Colorado to host wildfire insurance town hall for residents

Douglas County homeowners got a state wildfire insurance town hall with rules on policy copies, contents coverage and temporary housing as premiums, renewals and cancellations loom.

Colorado regulators hosted a virtual town hall Wednesday night for Douglas County homeowners and other Coloradans facing wildfire premiums, nonrenewal notices and coverage gaps. Commissioner Michael Conway and Colorado Division of Insurance staff took questions on homeowners, auto, health and flood insurance, plus Disaster Assistance Center information, in a session that included live Spanish translation and required registration.

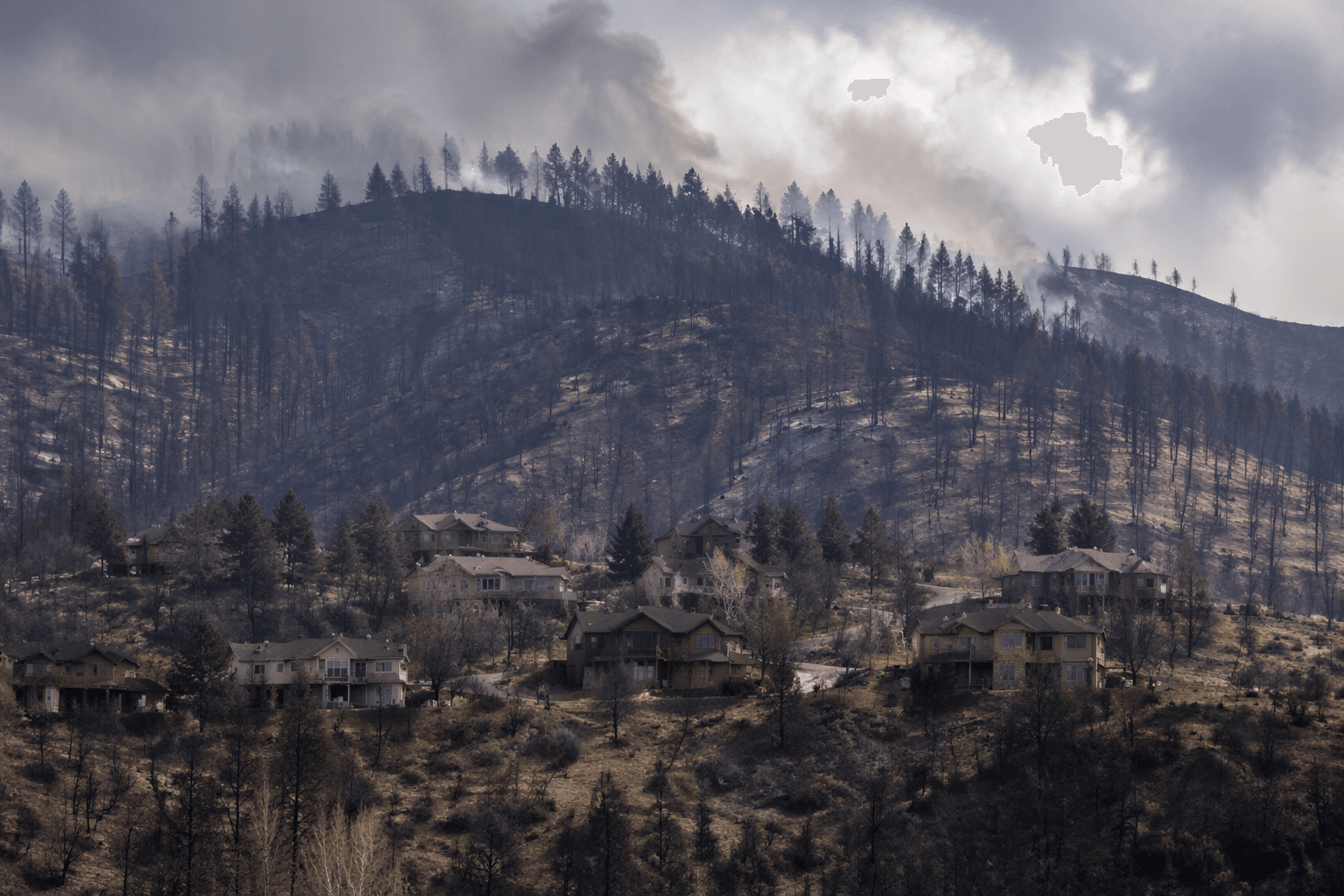

The forum ran from 5 p.m. to 8 p.m., with presentation slides and a recording to be posted later. The wildfire guidance covers residents dealing with the 2026 fires and sorting out coverage, claims and recovery while multiple wildfires continue to burn across Colorado.

In a governor-declared wildfire disaster, insurers must provide a policy copy within three business days of a request. If an owner-occupied home is a total loss, Colorado law requires carriers to offer at least 65% of contents coverage without requiring an inventory, along with at least 24 months of additional living expense coverage, plus two possible six-month extensions.

Draft emergency rules cover medical equipment, prescription refills, special enrollment periods and additional living expense coverage. DOI can help consumers understand coverage, contact an insurer or agent, file claims and navigate recovery, but it cannot rewrite every carrier’s underwriting model. Insurers still use their own tools, methodologies and maps to price wildfire risk, even as Colorado’s Wildfire Resiliency Code sets standards for structure hardening and defensible space in wildland-urban interface areas.

Colorado created the FAIR Plan to provide property insurance when traditional coverage is unavailable, and lawmakers added the Strengthen Colorado Homes Enterprise through SB26-155 to fund hail-mitigation roof grants and study ways to reduce wildfire-related insurance costs. Colorado homeowners insurance is under pressure from both hail and wildfire risk.

Homeowners heading into renewal season should watch for premium spikes, a notice that a carrier will not renew the policy, demands for mitigation work, or any uncertainty about flood coverage after a wildfire. Questions to ask include whether the insurer will provide the full policy quickly, what the contents limit will be if a house is destroyed, how long temporary housing coverage will last, and whether the home still qualifies for traditional coverage or needs the FAIR Plan instead.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?