2024 Audit Finds Internal Control Weaknesses in Owsley County Sheriff Tara Roberts

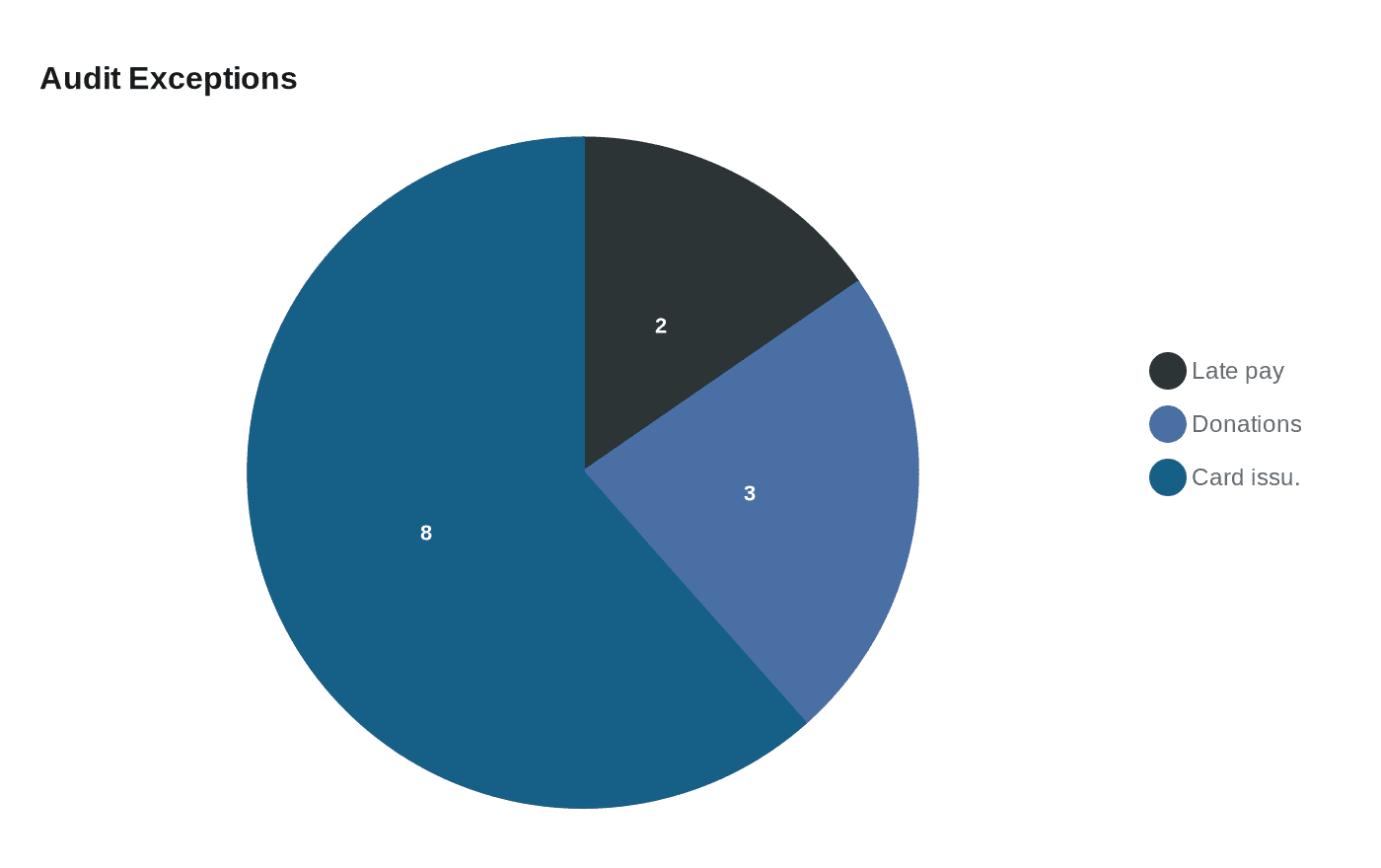

Auditor Allison Ball found Owsley County Sheriff Tara Roberts’ office lacks segregation of duties and flagged two late disbursements, three donations totaling $200, and eight credit card transactions.

State Auditor Allison Ball released the audit of the 2024 financial statement of Owsley County Sheriff Tara Roberts from FRANKFORT, Ky., finding that “the Owsley County Sheriff’s office does not have adequate segregation of duties.” The report names a single bookkeeper as performing multiple core functions: collecting payments, preparing daily checkout sheets, preparing disbursements, posting to receipt and disbursement ledgers, preparing all reports, and performing all reconciliations.

The audit identified specific exceptions in the sheriff’s 2024 fee account when it tested disbursements: “Two disbursements were not paid within 30 days,” there were “three disbursements for donations totaling $200,” and “Eight credit card transactions without proper supporting [...]” as shown in the Auditor’s excerpt. The credit card finding in the release is truncated in the public excerpt; the Auditor’s office recommends retrieving the full report on the Auditor’s website for the complete wording and any additional details.

Auditor Ball’s report reiterates statutory audit practice for county sheriffs: “State law requires the auditor to annually audit the accounts of each county sheriff,” and in compliance the office issues two sheriff’s reports each year - one for the tax account and one for the fee account used to operate the office. The audit materials provided note that the sheriff’s financial statement did not follow generally accepted accounting principles; “however, the sheriff’s financial statement is fairly presented in conformity with the regulatory basis of accounting, which is an acceptable reporting methodology.” That regulatory-basis approach is used across Kentucky’s sheriff audits - the Auditor’s office cites all 120 sheriff audits as following that methodology.

The Auditor sets out a direct corrective path: “We recommend the Owsley County Sheriff’s Office separate the duties involved in receiving payments, preparing daily checkout sheets, preparing disbursements, posting to ledgers, preparing reports, and preparing reconciliations.” The report adds a pragmatic alternative: “If this is not feasible due to a limited budget, cross checking procedures should be implemented and documented by the individual performing the procedures.” The audit further states plainly, “The sheriff did not provide a response.”

Local coverage in the Booneville Sentinel ran under the headline “Ball Releases Audit of Owsley County Sheriff’s Tax Settlement” on the paper’s March 5, 2026 issue page, with a summary noted March 6 in other circulation notes; the Sentinel page includes subscriber-only access and lists its contact as PO Box 129 Booneville, KY 41314, Phone: 1-606-464-2444. Neighboring-county audits show the range of outcomes the Auditor finds statewide: WPKYOnline reported that Caldwell County Sheriff Don Weedman’s 2024 financial statement had “no instances of noncompliance,” while a statewide aggregation noted a Whitley County sheriff audit also identified inadequate segregation of duties.

Until the full Auditor of Public Accounts PDF for Owsley County’s 2024 sheriff fee-account audit is retrieved from the Auditor’s website and the sheriff’s office provides any response, the report’s findings and recommendations stand as the official record: documented internal-control weaknesses, specified disbursement exceptions, and a clear call for separating duties or documenting cross-checks in the Owsley County Sheriff’s Office.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip