Analog Devices Q1 tops forecasts as industrial, communications surge

Analog Devices posted $3.16 billion revenue and $2.46 non‑GAAP EPS, driven by industrial and communications demand and a raised dividend that boosts shareholder returns.

Analog Devices reported fiscal first‑quarter revenue of $3.16 billion and non‑GAAP earnings of $2.46 a share, handily beating expectations and sending the stock up about 9% in premarket trading. The results reflected broad‑based strength across industrial and communications end markets, and management raised the company’s quarterly dividend as it pledged to return free cash flow to shareholders.

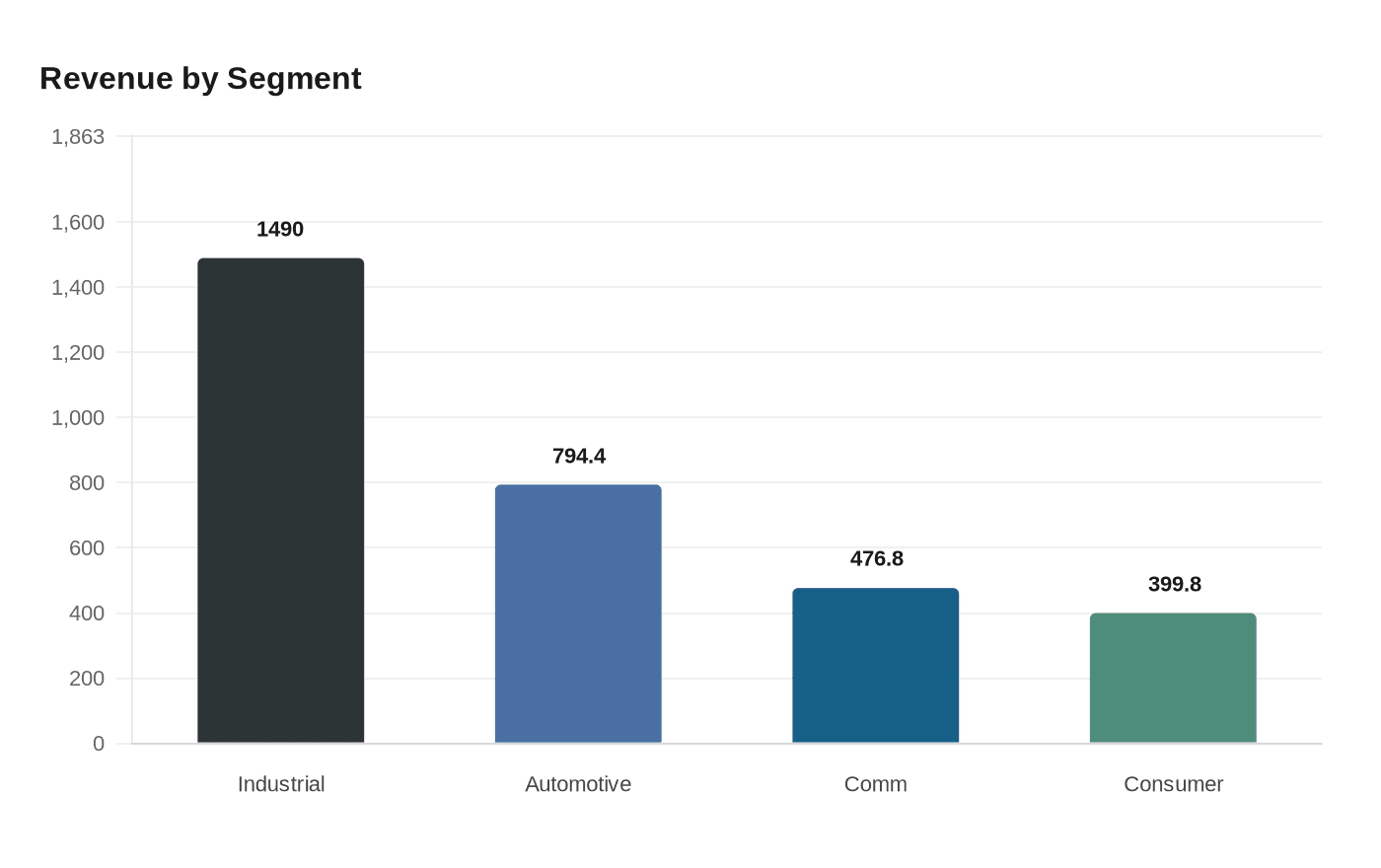

Revenue rose 30% year over year and 3% sequentially. Industrial sales accounted for $1.49 billion, or 47% of the quarter, expanding 38% from a year earlier; automotive produced $794.4 million, 25% of revenue and up 8% year over year but down sequentially; communications delivered $476.8 million, up 63% year over year; consumer revenue was $399.8 million, a 27% year‑over‑year gain. Management said industrial finished the quarter up 5% sequentially, while automotive fell about 8% from the prior quarter.

Margins were unusually high for the analog chipmaker. Adjusted gross margin was 71.2%; one report cited a 240‑basis‑point year‑over‑year expansion while another noted a 140‑basis‑point sequential gain. Adjusted operating margin reached 45.5%, which has been reported as a 500‑basis‑point increase year over year and a 200‑basis‑point improvement sequentially. Non‑GAAP EPS was about 9% higher sequentially and roughly 51% above the year‑ago quarter.

CEO Vincent Roche framed the results as a continuation of momentum: “Well, we extended our momentum through the first quarter with revenue, profitability and earnings per share, all coming in above the midpoint of our guidance. Year‑over‑year growth was broad‑based across our end markets with particular strength in industrial and communications, reflecting both cyclical improvement and company‑specific execution. This performance underscores the strength of ADI's diversified and resilient business model, enabling us to navigate uncertainty while continuing to capture share in the markets that matter most.”

Roche also pointed to durable demand in industrial niches: “our book‑to‑bill was well above 1. And that does exclude any impact from pricing. So we feel very good about where we are landing from an orders perspective on the industrial. For 4 straight quarters, we've been an above seasonal growth with double‑digit year‑over‑year growth, and that is driven by strength across all of the industrial segments.” He added that aerospace and defense, about a third of industrial, are reaching new highs in bookings and backlog.

Looking ahead, the company guided fiscal Q2 revenue to roughly $3.5 billion plus or minus $100 million, implying double‑digit sequential growth. CFO Richard Puccio said ADI expects roughly 100 basis points of gross margin expansion next quarter on a reported basis, or 150 basis points when excluding certain Q1 discrete items, driven by favorable mix and pricing. Puccio warned that operating expenses will grow in the mid‑single‑digit range because of hiring in strategic areas, a higher bonus factor and costs related to the company’s developer conference, though OpEx as a percentage of revenue should decline.

Analog Devices also highlighted its exposure to AI‑related end markets. Automated test equipment and data‑center power and optical businesses now approach 20% of revenue, and those lines grew rapidly in fiscal 2025, roughly 40% for ATE and 50% for data‑center power, positioning the company for continued above‑market expansion.

Analysts and investors will watch whether the company’s strong book‑to‑bill and backlog translate into sustained factory hiring and capital investment, and whether management’s capital‑return pledge, an 11% increase to a $1.10 quarterly dividend and a goal to return 100% of free cash flow, balances shareholder demand with longer‑term investment in product and domestic manufacturing.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?