Prince George’s homeownership debate centers on costs, racism, and wealth gaps

Prince George’s homeownership is still within reach on paper, but costs, appraisal bias and repair burdens can keep Black families from turning a purchase into lasting wealth.

Prince George’s County still sells one of the strongest Black homeownership stories in the Washington, D.C. region, but the harder question is whether families can keep the home, maintain it and build wealth once they buy it. The county’s market sits in the low-to-mid $400,000s, and that price level, paired with lending friction and rising repair costs, is reshaping what homeownership really means for longtime residents.

The gap between getting in and staying in

Dr. Kofi Bryant Sr. and other advocates push back on the idea that homeownership is only a matter of finding a program and signing papers. They argue that the real test begins after closing day, when homeowners face plumbing failures, HVAC replacements, roof repairs and the steady labor of caring for an aging house. In Prince George’s, that point matters because many residents are trying to buy into a market where the entry price is already steep, while the costs of ownership keep climbing.

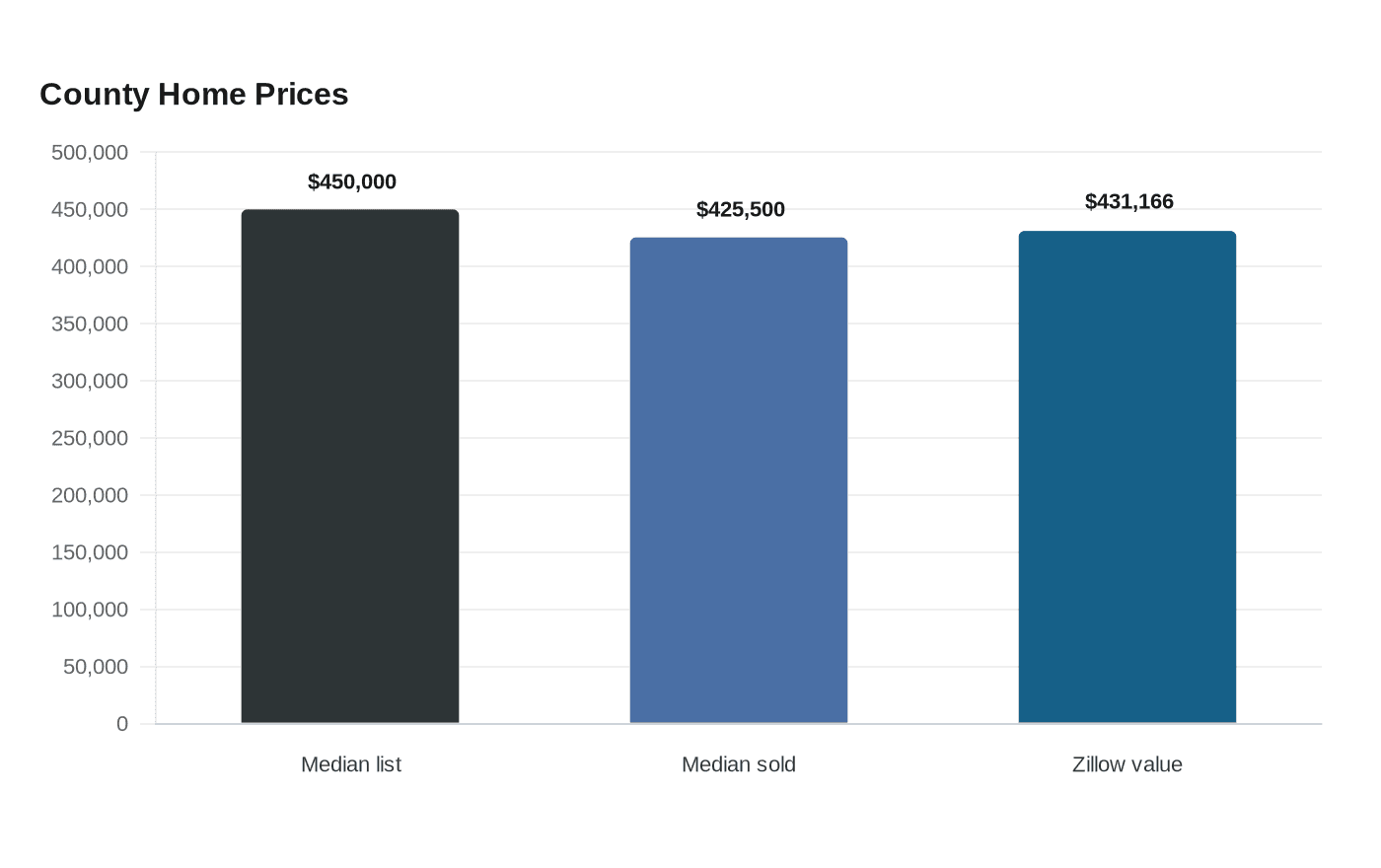

Recent market data show how tight the landscape remains. Median listing prices in the county are around $450,000, median sold prices are about $425,500, and Zillow put the typical home value at $431,166 as of May 31, 2026. That range leaves little room for error for households trying to save for a down payment, qualify for financing and still keep money aside for maintenance.

