European Shares Open 2026 at Record Highs Led by Defence Stocks

European equities kicked off 2026 with fresh record highs as the STOXX 600 rose in early trading and defence stocks outperformed, reflecting persistent geopolitical concerns. The move builds on a strong 2025 rally and leaves investors watching macro data and the U.S. interest-rate outlook for direction in a market trading with light volumes.

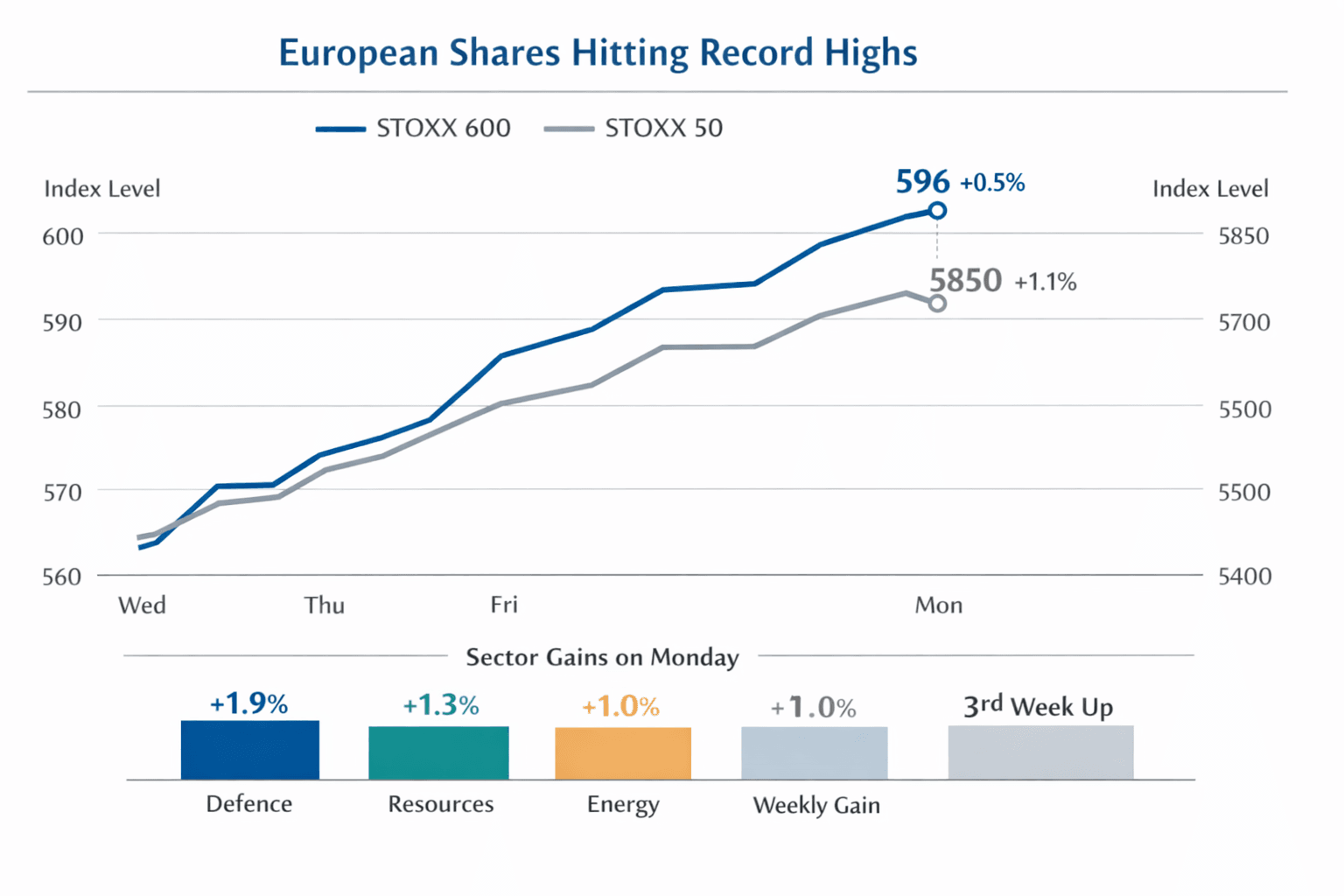

European equities surged in early trading on Jan. 2, 2026, with the pan-European STOXX 600 reaching record levels as investors returned from New Year holidays. By 0820 GMT the STOXX 600 was up about 0.4%, while a separate intraday snapshot put the index 0.5% higher at a record 596 points. The larger-cap STOXX 50 climbed roughly 1.1% to an all-time high near 5,850, placing the market on track for a third consecutive weekly advance.

Sector moves were skewed toward defence and commodity-linked names. Defence shares led gains within the STOXX 600, rising around 1.9%, supported by continued geopolitical tensions and expectations of increased military spending across Europe and allied nations. Basic resources and energy stocks also showed strength, with basic-resources up roughly 1.3% and the energy index advancing near 1.0%. Consumer-related shares lagged, slipping about 0.2% in early trade.

Bourses across the region were mostly higher, though national index moves varied by venue and by the precise intraday snapshot. Trading volumes were generally thin as market participation picked up after the holiday break, and Switzerland’s market remained closed for the holiday and was scheduled to reopen later in the week. Intraday index readings differed modestly across data feeds and timestamps, reflecting the fragmented picture of early-session activity.

The strong start to 2026 follows a robust 2025 for European equities. The STOXX 50 rose about 18% in 2025 while the STOXX 600 gained roughly 17%, their best annual showings since 2021. Analysts and market participants point to several drivers of that rally: falling interest-rate expectations that lifted valuations, Germany’s fiscal support measures that buoyed regional growth prospects, and a rotation out of richly valued U.S. technology stocks into more cyclical and value-oriented sectors in Europe. Markets also recovered from a volatile April 2025 when tariff actions triggered a sell-off, underscoring how policy shocks can quickly reshape sentiment.

Near-term risks and catalysts are concentrated in macro data and central-bank guidance. A euro-zone purchasing managers’ index reading was due at 0900 GMT and was flagged by traders as an immediate sentiment test. More broadly, investors remain focused on the U.S. interest-rate outlook; any indication that Federal Reserve policy will be tighter than priced could translate into rapid re-rating across European equities, especially for rate-sensitive sectors.

The current pattern suggests cautious optimism: the rally has momentum, but thin volumes and data sensitivity leave markets prone to sharper moves on mixed economic prints or abrupt geopolitical developments. For the moment, defence and commodity-related stocks are the chief beneficiaries of that environment, while consumer names remain vulnerable until clearer evidence of sustained demand growth emerges.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?