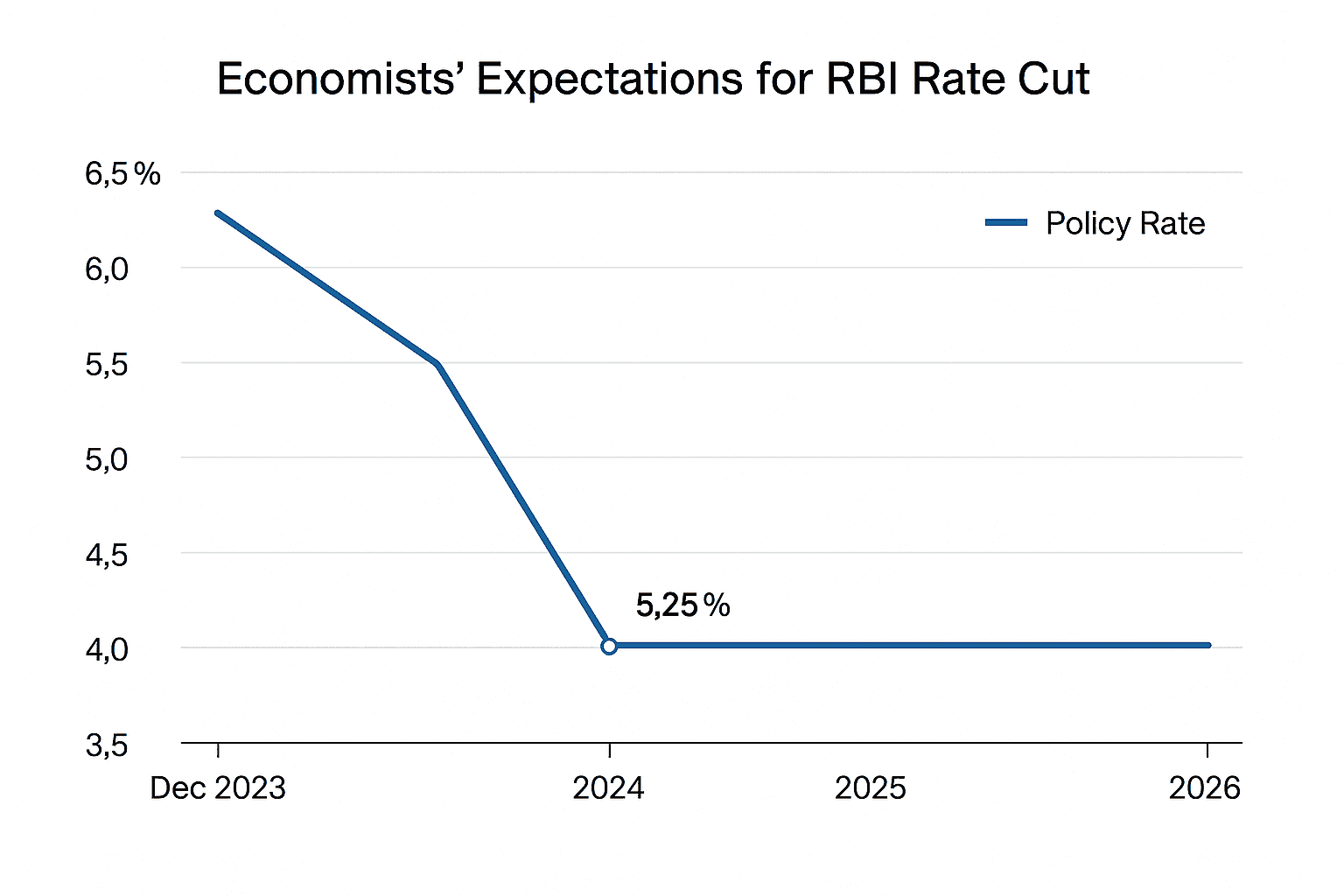

Economists See Reserve Bank Easing to 5.25 Percent in December

A Reuters poll republished November 27 found 62 of 80 economists forecast a 25 basis point cut in the Reserve Bank of India policy repo rate to 5.25 percent at the December 3 to 5 meeting. The consensus cited a marked drop in food inflation and weak consumer demand, while concerns about the rupee and trade barriers were flagged as risks to investor sentiment.

A clear majority of economists expected the Reserve Bank of India to reduce its policy repo rate by 25 basis points to 5.25 percent at the central bank’s December policy meeting, a Reuters poll republished on November 27 showed. The survey of 80 economists, conducted between November 18 and 26, found that 62 respondents or roughly 77.5 percent anticipated an easing, and most forecast the rate would stay at that lower level through 2026.

Economists pointed to a sharp fall in food inflation and historically low headline inflation in October as the primary justification for a near term cut. Those dynamics, coupled with signs of subdued consumer spending, were cited as rationale for shifting the balance of policy toward supporting activity after a period of monetary tightening that aimed to tame price pressures.

Financial markets were already parsing the implications. Expectations of a 25 basis point reduction typically ease short term government bond yields and can lower borrowing costs for households and businesses, supporting consumption and investment. For banks, a cut would put downward pressure on lending rates but could compress net interest margins if deposit costs do not adjust proportionally. For borrowers, especially in the retail and small business segments, marginally lower rates would reduce financing costs and could spur credit demand.

The poll also highlighted two important offsets that could complicate the RBI’s decision and its aftermath. Respondents flagged continued pressure on the rupee and lingering concerns about trade barriers as factors weighing on investor sentiment. A softer currency can feed into imported inflation, particularly via energy and raw material costs, and could force the central bank to tread carefully even as domestic inflation falls. Trade barriers that impair exports or raise input costs can also blunt the positive impact of monetary easing on growth.

Most economists in the survey expected the cut to be a one time easing in December followed by a pause, rather than the start of a sustained easing cycle. That outlook reflects a familiar central bank trade off between bolstering demand now and preserving flexibility to respond to upside inflation surprises or external shocks. With inflation reported at historically low levels in October, the RBI would gain room to act, but currency swings and global tightening or protectionist moves remain tail risks.

Investor flows and bond markets will likely react quickly to any signal of change from the RBI at the December meeting. A confirmed cut could lower yields and support equities in the near term, but persistent rupee weakness or renewed import price pressures could reverse those gains. For households and firms, the immediate benefit would be cheaper credit, while the longer term trajectory of rates will depend on whether domestic demand strengthens and on the evolution of external price pressures during 2026.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?