How much $8,000 earns in CDs versus high-yield savings accounts

An $8,000 deposit can earn almost the same headline return in a top CD or savings account, but liquidity and rate lock decide which one really wins.

An $8,000 deposit can land in nearly the same place on paper in a top high-yield savings account or a top one-year CD. The real difference is not just the APY, but whether you want cash you can reach at any moment or a fixed rate you can count on for the full term.

What $8,000 earns at current rates

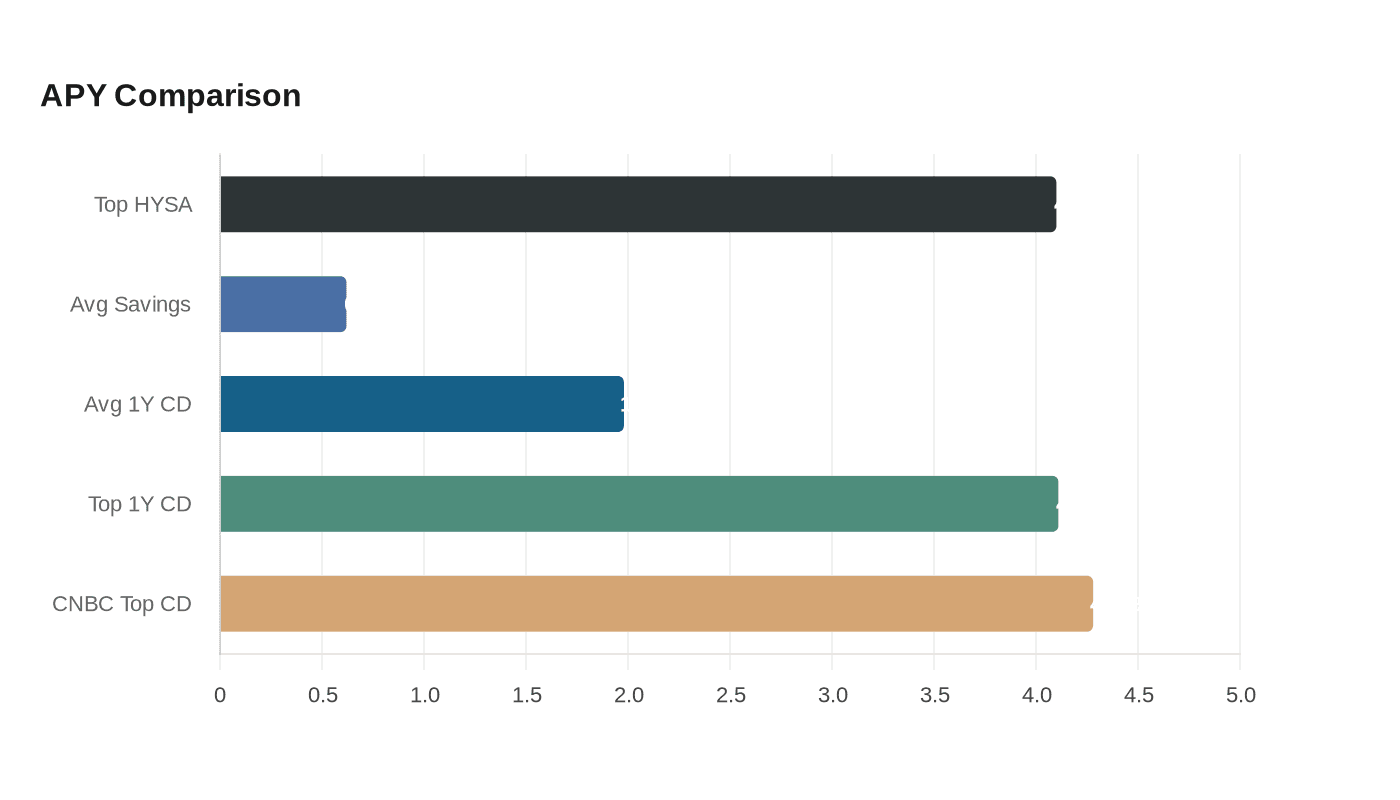

At Bankrate’s top high-yield savings rate of 4.10% APY, $8,000 would earn about $328 over one year if the rate held. That is a strong return for money that stays accessible, especially compared with the national average savings rate of 0.62% APY, which would produce only about $49.60 on the same balance.

