Brown endowment cuts Blue Owl stake by 53% in first quarter

Brown’s endowment cut its Blue Owl Capital Corp. stake by 53%, signaling fresh scrutiny of a $1.8 trillion private credit market.

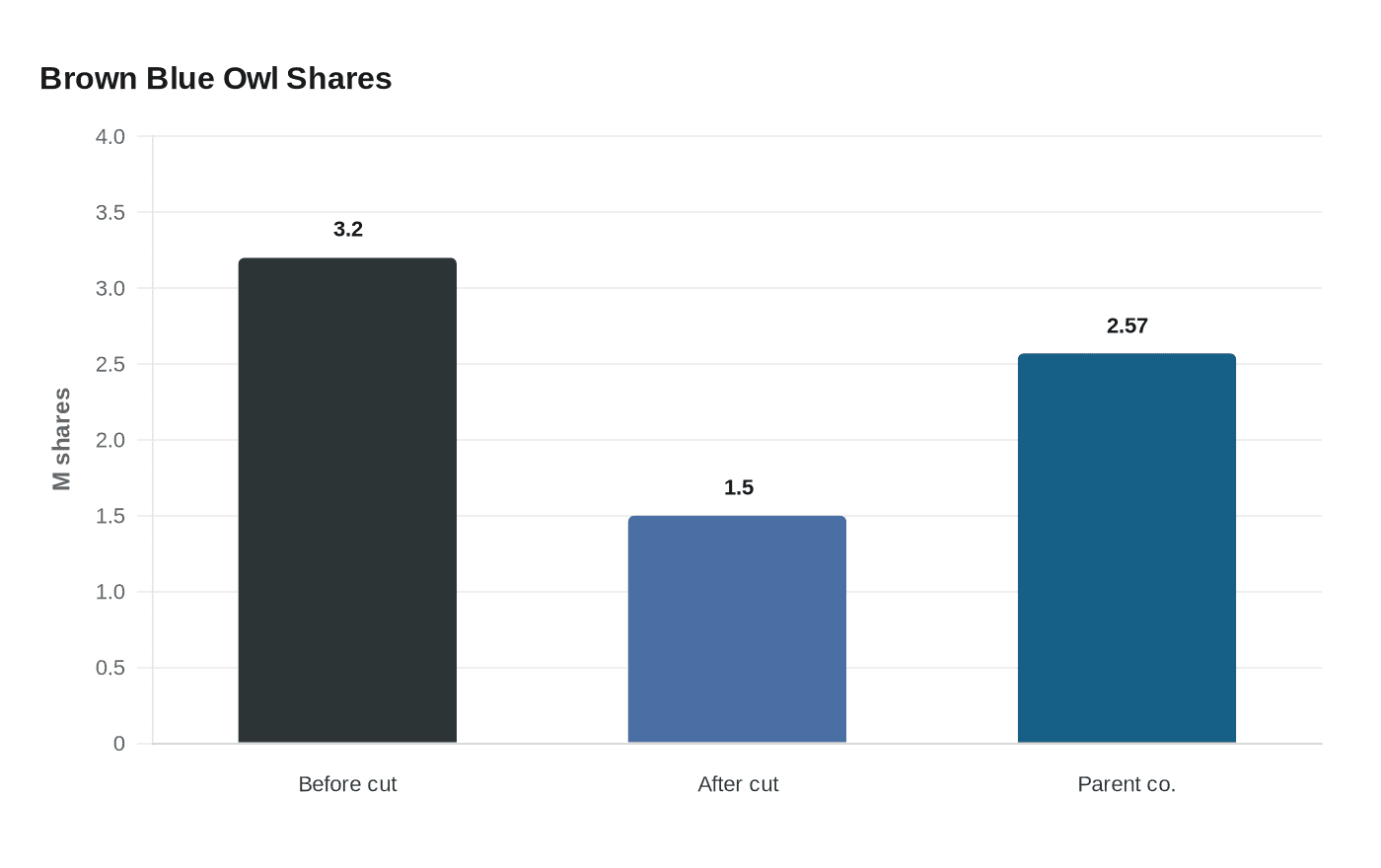

Brown University’s endowment slashed its stake in Blue Owl Capital Corp. by roughly 53% in the first quarter, trimming the position to 1.5 million shares from 3.2 million shares at the end of 2025. The move stands out because Brown is one of the country’s best-known institutional investors, and Blue Owl is among the most closely watched names in private credit.

The sale lands at a moment when private lending is under sharper scrutiny. Reuters and Bloomberg have described the private credit market as roughly $1.8 trillion, a size that reflects years of heavy institutional inflows into non-bank lending. Brown’s reduction does not prove a broad retreat from the asset class, but it does raise the question of whether some sophisticated investors are becoming more cautious about publicly traded vehicles tied to private credit.

Brown’s filing showed only the size of the change, not the reasoning behind it. That leaves open several possibilities, including valuation concerns, liquidity management, or a broader rebalancing across the university’s portfolio. Endowments routinely shift holdings to preserve returns, control risk and support long-term obligations, but changes in a fund the size of Brown’s often draw outsized attention because they can hint at how large investors are reading the market.

The cut also looks selective rather than absolute. Brown still held 2.57 million shares of Blue Owl Capital’s parent company, unchanged from the end of 2025, even as it reduced its position in Blue Owl Capital Corp. That suggests the university did not abandon the Blue Owl platform, but instead pulled back from the publicly traded business development company that gives investors daily access to private-credit exposure.

Brown has reason to be careful with those choices. The university said its endowment reached a record $8 billion as of June 30, 2025, after generating an 11.9% return in fiscal 2025. Those gains totaled $853 million and supported an all-time high of $352 million for financial aid, student support, scientific research and other priorities. Managing that pool means balancing growth with liquidity, especially when holdings sit in asset classes that can become crowded fast.

Blue Owl Capital Corp. continued to file regular SEC reports and earnings disclosures around the time of Brown’s sale, underscoring that Brown’s trim was in a liquid public security, not a locked-up private fund. For a market built on steady capital and patient investors, the message from Providence is not a full exit. It is a warning that even long-term buyers are weighing private credit more carefully than they did only a year ago.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?