Bryant’s broader argument is that the county cannot treat homeownership as a feel-good finish line. If families are encouraged to buy without full information about the long-term costs, they can end up asset-rich on paper but financially stretched in practice. That is especially true in older neighborhoods, where even a modest house can come with expensive upkeep.

What help exists, and why it still misses people

Prince George’s County and Maryland already have programs aimed at the exact problems Bryant describes. The Maryland Mortgage Program’s Pathway to Purchase can provide up to $50,000 in down payment and closing-cost assistance for eligible Prince George’s County homebuyers. The county’s Home Ownership Preservation Program, known as HOPP, can provide up to $30,000 for health, safety, energy-efficiency and accessibility repairs in qualified owner-occupied homes.

Those programs are not just cosmetic support. County homeowner resources say rehabilitation assistance is intended to bring deteriorated homes up to contemporary minimum property standards and eliminate housing code violations. In other words, the county is trying to help residents do more than buy property. It is trying to keep housing safe, usable and compliant after the purchase.

Still, the existence of aid does not guarantee access in practice. Families have to know the programs exist, understand the eligibility rules, gather paperwork and move quickly enough to compete in a market where homes can go fast. That awareness gap matters because the households most likely to need help are often the same households least likely to receive it through ordinary market channels.

Prince George’s as a case study in Black wealth

Urban Institute data show why Prince George’s carries national significance. In 2022, Black households in the county owned 66.9 percent of the county’s total home value while making up 64.8 percent of households. Black households also had a 61.8 percent homeownership rate in the county, far above the national Black homeownership rate of 44.3 percent and above the 65.1 percent rate for all households nationwide.

Those numbers make Prince George’s look like a relative bright spot, but they do not erase the underlying wealth gap. The county’s high Black homeownership rate shows strength, yet even here, the benefits of ownership remain uneven when appraisal practices, credit access and repair costs continue to shape what a home is worth and how much equity a family can tap.

That is why this debate is not only about first-time buyers. It is also about inherited inequities that determine who gets to keep appreciating assets, who gets trapped by expensive maintenance, and who can convert a home into generational wealth.

Appraisals, lending, and the value problem

The fair housing issue extends beyond monthly payments. Brookings has reported that appraisals in majority-Black neighborhoods can be systematically biased and that homes in those neighborhoods are often valued below comparable homes in non-Black neighborhoods. That kind of undervaluation can depress equity, reduce refinancing options and limit a homeowner’s ability to borrow against value they have actually created.

The policy response has begun to catch up. Maryland established the Task Force on Property Appraisal and Valuation Equity in October 2023 under HB1097 of the 2022 legislative session. At the federal level, the U.S. Department of Housing and Urban Development issued guidance on May 1, 2024, requiring lenders to provide a reconsideration-of-value pathway for borrowers who believe an appraisal is wrong.

Those steps matter because appraisal bias is not a technical glitch. It is a wealth mechanism. When Black neighborhoods are consistently undervalued, households can do everything the market asks of them and still end up with less borrowing power, less equity and less upside than comparable white households in stronger-valued areas.

Why the county’s history still shapes today’s market

Maryland housing officials have been blunt about the larger backdrop. They say the suburbanization of poverty spread inside the Capital Beltway and that the Great Recession decimated Black wealth in Prince George’s County, with subprime mortgage lending evolving into reverse redlining. That history helps explain why many families approach homeownership cautiously, even in a county where Black ownership has been relatively strong.

The lesson is not that homeownership no longer matters. It is that ownership without fair lending, accurate valuation and realistic cost counseling can reproduce the same inequities it claims to solve. Families need more than encouragement to buy. They need financial literacy, access to down payment help, repair aid after closing, and a housing market that does not punish Black neighborhoods for their racial makeup.

In Prince George’s County, the real measure of housing policy is no longer how many people can be told to aspire to ownership. It is whether those people can buy, maintain and keep a home long enough for that home to become lasting wealth.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip