Four mortgage rate dos and don'ts for borrowers in today’s market

At 6.48%, small rate mistakes get expensive fast. The smartest borrowers shop against benchmarks, lock with care and avoid points or refi bets that may not pay off.

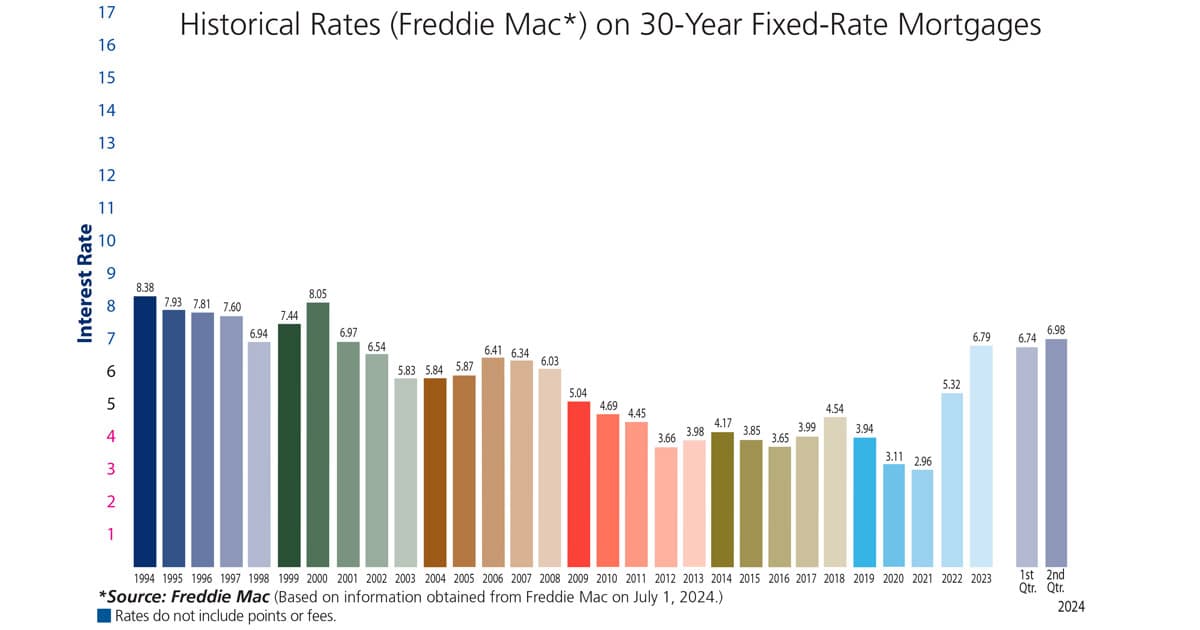

Mortgage shoppers are still facing a market where every eighth of a point matters. Freddie Mac’s latest weekly reading put the 30-year fixed rate at 6.48%, far above the pandemic-era lows and high enough to keep payments sticky for buyers who are already stretching for affordability. That is why today’s winning strategy is not guesswork, but disciplined tradeoffs: compare offers, understand lock terms, test the math on points and avoid assuming a better refinance will magically appear later.

Shop every rate against a benchmark

The first smart move is to compare multiple offers against a neutral benchmark instead of anchoring on the first quote that sounds attractive. The Consumer Financial Protection Bureau tells borrowers to check Freddie Mac’s average mortgage rates while shopping, and its examples assume a $400,000 single-family primary residence, a 10% down payment, a 700 credit score, a conventional loan, a 30-year fixed term and a 60-day rate lock. Those assumptions matter because they give you a clean baseline for judging whether a lender’s pricing is competitive or just dressed up with fine print.

The payment difference can be meaningful even when the rate spread looks small. On a $400,000 home with 10% down, the loan amount is $360,000, and a 30-year mortgage at 6.48% comes out to about $2,271 a month in principal and interest. At 7.0%, that rises to about $2,395, or roughly $124 more each month. Over years, that gap can reshape how much room you have for insurance, maintenance, childcare or retirement saving, which is why borrowers should treat rate shopping as part of the household budget, not just a closing-day tactic.

The broader market makes that discipline even more important. Freddie Mac says pending home sales have increased three months in a row, a sign that demand is waiting on the sidelines for rates to ease. The National Association of Realtors has said a drop toward 6% could pull some buyers back into the market, and that possibility reinforces the value of comparing offers now rather than hoping the market will hand you a better deal later.

Treat a rate lock as protection, not a promise

A rate lock is useful because mortgage prices can change fast. The CFPB says rates can move daily, sometimes hourly, and a lock means your interest rate will not change between the offer and closing if you close within the agreed time frame and nothing changes in your application. The Federal Reserve adds that a lock can cover not only the interest rate but also a certain number of points, so the lender is promising more than a single number on a worksheet.

That protection only works if you understand the clock. Lock periods are commonly 15 to 60 days, and if the closing runs late, extending the lock can cost extra. For borrowers juggling inspections, appraisal delays or underwriting requests, that can turn a well-priced loan into a more expensive one if the paperwork drags on. The practical takeaway is simple: lock when you are ready to move, not when you are merely optimistic.

There is also a behavioral payoff to locking with purpose. In a market shaped by the mortgage lock-in effect, the gap between old homeowner loans and new mortgage rates has already reduced mobility and discouraged moving, according to the Federal Housing Finance Agency. Researchers cited in later analysis said the effect prevented 1.33 million sales between 2022Q2 and 2023Q4, and the Philadelphia Fed said there has "never been such a huge gap" between current homeowner rates and prevailing new mortgage rates. If you are buying in that environment, a lock helps you protect the loan you negotiated from becoming a moving target.

Do the math before buying discount points

Discount points can be smart in the right case, but they are not automatically worth the upfront cash. Freddie Mac says one discount point equals 1% of the loan amount, or $1,000 per $100,000 borrowed, paid at closing in exchange for a lower interest rate. On a $360,000 loan, one point costs $3,600 before you see a penny of interest savings, and the size of the rate cut depends on the lender and the loan.

That is why the break-even period should drive the decision. If you expect to stay in the home long enough to recover the upfront cost through lower monthly payments, points may make sense. If you might sell, move, or refinance in a few years, the points can become prepaid interest you never fully earn back. In a market where cash is already tight, that matters because every dollar spent on points is a dollar not available for closing costs, moving expenses, emergency reserves or a larger down payment.

For borrowers comparing the emotional appeal of a lower monthly payment with the reality of closing cash, the right question is not "Can I afford the point?" It is "Will I still live in this loan long enough to get my money back?" That shift in framing can prevent a cheap-looking rate from turning into a costly shortcut.

Do not assume refinancing will rescue you later

The riskiest mistake is treating a future refinance like an insurance policy. The FDIC warns borrowers not to count on being able to refinance into a lower-rate fixed mortgage later, because personal finances can change and a lower-rate refi may not be available when rates finally fall. Income can tighten, credit scores can slip, home values can soften or underwriting standards can get stricter exactly when you hoped to improve your terms.

That reality should change how you choose the first loan. If a payment is only comfortable under a best-case refinance scenario, the mortgage is too thin for the life you are actually living now. A safer approach is to buy a home you can carry at today’s rate, with a structure you can live with if rates stay higher for longer, even as the market slowly normalizes.

The latest data suggest that buyers are already waiting for a better entry point, but waiting is not the same as planning. If rates ease closer to 6%, more sidelined borrowers may re-enter the market, and that could improve liquidity for both buyers and sellers. Until then, the most durable strategy is to control what you can control: compare offers, lock deliberately, scrutinize points and refuse to build your homeownership plan around a refinance that may never arrive.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip