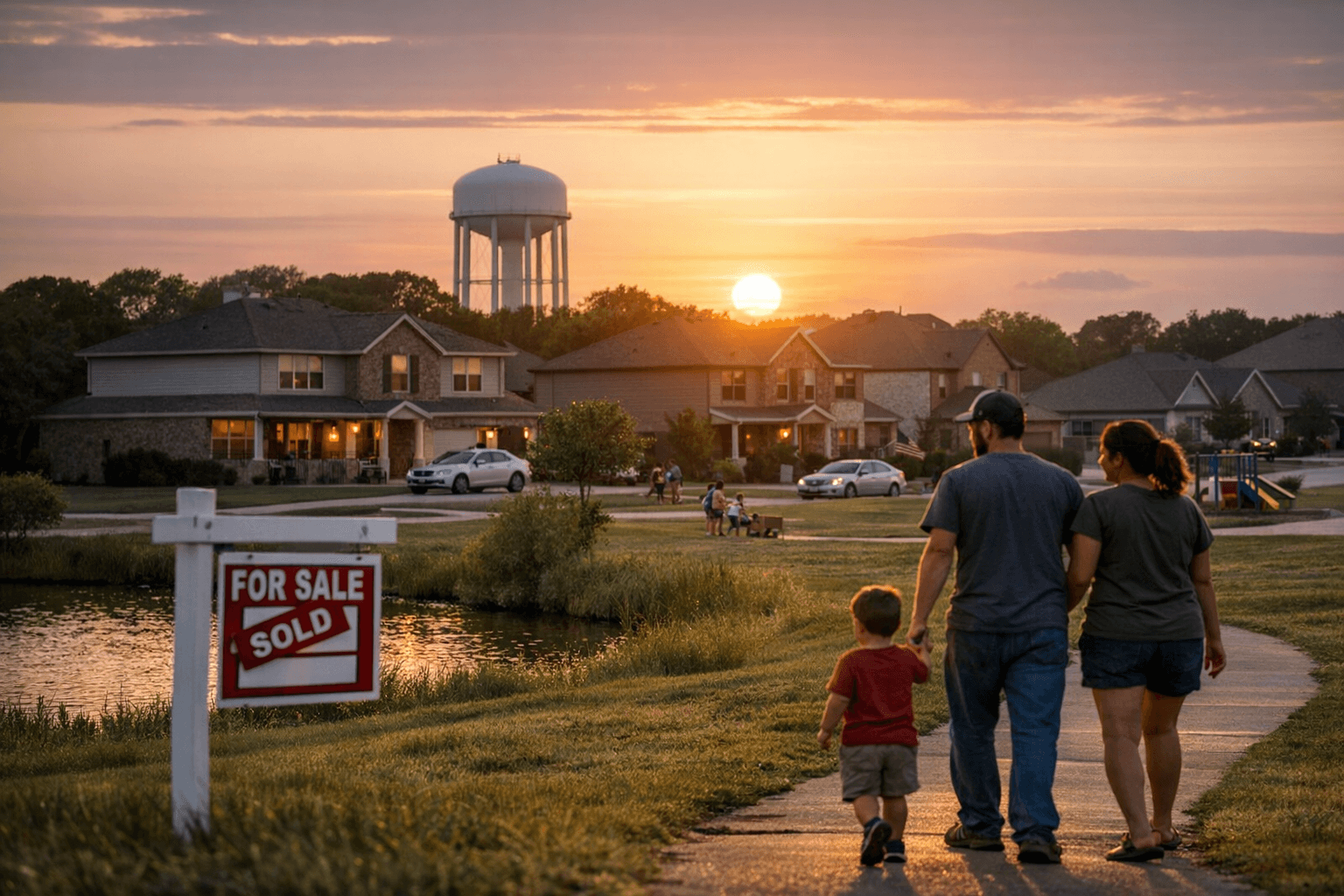

Why McKinney Was Ranked the Country’s Most Affordable City

A recent ranking from The Motley Fool placed McKinney at the top of a national affordability list by weighing cost-of-living measures against median household income. This article explains the ranking methodology, why McKinney scored highly, and what the result means for moderate- and low-income households, local housing markets, and policy choices in Collin County.

