DroneShield Shares Jump After FY2025 Results, Fueling Military FPV Investment

DroneShield’s FY2025 results show A$216.5m revenue (+276%) and A$210m cash, sparking a share surge and backing A$104m in secured FY2026 orders that could funnel military FPV tech into racing pits.

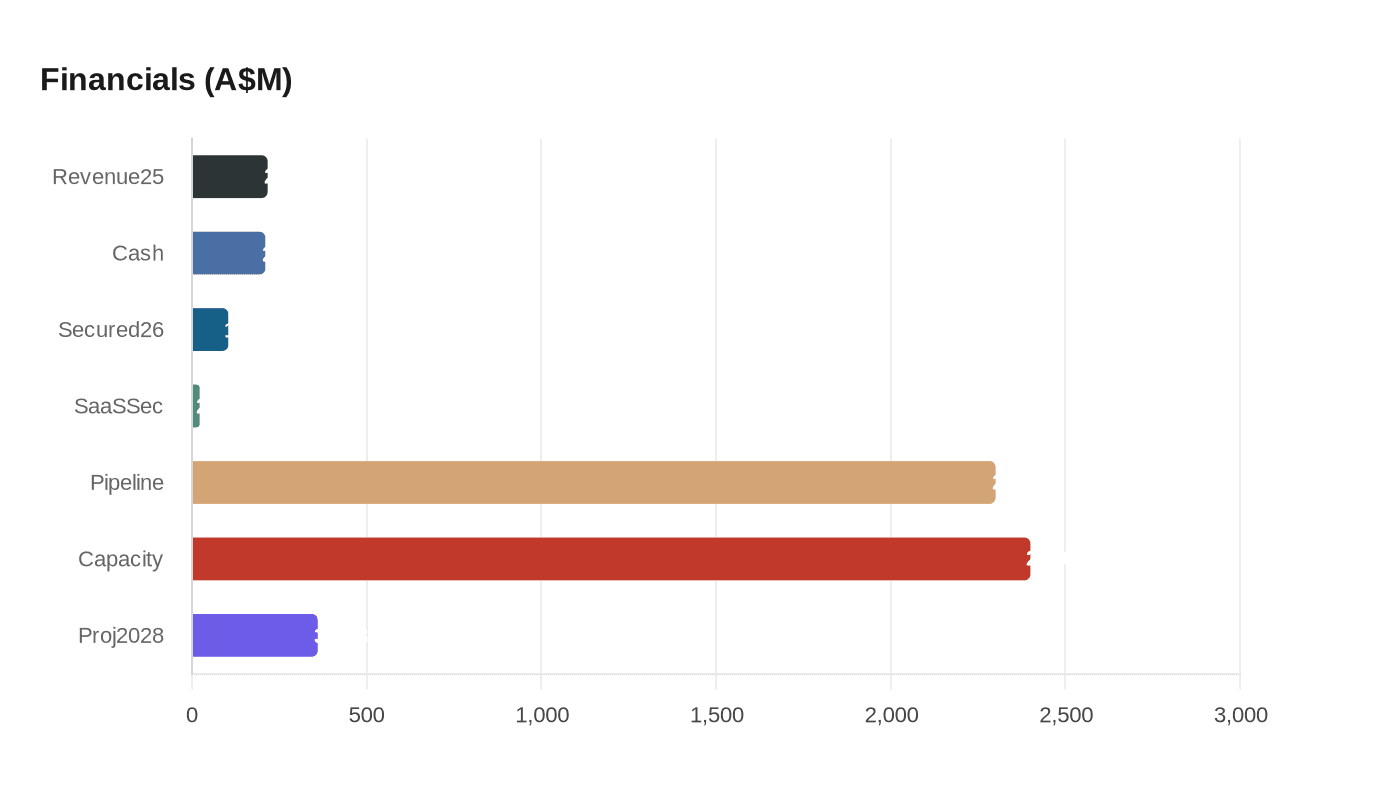

Pilots adjusting goggles this season may feel the trickle of military‑grade FPV hardware into race pits after DroneShield reported FY2025 revenue of A$216.5 million, a year‑on‑year jump of about 276%, and a strengthened balance sheet holding A$210 million in cash and term deposits. The company reported underlying profit before tax of A$33.3 million and three consecutive quarters of positive operating cashflow as at 31 December 2025, facts that underpinned a fresh wave of investor buying.

Markets reacted as the results landed: DroneShield shares have climbed more than 286% year‑on‑year, and intraday snapshots have varied from A$3.01–A$3.09 in late February trading to a capture showing A$4.07 (+10%) on 6 March 2026. The FY2025 disclosure also highlighted SaaS growth — “SaaS revenue was a particular bright spot, climbing 312% to $11.6 million as DroneShield advances its strategic ambition to have software‑as‑a‑service account for 30% of total revenue within five years” — a push that ties software and data back into fast‑moving FPV systems.

Management moved quickly to translate the numbers into forward orders and capacity. Company commentary put FY2026 secured revenue at A$104 million, with A$22 million recognised to date, and secured SaaS at A$22 million with A$2 million recognised so far. At the same time DroneShield laid out an aggressive production scale‑up from a 2025 run rate of A$500 million per year to a target of A$2.4 billion per year by the end of 2026 via new facilities in Australia, the United States and Europe, while analysts point to an enlarged A$2.3 billion sales pipeline that would need conversion to sustain that capacity.

Contract flow has followed the rhetoric. Marketscreener flagged a Feb. 26 package of AU$22 million for dismounted counter‑drone systems and a reported A$21.7 million Western military award the same day, while the company logged quarterly revenue of A$51.3 million in late January. Those wins, coupled with the secured FY2026 backlog, signal more military FPV demand feeding suppliers of tiny high‑bandwidth video systems, low‑latency radios and hardened airframes that race pilots use or adapt.

The corporate recovery has not been linear. A late‑2025 episode of heavy insider selling — CEO Oleg Vornik disposed of roughly 14.8 million performance‑granted shares in early November for about A$49–50 million and executives sold roughly A$70 million in aggregate — and the sudden mid‑November resignation of US CEO Matt McCrann pushed the stock down to about A$1.62. Vornik later described his sell‑off as driven by “a hefty tax bill, an 'out‑of‑control' home renovation, and a general need to secure his financial future.” Governance fixes followed, including mandatory minimum shareholding rules, and on 10 February 2026 DroneShield hired Michael Powell as chief operating officer; Powell brings more than 25 years in defence and aerospace from roles at Thales Australia and Knorr‑Bremse, a hire CEO Oleg Vornik called “instrumental” for disciplined scaling.

Analysts urge caution even as the company plots growth. Simply Wall St’s model projects revenue reaching A$359.8 million and earnings A$96.1 million by 2028, a path that demands roughly 49.7% annual revenue growth and reliable conversion of the reported A$2.3 billion pipeline. For the FPV racing world, the near term is clearer: military demand has bolstered DroneShield’s cash and order book, and that capital and capacity expansion is likely to accelerate technology transfer into civilian FPV systems, supply chains and sponsorship dollars as production ramps toward a A$2.4 billion annual capacity by end‑2026.

Know something we missed? Have a correction or additional information?

Submit a Tip