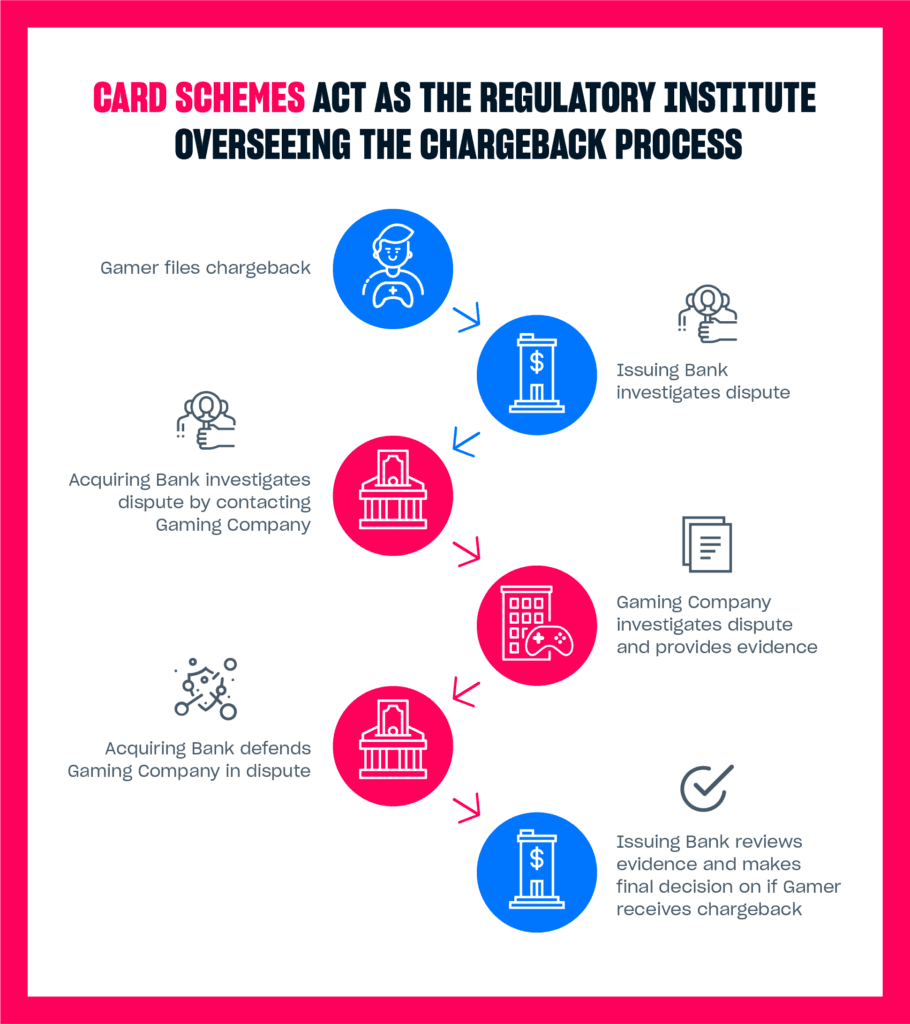

How to Spot and Dispute Unauthorized Mobile Game Charges Quickly

Spot unauthorized mobile‑game charges fast, call your card issuer, report the bank, send a written dispute, and follow the checklist below to protect liability under FCBA/EFTA.

This evergreen guide consolidates authoritative, player-focused steps for spotting, reporting, and disputing unauthorized charges tied to mobile games, including purchases through PayPal, Google Play, and Apple’s App Store. It’s written as a utility-first checklist players"

1. Confirm the charge and document it immediately

Check your transaction history in the app store or payment service and on your bank/credit card statement as soon as you notice an unexpected charge. “Monitor your account activity. Monitor your account activity regularly either online or by reviewing your monthly statements and report any unauthorized transactions right away.” Take screenshots of the transaction, note dates, amounts, merchant names (for example, Google Play, Apple’s App Store, or PayPal), and log when you first saw the charge so you have a timeline for disputes.

2. Report the theft to your card issuer as quickly as possible

“Report the theft of this information to the card issuer as quickly as possible: Many companies have toll-free numbers and 24-hour service to deal with such emergencies.” Call your card issuer right away to flag the charge, freeze the card, or request a replacement number. During the call make sure to get a reference number or case ID and the name of the representative; that record will help if you need to escalate or follow up in writing.