1. The ranking: affordability measured as cost of living relative to income

The Motley Fool ranking compared local cost-of-living indicators against median household income to produce an affordability score; cities where incomes outpace local prices rise in the standings. That methodology highlights places where residents, on average, have stronger purchasing power rather than simply low prices. For McKinney, a relatively moderate cost-of-living index combined with a notably high median household income produced the top position in the list.

2. Median household income drove McKinney’s high placement

The ranking’s formula gave weight to median household income as the numerator in affordability comparisons, and McKinney’s median household income is substantially above the national median. By contrast, the U.S. Census Bureau’s most recent national median household income (2022 estimate) is roughly $70,800, so municipalities with incomes materially above that baseline gain an advantage in income-adjusted affordability metrics. That arithmetic explains why McKinney, a higher-income suburban city in Collin County, performed well on the composite measure.

3. Cost-of-living metrics have limits for local housing realities

Cost-of-living indices typically bundle categories such as groceries, utilities, transportation and rents, which can understate localized housing-market pressure when median home values and mortgage rates diverge. In fast-growing suburbs, housing purchase prices and for-sale inventory trends often matter more to long-term affordability than short-term commodity price differences. McKinney’s placement reflects the composite measure, but that measure can mask acute housing affordability stress for homebuyers facing elevated purchase prices and tighter credit conditions.

4. Elevated home prices change the picture for many residents

Local housing experts and some residents have questioned whether the “most affordable” label reflects the experience of moderate- and low-income households, given elevated median home prices in the region. Even when median household income is high, distribution matters: if a large share of income gains sits with higher-income households, median housing costs can price out middle- and lower-income buyers. For working families and newcomers in Collin County, homeownership affordability is determined by sale prices, down-payment requirements, and mortgage costs, not just the income-to-cost ratio used by rankings.

5. Distributional effects: averages vs. lived experience

The ranking highlights an important statistical caveat: averages and medians can conceal wide dispersion. A city with a strong middle-to-upper-income population can look “affordable” on paper while lower-income residents face rent burdens or long commutes. This divergence matters for local social services, school funding needs, and demand for subsidized housing; policymakers must assess whether headline affordability aligns with the experience of families earning near the lower quartiles of the income distribution.

6. Market implications for Collin County housing and labor markets

A high-profile affordability ranking can influence demand patterns, drawing attention and potentially more in-migration from buyers seeking value, which, paradoxically, can put upward pressure on prices. For local employers, a reputation for affordability can aid recruitment, but if housing supply fails to expand for middle-income households, employers could face labor shortages in service and skilled-trades sectors. Monitoring housing starts, permitting activity, and inventory levels will be important to measure whether the ranking translates into sustained market changes.

7. Policy levers Collin County and McKinney leaders should consider

To align headline affordability with broader community needs, officials can pursue targeted actions: increase incentives for deed-restricted affordable units, accelerate permitting and infrastructure funding near transit and job centers, and expand preservation of naturally occurring affordable housing. Local fiscal policy and zoning reform that enable diverse housing types (smaller single-family lots, duplexes, accessory dwelling units) would help supply keep pace with demand, reducing the risk that an affordability ranking becomes a short-term headline rather than a durable advantage.

8. Long-term trends: growth, inequality and resilience

McKinney and Collin County are part of a larger long-run dynamic in Sun Belt metros: rapid population and job growth, rising housing demand, and uneven distribution of income gains. Over the next decade, sustaining affordability will depend on balancing growth with strategic investments in transportation, schools, and affordable housing supply. Without those moves, statistically “affordable” places risk becoming unaffordable for the very households that form the backbone of local economies.

9. What residents should watch next

Track three measurable indicators to judge whether the ranking reflects long-term affordability: changes in median sale price and rent, housing inventory and time on market, and the share of households paying more than 30% of income on housing. If prices rise while inventory remains tight, the practical affordability for moderate- and low-income families will worsen despite favorable headline metrics. Local advocates and officials should use such indicators to guide targeted interventions.

10. Bottom line for Collin County residents

The Motley Fool ranking spotlights McKinney’s relatively strong income-to-cost ratio, but it is not a substitute for granular analysis of housing access and income distribution. For many residents, particularly those not near the median income, affordability depends on home prices, rental markets, and policy choices made at the local level. Policymakers, employers and community groups should treat the ranking as a prompt to measure who benefits from regional prosperity and to act where gaps persist.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?