India’s Economy Set for 7.4% Growth in FY2025-26

India’s National Statistics Office released a first advance estimate projecting real GDP growth of 7.4% for fiscal year 2025-26, a pace driven by private consumption, investment and a strong services sector. The upward revisions from the RBI and ADB reinforce domestic momentum but raise fiscal questions for Budget 2026 amid subdued inflation and potential external headwinds.

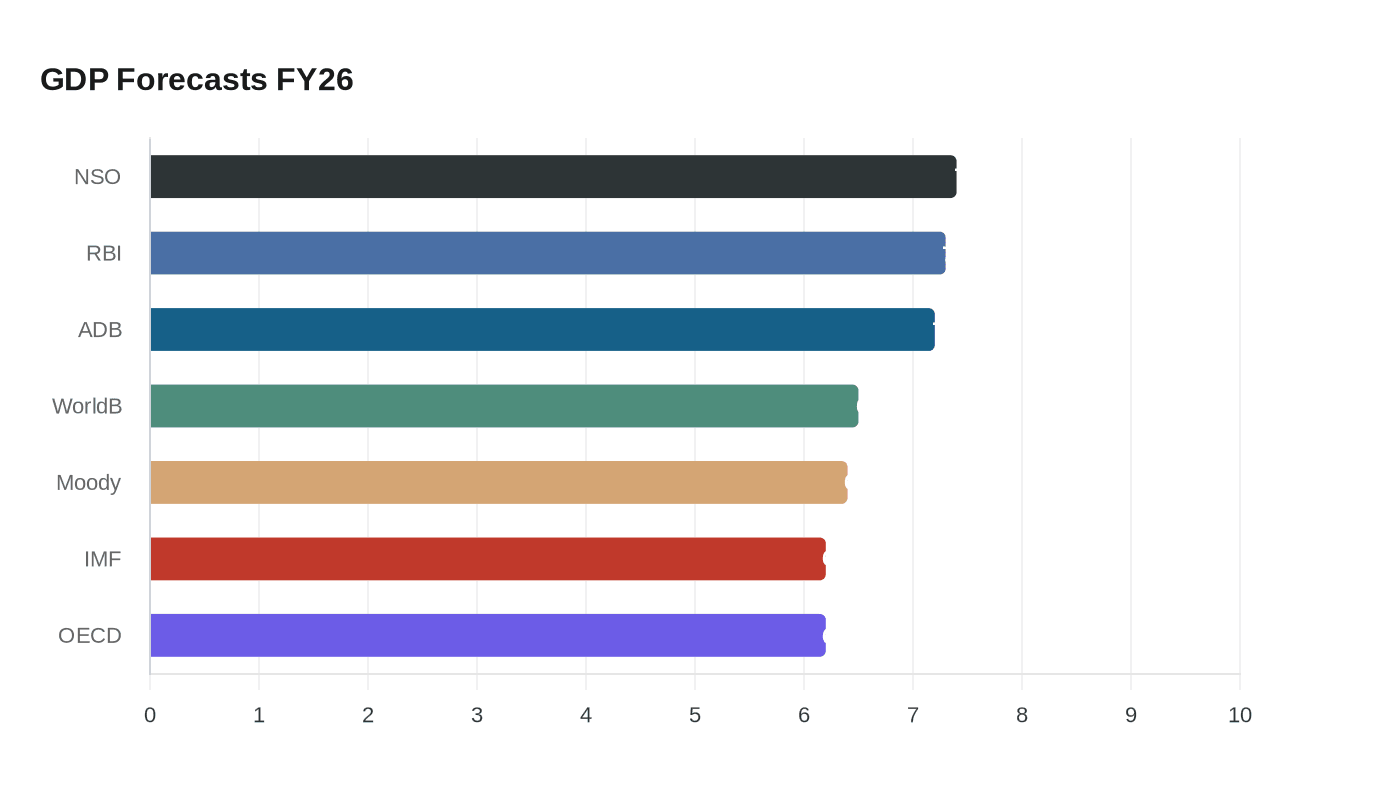

India's National Statistics Office, under the Ministry of Statistics and Programme Implementation, released a first advance estimate on Jan. 7, 2026, projecting real GDP growth of 7.4% for the fiscal year ending March 31, 2026. The NSO described the expansion as being supported primarily by private consumption and investment, with the estimate to be revised as more quarterly and sectoral data become available.

The NSO figure has been broadly endorsed by other credible forecasters. The Reserve Bank of India revised its own FY2025-26 forecast up to 7.3% from 6.8% in its December 2025 review, while the Asian Development Bank lifted its outlook to 7.2% from 6.5%, citing an approximately 8% expansion in the first half of the fiscal year. Several international institutions remain more conservative, clustering in the mid-6% range: the World Bank at 6.5% for 2026, Moody’s at 6.4% for 2026 and 6.5% for 2027, the IMF at 6.6% for 2025 and 6.2% for 2026, and the OECD at 6.7% for 2025 and 6.2% for 2026.

Sectoral patterns underpinning the estimate point to a services-led expansion. Services are projected to accelerate to roughly 9.1% in FY26, up from 7.2% the prior year, with financial services, real estate and public administration estimated to grow near 9.9%. Hotels, transport and communication are estimated at about 7.5%. Manufacturing and construction are both estimated to grow 7.0% at constant prices; manufacturing accelerates from 4.5% a year earlier while construction slows from 9.4% the prior year.

Macro indicators show a mixed backdrop. Unemployment in November 2025 stood at 4.7%, the lowest since April, and subdued consumer price inflation was reported at 0.71% in November 2025. Analysts warn that such low inflation, while supportive of purchasing power and accommodative monetary policy, can keep nominal GDP growth weak. Professional services firms note that muted nominal expansion may complicate fiscal arithmetic for Budget 2026 by constraining gross tax revenues and potentially forcing adjustments in revenue expenditure.

Near-term risks temper the upbeat headline. Credit ratings firm ICRA projects some moderation in momentum in the second half of the fiscal year, forecasting GDP and GVA growth of 6.9% and 6.8% respectively for H2, citing the possibility of a contraction in government capital expenditure, new U.S. tariffs on merchandise exports, and an unfavorable statistical base. External trade tensions and any unexpected shifts in oil prices remain key downside risks.

For markets and policymakers, the immediate implications are clear. Stronger-than-expected real growth will support demand, corporate earnings and credit off-take, and gives the Reserve Bank room to keep financial conditions accommodative if inflation remains benign. At the same time, low nominal growth raises the stakes for the government’s fiscal plan due in Budget 2026; authorities may need to balance revenue shortfalls against the political and economic benefits of continued capital spending. The first advance estimate sets a positive baseline, but revisions, second-half momentum, and policy choices will determine whether the strength is sustained into 2026-27.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?