Delta Air Lines Misses Q1 2026 Profit Estimates Despite Revenue Growth

Delta posted record Q1 revenue of $14.2B but missed profit estimates as fuel and labor costs surged; reduced capacity and bag fee hikes signal a pricier summer for fliers.

Delta Air Lines turned a $289 million GAAP net loss in the first quarter of 2026, even as the Atlanta-based carrier reported a record $14.2 billion in adjusted operating revenue, up 9.4 percent from the same period a year earlier. Adjusted earnings per share came in at $0.64, missing the consensus estimate of $0.65, a result that reflects how sharply rising fuel and labor costs compressed margins despite the strongest first-quarter top line in the company's history.

Fuel prices averaged $2.62 per gallon during the quarter, while non-fuel unit costs climbed 6 percent year-over-year, squeezing an operating margin that landed at 4.6 percent for the March quarter even as pretax profit reached $530 million and free cash flow hit $1.2 billion.

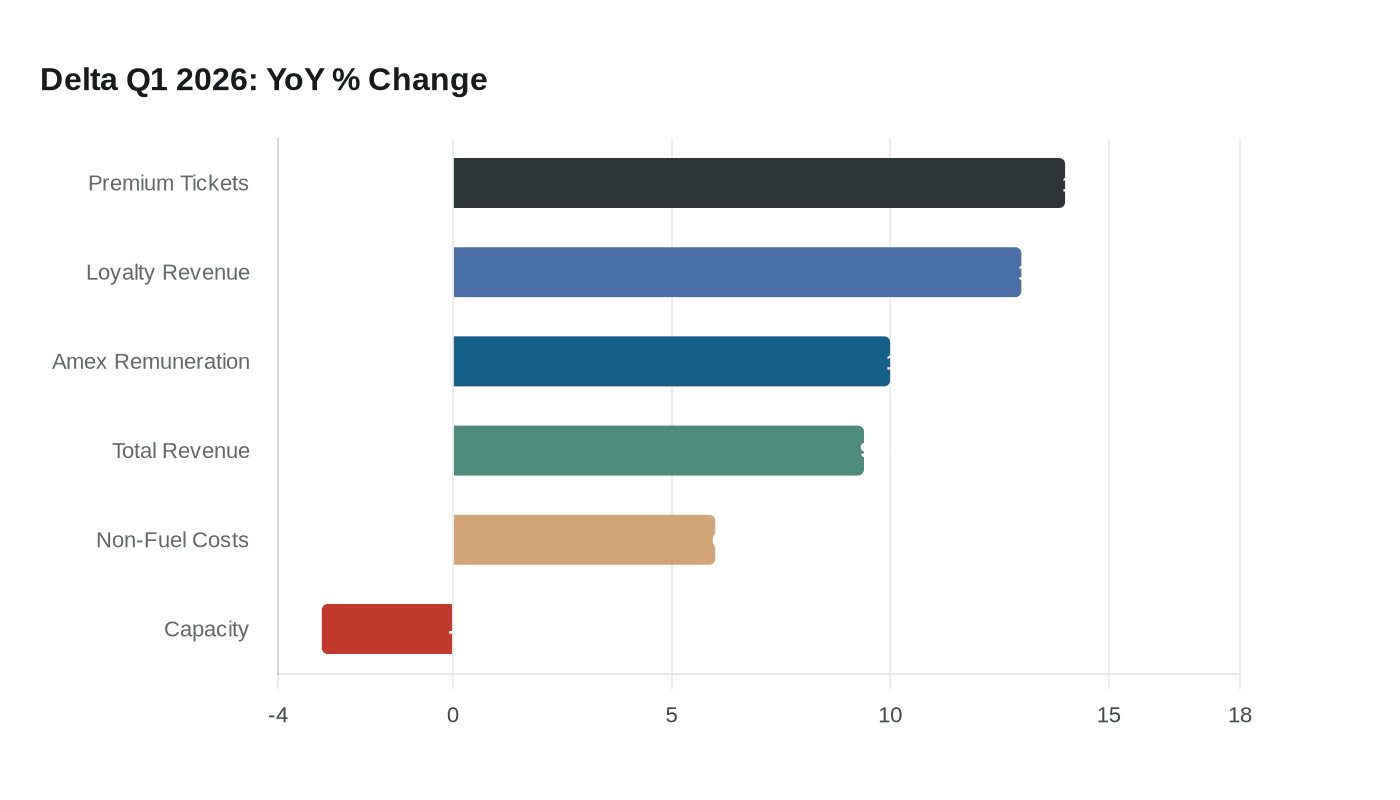

For passengers, the most direct signal in Delta's results is the capacity picture. The airline deliberately cut capacity 3 percent compared with a year earlier, a reduction it attributed to fleet renewal investments that simultaneously drove a higher premium seat mix. Premium ticket revenue surged 14 percent, and main cabin revenue increased for the first time since late 2024. Less supply against resilient demand is the textbook condition for sustained or higher fares. Delta also joined JetBlue Airways and United Airlines in raising checked bag fees, compounding the cost of travel in coach.

Premium ticket revenue rose 14 percent to $5.4 billion, loyalty and related revenue increased 13 percent to $1.2 billion, and American Express remuneration grew 10 percent to more than $2 billion. Corporate sales hit a record for the quarter, with all sectors showing positive revenue growth, and a Delta-commissioned survey found that 85 percent of corporate respondents expected travel spending to increase or hold steady in the second quarter. Management noted that premium and loyalty streams now represent 62 percent of total revenue, a structural shift that insulates the airline from swings in commodity coach pricing.

Rival United, the second-most profitable U.S. carrier, has been expanding its premium seat footprint and investing in new onboard technology, reinforcing an industry-wide push away from base-fare competition toward higher-margin cabin products. The convergence of capacity discipline and premium investment across major carriers leaves summer travelers with little near-term prospect of fare relief, particularly in business and first class.

CEO Ed Bastian indicated that sustained high fuel prices would force structural adjustments, with the airline targeting capacity reductions specifically in off-peak windows such as edge-of-day and red-eye flights, which the company identified as 15 to 20 percent less valuable than peak flying. On the balance sheet, adjusted net debt fell to $13.5 billion, below 2019 levels, down 20 percent from a year earlier, giving Delta room to absorb continued fuel volatility without compromising fleet investment.

For the June quarter, Delta guided to low-teens revenue growth, a 6 to 8 percent operating margin, and earnings per share of $1.00 to $1.50, with the outlook contingent on fuel assumptions tied to the April 2 forward curve. If that guidance holds, the summer season would represent a meaningful recovery in profitability over the first quarter's narrow margins, driven almost entirely by premium cabins filling at peak-season prices.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)