New Mexico's 36% Lending Cap Saves Millions, but Faces Growing Threats

New Mexico's 36% lending cap saved borrowers over $50 million in two years while loan volume actually grew, but fintech firms are lobbying for exemptions that could undo those gains.

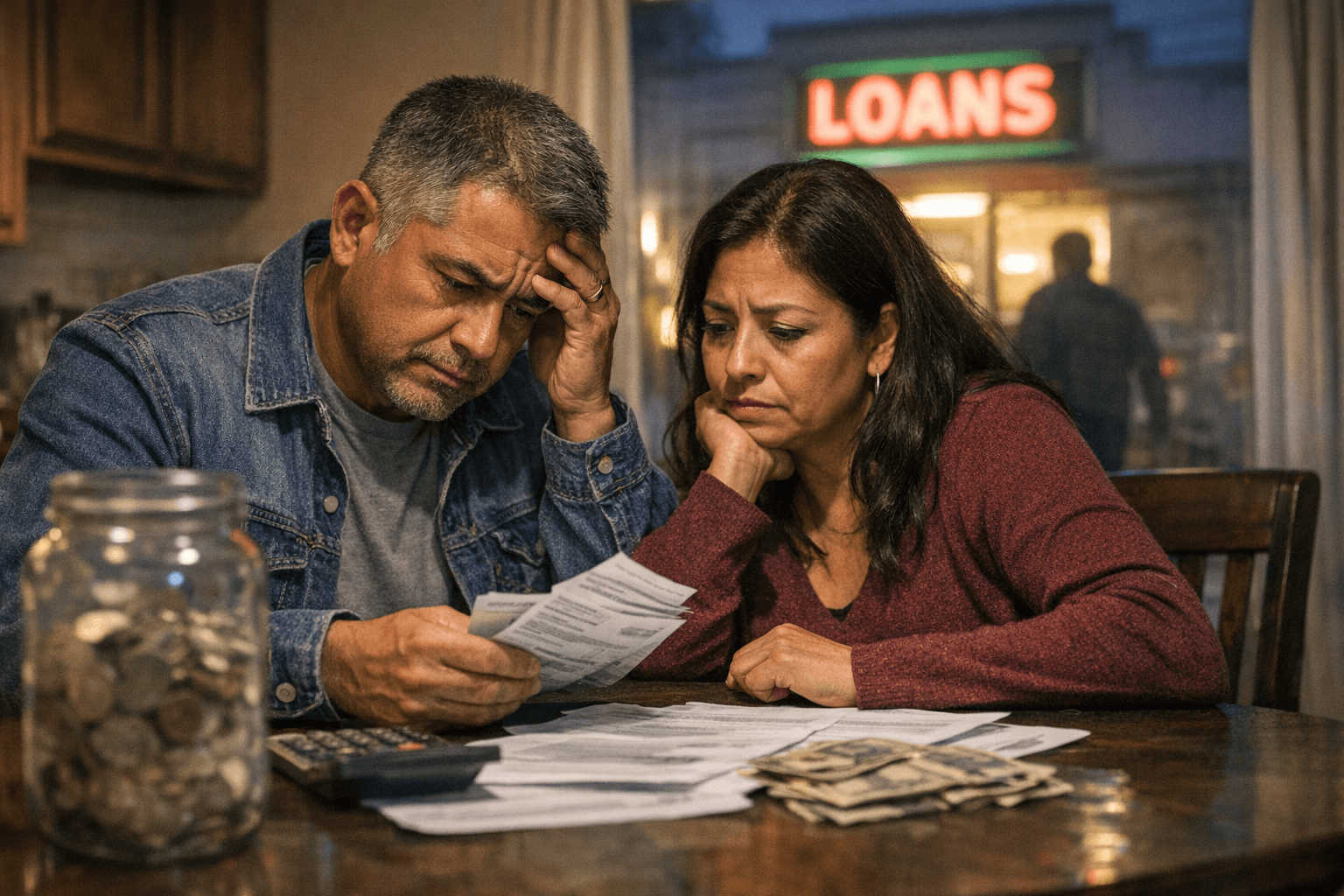

New Mexico borrowers saved more than $50 million in fees and interest on small loans in 2023 and 2024 combined, compared to 2022 levels, according to enforcement findings from the state's Financial Institutions Division. That figure, cited in an op-ed by Katie Gutierrez of Think New Mexico, represents the clearest measure yet of what the legislature's bipartisan 2022 interest-rate cap has delivered. The question now is how long it lasts.

Gutierrez's piece, published Monday in the Los Alamos Daily Post, makes the case that the 36% annual percentage rate ceiling on small loans did not, as critics warned, collapse the lending market. Instead it restructured it. The number of licensed small lenders in New Mexico fell from 531 in 2022 to 270, as high-cost operators exited rather than comply. But the total dollar value of small loans rose 31.7% in inflation-adjusted terms over the same period, driven by credit unions and tribal lenders that could profitably serve borrowers at rates below the cap.

National Credit Union Administration data Gutierrez cites underscores the shift: loan originations at credit unions climbed nearly 30% between December 2022 and December 2025. For Los Alamos, where Zia Credit Union has long served local households, that trajectory reflects a broader pattern of compliant lenders expanding into space vacated by payday-style operators.

The threat Gutierrez identifies sits in a category of fintech products called "earned wage access," or EWA. These products allow workers to draw wages before payday, and their providers are actively lobbying state and federal regulators for exemptions from rate-cap laws, arguing the advances are not technically loans. That distinction is already contested at the federal level: the Consumer Financial Protection Bureau has issued advisory guidance treating certain employer-offered EWA products as outside the Truth in Lending Act's definition of credit.

If New Mexico's legislature or regulators follow that logic and carve EWA out of the 36% cap, Gutierrez argues the products could function identically to payday loans, deducting fees directly from paychecks with no APR disclosure requirement. The fee structures involved, she warns, could replicate the debt cycles the 2022 law was designed to break.

Los Alamos County's household incomes rank among the highest in New Mexico, but community organizations here work with residents for whom a single high-cost short-term loan can cascade into prolonged financial strain. Local credit unions also have a concrete competitive stake: an EWA exemption would allow fintech companies to undercut institutions operating under the cap while facing none of its constraints.

The Financial Institutions Division of the Regulation and Licensing Department holds the primary regulatory authority to hold or yield that line at the state level. Whether it does will determine if $50 million in annual savings remains a floor or a high-water mark.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?