Claremont Savings Bank expands business development team, adds leaders

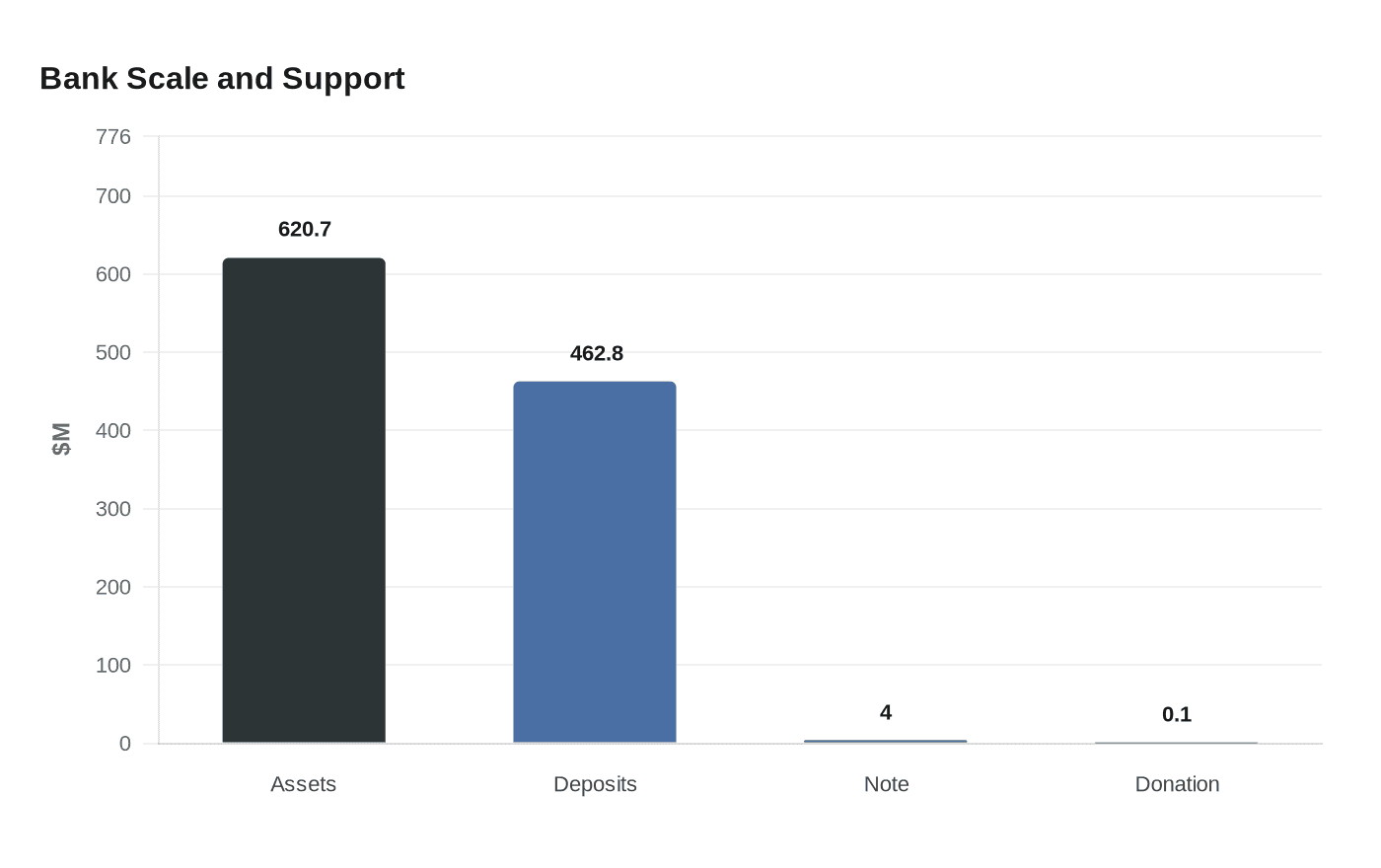

Adam Hamilton joins Claremont Savings Bank’s expanded business-development team as the bank, with about $620.7M in assets, highlights a past $4 million emergency loan to SAU 6.

Adam Hamilton, named Senior Business Development Officer, Vice President, is one of three new business-development leaders Claremont Savings Bank announced as part of a strategic expansion intended to deepen lending and advisory capacity across Sullivan County and the Upper Valley. The bank named Julie Martin, Business Development Officer, Vice President, and Zach Haines, Business Development Officer, Vice President, in the April 7, 2026 announcement that framed the hires as a unified, community-centered build-out of commercial and municipal outreach.

The release said the staff changes aim to "reinforce the Bank’s commitment to relationship-driven service and deepen its support for local businesses, municipalities, and nonprofit organizations," and it tied the reorganization to recent leadership changes in the lending line. Joe Kenney, who joined CSB as Executive Vice President and Chief Lending Officer earlier this cycle, provided a brief statement: "I am truly honored and excited to be joining Claremont Savings Bank." Kenney’s role establishes the lending leadership that will coordinate the new business-development officers.

The hires arrive at a bank of material regional scale. Public filings and call-report summaries show Claremont Savings Bank holding roughly $620.7 million in total assets and about $462.8 million in deposits as of year-end 2025, and the institution operates five local offices including branches in Claremont and Charlestown, New Hampshire, and Springfield, Vermont. The bank, founded in 1907 and organized as a mutual savings bank, has used that deposit base to underwrite local needs: in August–September 2025 CSB provided a $4 million reimbursement-anticipation note to SAU 6 to bridge a budget shortfall and made a related $100,000 donation to preserve extracurricular programs.

Those concrete precedents inform what the expanded team could mean for municipal budgets and school finance in 2026. With a dedicated Senior Business Development Officer and two additional business officers reporting into Kenney’s lending operation, local governments that previously navigated emergency financing could see quicker response times on short-term lines, more active advice on bond or note structures, and hands-on support for grant‑funded capital projects. Industry research and trade commentary underscore that community banks leverage local knowledge to speed small-business credit decisions and to provide municipal underwriting and technical assistance, functions CSB’s announcement signaled it intends to emphasize.

For Sullivan County small businesses, the staffing increase suggests more proactive relationship management: locally tailored lending discussions, outreach on federal or state grant-matching programs, and referrals for USDA or Northern Border Regional Commission opportunities. Whether that translates into specific new municipal products, underwriting targets, or measurable loan-growth this year will depend on how the new officers convert outreach into signed commitments; the bank’s 2025 annual report and recent call reports establish the baseline lending capacity against which any 2026 changes will be judged.

Claremont Savings Bank’s concentrated hiring and Kenney’s elevation make a clear operational bet: channel a $620.7 million balance sheet and a five-branch footprint into faster, relationship-driven municipal and commercial lending across the region. Local officials and business owners will watch whether the expanded team shortens turnaround times and increases advisory capacity during a year of tight municipal budgets and capital needs.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?