3. Report the theft to your bank if a debit/ATM account is affected

“Report the theft of this information to the bank as quickly as possible.” If the unauthorized charge hit your debit account, contact your bank's fraud department immediately, debit/ATM liability depends on reporting speed. Remember the source warning: “You risk unlimited loss if you fail to report an unauthorized transfer within 60 day after your bank statement containing unauthorized use is mailed to you,” so act fast once the statement with the charge is available.

4. Review statements and send a written dispute for each questionable charge

“Review your billing statements carefully after the loss: If they show any unauthorized charges, it's best to send a letter to the card issuer describing each questionable charge.” A written dispute creates a formal record that card issuers and banks use in investigations; list each charge by date and amount and include any supporting documentation. The source explicitly recommends sending a letter, so follow that step in addition to any phone report, keep copies of everything you send and note delivery dates.

5. Cancel compromised accounts and open new ones when necessary

“Cancel your account and open a new one.” If a payment method or in-game account has been compromised, close it and replace it with a fresh account or payment token where possible. The research note doesn’t specify whether this refers to game accounts, payment accounts, or both, so treat this as an instruction to evaluate both: cancel or replace compromised cards and consider changing or locking the game account until you’ve secured it.

6. Know your legal exposure under FCBA and EFTA

The guidance spells out federal law limits you should know right away: “Your maximum liability under federal law for unauthorized use of your credit card is $50.” It also says, “If the loss involves your credit card number, but not the card itself, you have no liability for unauthorized use.” For debit cards and ATM transfers, “Your liability under federal law for unauthorized use of your ATM or debit card depends on how quickly you report the loss.” These are the exact statutory framings given in the source; verify timelines with your issuer but act promptly to preserve consumer protections.

7. Use secure devices for follow-up and future purchases

“Use secured computers. When performing financial transactions, using secured computers whenever possible, such as your home or work computer will be safer than using publicly available computers.” After spotting fraud, avoid public Wi‑Fi or shared machines when you call, change passwords, or submit disputes. Move future purchases to secured devices, enable device locks, and use network protections to reduce the chance of repeat theft.

8. Monitor accounts continuously and reassess risk regularly

The source urges you to “Monitor your account activity. Monitor your account activity regularly either online or by reviewing your monthly statements and report any unauthorized transactions right away.” It additionally recommends to “Assess your risk. We recommend periodically assessing your online banking risk and put into place increased security controls where weaknesses are found; particularly for members with business accounts. Some items to consider when assessing your online banking risk are:”, the source does not include the continued list. Make monitoring a recurring habit and escalate security controls where needed, especially for anyone linking business accounts to payment methods.

9. Remember platform coverage, PayPal, Google Play, Apple’s App Store

The guide scope explicitly includes purchases through PayPal, Google Play, and Apple’s App Store, so check each platform’s help and purchase history immediately. The supplied material names those platforms but does not provide platform-specific steps; you should call your card issuer and bank first (per the source), then follow each platform’s dispute or refund process after flagging the charges to your financial institution.

10. What the source flags as missing and what you should follow up on

The research notes identify clear gaps you should be aware of: the excerpt leaves out platform‑specific dispute flows for PayPal, Google Play, and Apple’s App Store; it ends a sentence fragment (“It’s written as a utility-first checklist players”) and truncates the list after “Some items to consider when assessing your online banking risk are:”. The guide also does not provide issuer phone numbers, sample dispute letters, or certified-mail recommendations, these are follow-ups to collect before you finish any formal dispute package.

- Call your card issuer and report the theft, “Report the theft of this information to the card issuer as quickly as possible.”

- Freeze or replace the compromised card and ask for a case reference (many issuers have “toll-free numbers and 24-hour service”).

- Report the issue to your bank if funds were debited, “Report the theft of this information to the bank as quickly as possible.”

- Review statements and “send a letter to the card issuer describing each questionable charge.”

- Cancel and replace compromised accounts: “Cancel your account and open a new one.”

11. Quick "do this now" checklist (actions you can take in the next hour)

Acting quickly preserves legal protections and limits liability under the federal rules cited in the guidance.

Closing note, what to watch for next This checklist pulls only the explicit steps and legal framings present in the source material; the key takeaways are urgent: report thefts “as quickly as possible,” document charges in writing, and be aware of the FCBA/EFTA liability language, $50 maximum for most unauthorized credit card use and the 60‑day debit/ATM reporting risk. I’ll be tracking platform-specific dispute flows and issuer contact details so you can follow up, but for now, call your issuer and bank, document everything, and send that written dispute.

Know something we missed? Have a correction or additional information?

Submit a Tip