The CD side of the market looks similar at the top end, but much weaker on average. Bankrate says the national average APY for one-year CDs is 1.98% as of June 9, 2026, which would generate about $158.40 on $8,000 over a year. Bankrate’s top tracked one-year CD rate is 4.11% APY from Popular Direct, which would earn about $328.80, and CNBC reported top one-year CD rates as high as 4.28% APY, or roughly $342.40 on the same deposit.

That spread matters because it shows how much saver behavior changes the outcome. A depositor who is content to leave money alone for 12 months can capture a fixed return in the same neighborhood as the best savings account. A depositor who needs flexibility may accept a slightly lower or variable return in exchange for easier access to cash.

Why the winner changes with your timeline

If your $8,000 is part emergency fund and part short-term savings, a high-yield savings account has the edge because it keeps the money liquid. You can move quickly if the car breaks down, a tax bill arrives, or a medical expense comes up. In that case, a few dollars of extra interest matter less than the ability to use the funds without paying to get them back.

If your $8,000 is money you can truly set aside, a CD can be the smarter bet because it locks in the rate. That protection becomes more valuable if savings rates fall after you open the account. A high-yield savings account can start at 4.10% and drift lower over the year, while a one-year CD preserves the original rate for the full term. If that happens, the CD can finish ahead even when the starting yields look similar.

That is the core saver trade-off: liquidity versus certainty. A high-yield savings account gives you agility, but its rate can move. A CD gives you a known payoff, but only if you can live without the cash until maturity.

How penalties change the math

CDs are not just savings accounts with a timer attached. The Consumer Financial Protection Bureau says Regulation DD helps consumers comparison-shop for deposit accounts, and it notes that CDs generally require keeping money deposited for a specified length of time. Withdraw early, and you usually face a penalty.

That penalty is the hidden cost that can erase the advantage of a CD if you guess wrong about your cash needs. An account that pays 4.11% APY is attractive only when the money stays put. If you break the CD before maturity, your return can shrink fast, which is why the best CD is not always the best choice for a saver who may need the funds soon.

High-yield savings accounts avoid that trap. They are more forgiving when life changes, which is why they often make sense for emergency savings and near-term expenses. CDs are better suited to money that can sit untouched for the full term without anxiety.

The market is still rewarding comparison shoppers

The current market also shows how wide the gap is between average yields and the best offers. Bankrate says the national average savings rate is 0.62% APY, while the top high-yield savings rate is 4.10% APY, around six times higher. On the CD side, the national average one-year rate is 1.98% APY, but the best advertised rates are more than twice that, reaching 4.11% at Bankrate’s top tracked offer and up to 4.28% in CNBC’s reporting.

FDIC national rate data reinforce the same point. The agency said the 12-month CD national average was 1.55% in May 2026, which is even lower than the 1.98% one-year CD average Bankrate cited for June 9, 2026. The message for savers is clear: the average account will not earn nearly as much as the best account, so the comparison step matters as much as the deposit itself.

The Consumer Financial Protection Bureau’s Regulation DD is designed to help with exactly that, because deposit accounts can look similar on the surface while paying very different yields. The strongest returns are available, but only to savers who shop around and accept the rules that come with each product.

Safety is not the deciding factor, access is

Both CDs and high-yield savings accounts are low-risk choices for many savers because FDIC insurance protects deposits up to at least $250,000 per depositor, per insured bank, per ownership category. That means the real decision is usually not about safety in the credit-risk sense. It is about behavior, timing, and whether you are likely to need the money before the term ends.

For a one-year horizon, the numbers are close enough that flexibility can matter more than a slight APY edge. If you want maximum access, a top high-yield savings account can earn about $328 on $8,000 at 4.10% APY while leaving your cash reachable. If you can commit to a full year without touching the money, a top CD at 4.11% APY can deliver essentially the same return, and a 4.28% rate can do a bit better, but only if you avoid early withdrawal altogether.

For savers, the best choice is the one that matches the money’s job. Cash you may need soon belongs in the more flexible account. Cash you can truly lock away can be worth fixing at a CD rate before the market has a chance to move against you.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip