Gilead to buy Arcellx for $115 per share, deal implies $7.8 billion

Gilead agreed to acquire Arcellx for $115 cash plus a $5 contingent value right, giving it full control of a late‑stage CAR‑T program and an implied $7.8B valuation.

Gilead Sciences said it will acquire clinical‑stage biotech Arcellx for $115 per share in cash at closing plus one contingent value right worth $5 per share, an arrangement the company described as “an implied equity value of $7.8 billion payable at closing.” The transaction, announced Feb. 23, 2026, hands Gilead full control of Arcellx’s investigational BCMA‑directed CAR‑T therapy anitocabtagene autoleucel, known as anito‑cel, and the broader D‑Domain CAR platform.

Under terms outlined by analysts, the $5 CVR is tied to commercial milestones and will pay out only if anito‑cel achieves $6.0 billion in cumulative global sales by year‑end 2029. Stocktitan described the structure as a way to “share commercial risk between Gilead and Arcellx shareholders while preserving headline premium economics,” and framed the acquisition as a “multibillion‑dollar bet to own a late‑stage multiple myeloma cell therapy platform outright.”

The deal converts an existing co‑development and co‑commercialization relationship between Arcellx and Kite, a Gilead company, into outright ownership. Observers said the move accelerates Gilead’s path to control development and commercialization and eliminates ongoing profit‑share arrangements, milestones and royalty obligations tied to the program.

Anito‑cel’s regulatory timetable makes the asset especially valuable. The biologics license application for anito‑cel has been accepted by regulators, with an anticipated PDUFA action date of Dec. 23, 2026, and the application is supported by Phase 1 data and the pivotal Phase 2 iMMagine1 study. If approved, the therapy would be positioned as a fourth‑line option for relapsed or refractory multiple myeloma, a disease where patients often exhaust effective treatments and face diminishing responses over successive lines of therapy.

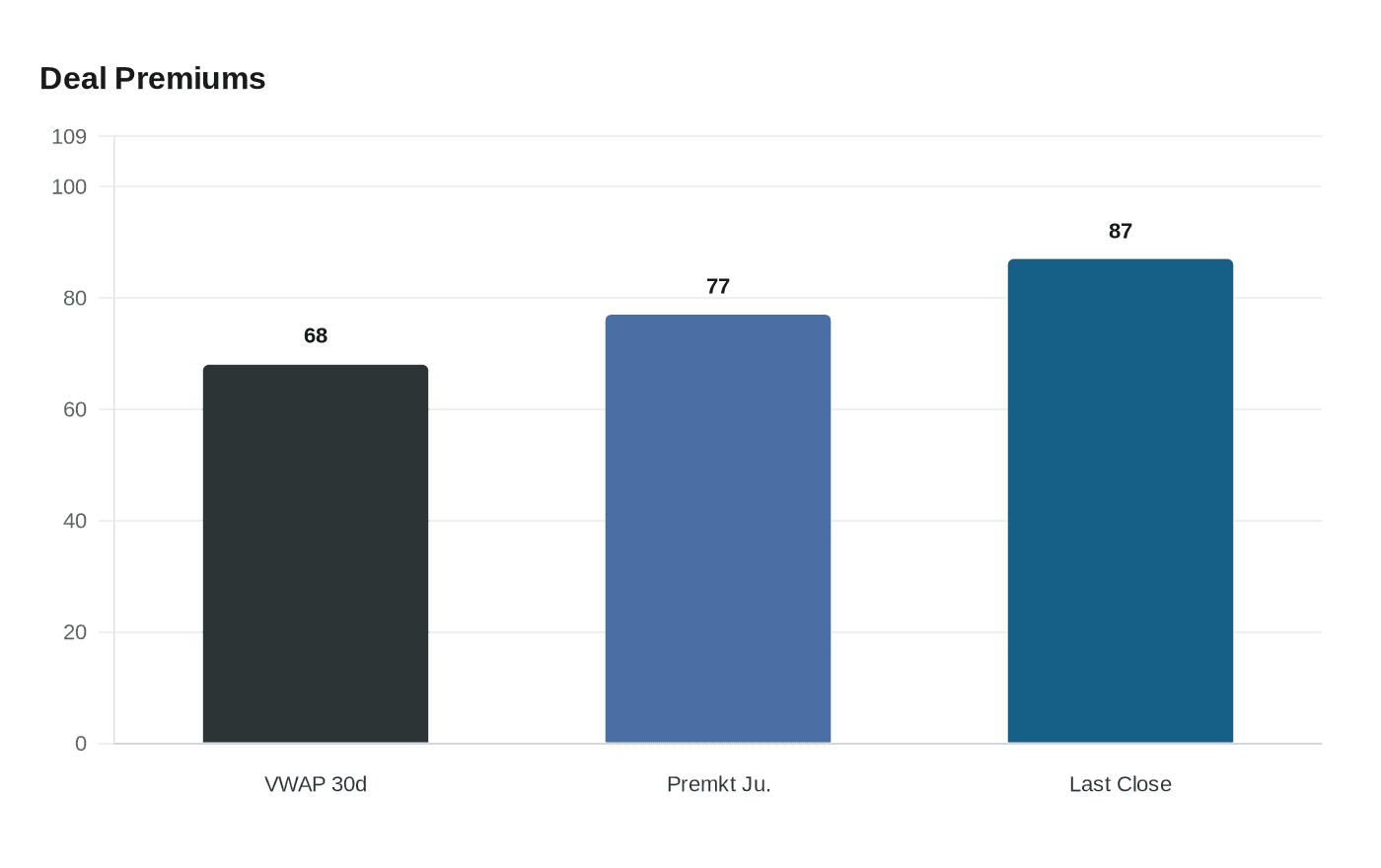

Markets reacted sharply. Arcellx shares jumped roughly 77 to 78 percent in premarket trading to about $114, while Gilead shares were reported down about 0.8 percent in one snapshot. Commentators noted different measures of the deal premium: Stocktitan calculated a 68 percent premium to Arcellx’s 30‑day volume‑weighted average price through Feb. 20, 2026, while comparisons to the stock’s last close produced an 87 percent premium.

Analysts cited potential near‑term financial effects. Stocktitan expects the acquisition to be accretive to Gilead’s earnings per share from 2028 onward contingent on FDA approval, a projection that hinges on both regulatory success and commercial uptake of anito‑cel. For shareholders and patients, the most important upcoming milestones are the FDA decision in December and early commercial sales that will determine whether the CVR pays out.

The deal underscores a continuing industry trend of large pharmaceutical companies buying late‑stage cell therapy assets to secure proprietary platforms and streamline commercialization. The immediate lines of inquiry for investors and regulators will include the accounting treatment of the CVR, integration of Kite’s role into Gilead’s commercial plans, and monitoring clinical and sales trajectories toward the CVR threshold.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?