CD rates still top 4%, but national averages stay much lower

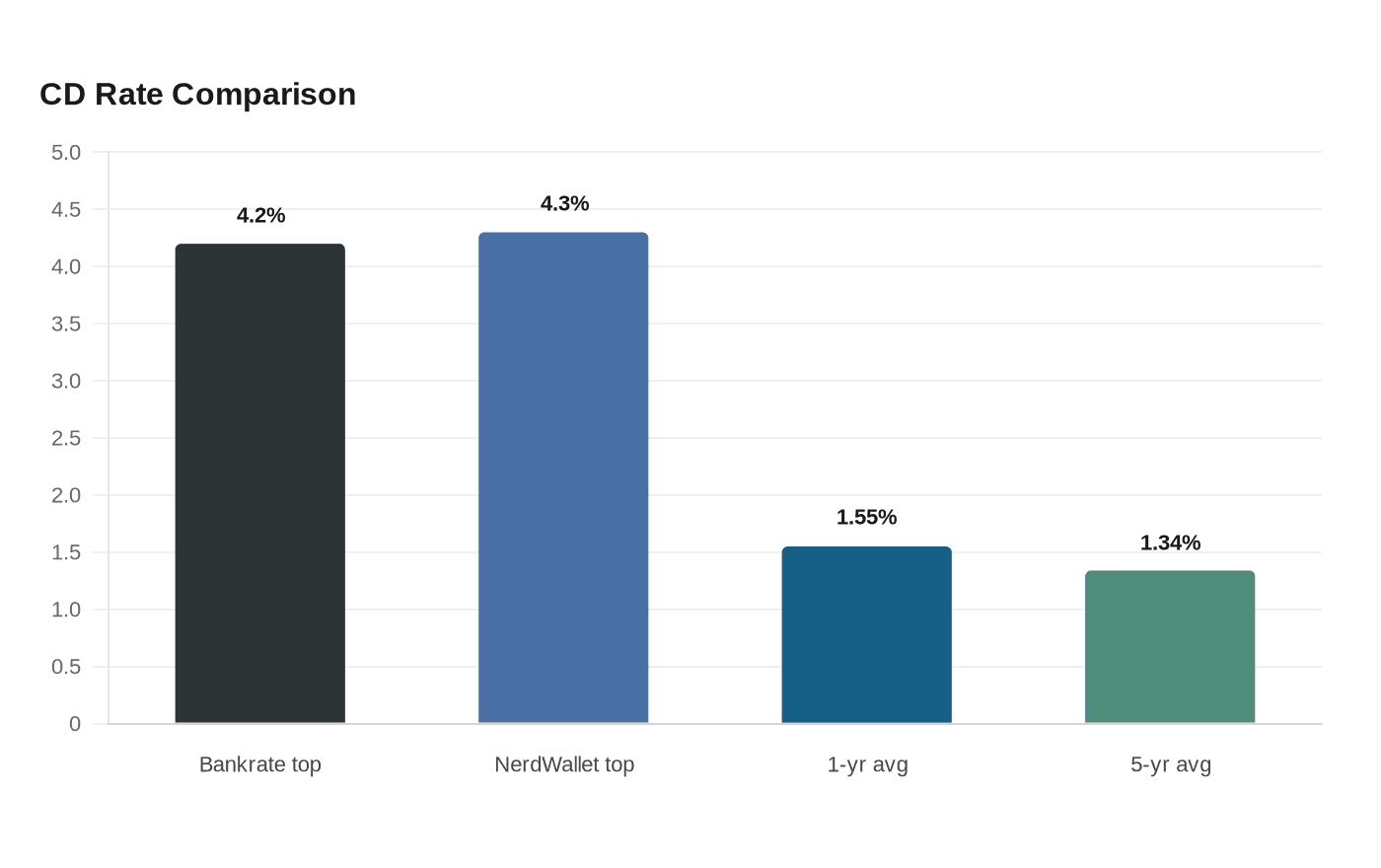

Top CDs still pay above 4%, but a one-year average of 1.55% and a five-year average of 1.34% make timing the real decision.

The best CD yields in June are still clearing 4%, but the bigger question for savers is whether to lock money away now or wait as rates soften. Bankrate’s top-tracked CD rate stood at 4.20% APY at Mountain America Credit Union, while NerdWallet’s highest current rate reached 4.30% APY at Connexus Credit Union.

That spread is striking because the national averages remain far lower. NerdWallet put the average one-year CD at 1.55% APY and the average five-year CD at 1.34% APY, a gap that helps explain why rate shoppers are still heading to online banks and credit unions for the best deals. NerdWallet said its quoted APYs were current as of June 5, 2026, while Bankrate’s CD data-center chart showed a June 3, 2026 observation.

For savers trying to decide whether to move now, the risk is mostly about timing. Bankrate says CD rates are generally trending down in 2026, even after a brief spring increase in some online one-year offers. That makes a fixed-rate CD appealing if cash will not be needed before maturity, because the rate locked in at account opening stays in place for the full term. If market rates fall further, that lock can look wise in hindsight.

The tradeoff is flexibility. A high-yield savings account or money-market fund keeps cash more accessible and lets savers benefit if rates rise again, though those rates can change at any time. Short-term Treasurys offer another option for people willing to keep money parked until maturity, with the added appeal of federal backing and a market that tends to move in step with interest-rate expectations. CDs, by contrast, can be the better fit for money with a clear deadline, such as a tuition bill, tax payment or planned home purchase.

The Federal Reserve still shapes that decision because its monetary policy seeks maximum employment, stable prices and moderate long-term interest rates. The FDIC, which defines the national rate as a deposit-weighted average paid by insured depository institutions and credit unions, publishes monthly National Rates and Rate Caps updates that help show how far the best promotional offers sit above the broader market. For savers who can give up liquidity, locking a 4%-plus CD now may still make sense. For anyone who may need cash soon, the penalty for reaching for yield can be reduced flexibility exactly when rates are near a turning point.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip