Dollar General Set to Report Earnings This Week, Alongside Oracle and Adobe

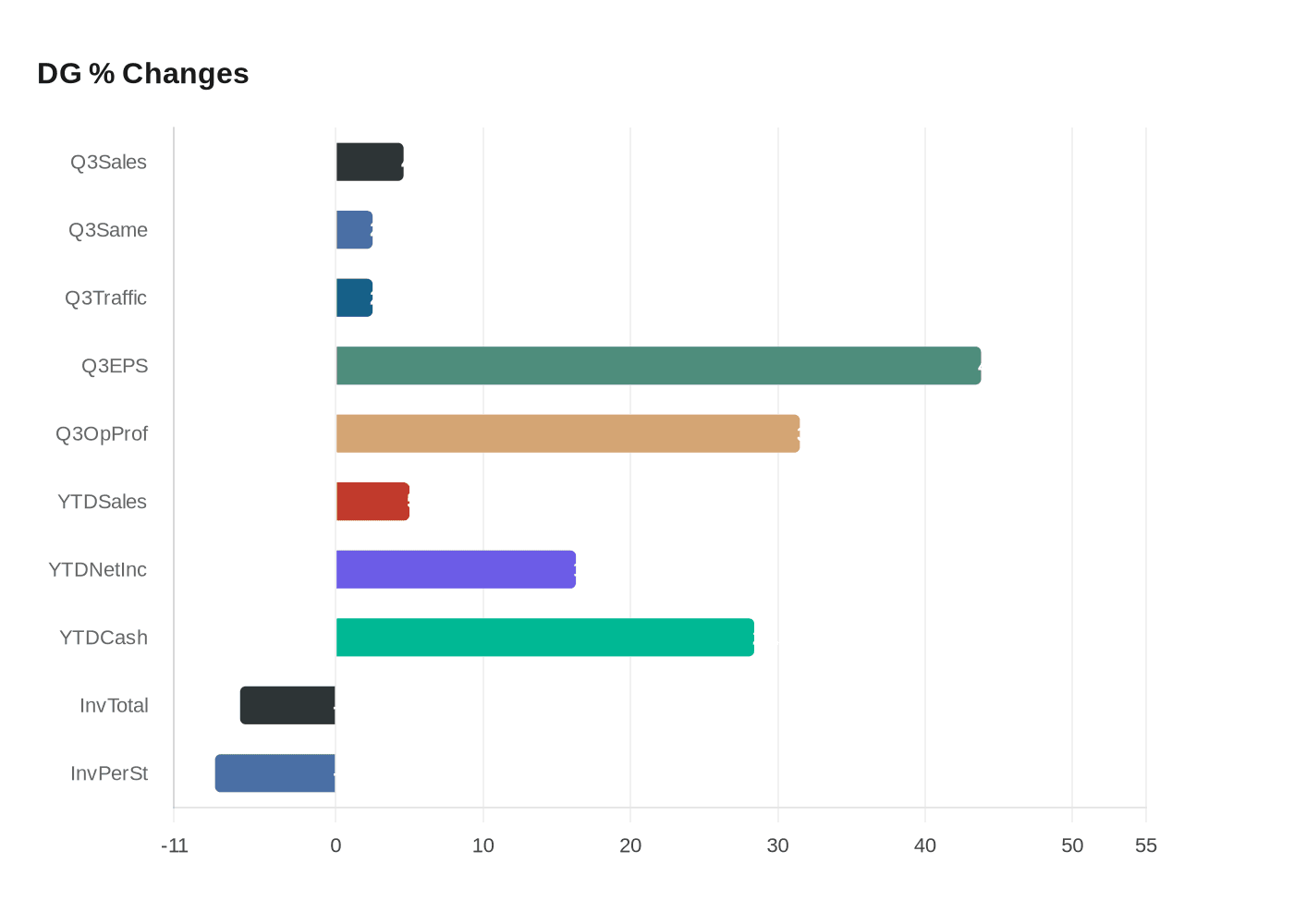

Dollar General heads into an earnings week after Q3 diluted EPS jumped 43.8% to $1.28 and year-to-date net income climbed 16.3% to $1.09 billion.

Dollar General ($DG) is set to report earnings this week alongside Oracle and Adobe, according to an industry brief that flagged the company’s upcoming release. That preview matters because the retailer enters the call off Q3 and year-to-date results that showed sizable margin and cash-flow gains, an unusual combination for a value discounter balancing store growth and inventory tightening.

For Q3 2025 the company reported net sales of $10.65 billion, a 4.6% year-over-year increase driven by new store openings and a 2.5% same-store sales rise with customer traffic also up 2.5%. Profitability metrics showed a sharper move: diluted EPS increased 43.8% to $1.28, net income rose to $282.7 million, and operating profit climbed 31.5% to $425.9 million. Gross profit margin improved by 107 basis points to 29.9%, which the summary attributes mainly to higher inventory markups and lower shrink.

The year-to-date picture through the 39 weeks ended October 31, 2025 paints the broader context analysts will press management on during the call. Net sales grew 5.0% to $31.81 billion, net income increased 16.3% to $1.09 billion, and year-to-date cash flows from operations rose 28.4% to $2.8 billion. Merchandise inventories declined 6.5% to $6.7 billion, with an 8.2% decrease per store, and inventory turnover improved to 4.4 from 4.0 year-over-year.

Operational drivers named in the company’s summary point to where management can be expected to provide color. Digital and delivery initiatives, including partnerships and expanded same-day home delivery, were credited with larger basket sizes and higher customer incrementality. Inventory optimization and SKU rationalization were cited as leading to lower shrink and improved gross margin, while the company flagged “Upside potential for remodel program sales lifts” and a “Retain higher-income customers strategy.” SG&A as a percentage of sales rose 25 basis points to 25.9%, noted as mainly due to higher incentive compensation and maintenance costs.

There is, however, a timing discrepancy readers should note: the industry brief stated Dollar General “is set to report earnings this week,” while the Quartr dataset lists the next Dollar General earnings date as Q4 2026 12 Mar, 2026, a line that appears twice in the excerpt. The Quartr excerpt also includes the odd string “Q3 2026 earnings summary4 Dec, 2025.” Before treating any calendar as definitive, verify the release date and time with Dollar General’s investor relations or an SEC filing.

Quartr’s public summary contains both the financial highlights above and promotional lines, including verbatim headings and copy such as “Partial view of Summaries dataset, powered by Quartr API” and “The #1 app for qualitative research. Live earnings calls, AI chat, transcripts, and more. All for free.” On the call investors and store leaders should listen for management guidance on whether remodel lifts, SKU rationalization and expanded same-day delivery will sustain the margin gains that powered the recent EPS jump, and how SG&A pressures from incentive pay and maintenance will be managed going forward.

Know something we missed? Have a correction or additional information?

Submit a Tip