Federal Regulators to Propose Winter Revisions to EV Sales Mandate

Federal officials say they will unveil proposed changes to the electric-vehicle sales mandate this winter, a move aimed at rebalancing climate goals with a cooling market after federal tax credits expired. The announcement could reshape automakers’ production plans, dealer economics and the pace of decarbonization across the U.S. auto sector.

Federal regulators plan to unveil proposed changes to the nation’s electric-vehicle sales mandate this winter, officials said, signaling a potential recalibration of policies designed to accelerate the auto sector’s transition away from internal-combustion vehicles. The timing comes as consumer demand for EVs softens and industry stakeholders press for a more flexible compliance framework.

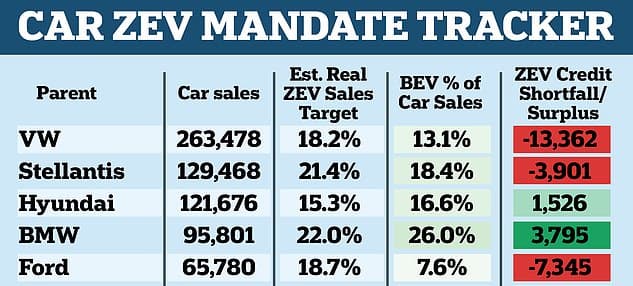

Market indicators underscore the fragility of near-term EV demand. Industry forecasters from J.D. Power-GlobalData and Cox Automotive projected the overall U.S. auto market would fall between 3 percent and 6.9 percent in October, a pullback the firms attributed in part to the expiration of federal EV tax credits. The sales data for October showed a mixed picture across manufacturers: Toyota, Ford, Honda and Kia recorded volume gains while Hyundai, Subaru and Mazda experienced declines. Those shifts complicate manufacturers’ capacity to meet rigid, rising EV targets without incurring steep compliance costs.

Dealers and some automakers have been vocal about the economic strains from sharply escalating EV targets and related compliance mechanisms. Nissan dealers have complained that stair-step targets are “unattainable,” according to reporting on dealer reactions, illustrating the friction between production mandates and retail realities. Suppliers are also watching closely; production shifts tied to rapid electrification have knock-on effects throughout supply chains and regional economies. Meanwhile, broader trade and policy factors, including an upcoming 2026 review of the USMCA trade agreement, add uncertainty to North American sourcing and supplier strategies.

The administration’s proposed changes are likely to address several recurring themes in industry and policy debates: the pace of mandated EV shares, flexibilities for automakers through credit trading or off-ramps, carve-outs for affordability or plug-in hybrids, and recognition of infrastructure and charging deployment as constraints on consumer adoption. Adjustments could also reflect recent market behavior after incentive changes, with regulators balancing emissions reduction targets against consumer choice and economic disruption.

For automakers, the proposal’s contours will shape capital allocation plans already committed to battery factories, powertrain retooling and technology investments. A tighter or more prescriptive mandate could force additional investments and accelerate retirements of combustion platforms; a looser or more flexible approach could alleviate near-term dealer and supplier pressures but slow the pace of fleet emissions reductions. Lenders and residual-value analysts will watch closely, since shifts in mandated EV shares affect resale values, lease pricing and credit availability.

Longer term, most analysts maintain that electrification is the dominant structural trend for the auto industry, driven by falling battery costs, regulatory pressure globally and automakers’ own commitments. But the winter proposal underscores that the pathway and timeline remain politically and economically negotiable. The next regulatory steps, proposal release, formal comment period and eventual final rulemaking, will be a critical test of whether policy can adapt to market volatility while preserving decarbonization objectives.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?