Home Depot Issues Cautious Fiscal 2026 Outlook, Sees Market Recovery

Home Depot issued a cautious preliminary fiscal 2026 outlook while reaffirming fiscal 2025 guidance, citing only a modest housing recovery that matters for store staffing and contractor demand.

Home Depot framed its outlook for the year ahead as restrained even as its Pro Forecast points to early signs of a housing-market rebound that could lift building jobs and contractor activity. The company reaffirmed its full-year guidance for fiscal 2025 while setting a preliminary fiscal 2026 outlook that officials described as cautious.

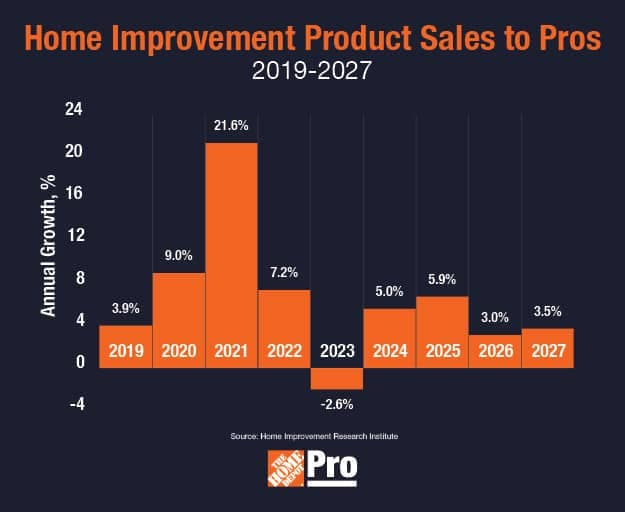

The Home Depot Pro Forecast (January 2026) notes a modest recovery in housing next year, with single-family housing starts expected to gain 3.1% in 2026 after a 4.3% drop in 2025, which signals a rise in building jobs. The forecast is presented specifically as a summary of macro and industry expectations that affect the company’s frontline workforce and contractor customers, and it highlights continued remodeling demand in certain product categories.

Financial details in a republished analyst excerpt portray a mixed picture for store-level economics and corporate plans. The report states that diluted earnings per share are projected to decline by 6% from $14.91 in fiscal 2024, while capital expenditure is set at 2.5% of total sales. It also says, “Operating profit would be expected to grow at a faster rate than sales, and diluted earnings per share to rise in mid-to-high-single-digits.” That passage contains apparently conflicting EPS language that has not been reconciled in the excerpts provided.

Analyst scenario language underscores the conditional nature of the outlook. “In our accelerated recovery case, we could see sales and earnings per share grow faster in the event of a sharper housing recovery,” the report notes, signaling that upside depends on a stronger-than-expected rebound in homebuilding and remodeling.

Market reaction was muted. “Home Depot stock ((HD) gained roughly 1% last week, remaining within its recent trading range near prior highs following mixed company and regulatory news,” market commentary observed, adding that “Home Depot stock valuation reflects execution risk and sensitivity to housing, spending cycles, and margins, meaning outcomes may vary despite stable long-term fundamentals.”

What this means for workers and workplace dynamics is concrete but gradual. A 3.1% lift in single-family starts points to more building and renovation work for contractors who buy materials at Home Depot and to steadier demand for in-store associates who support pro customers. At the same time, the company’s cautious tone and the mixed EPS signals suggest management is planning conservatively on hiring, store hours, and capital projects until recovery proves stronger.

Employees and contractor customers should watch for the company’s full corporate and investor materials for clarified EPS guidance, the final list of product categories showing remodeling demand, and any regional staffing changes tied to local housing activity. The pace of the housing recovery will determine whether the preliminary caution turns into tangible hiring and margin expansion or a longer period of tightened planning.

Know something we missed? Have a correction or additional information?

Submit a Tip