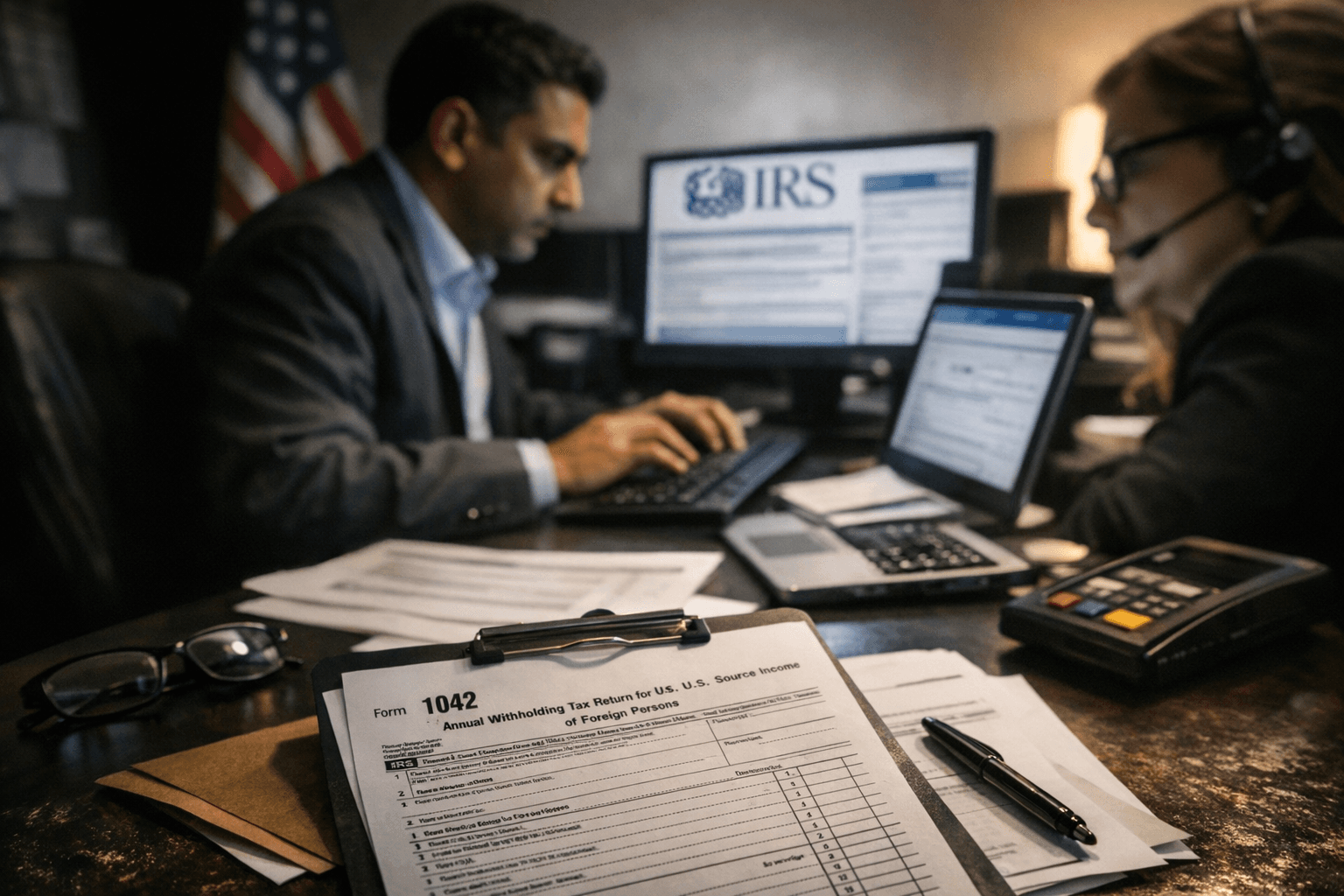

IRS Alert: Withholding Agents Must E-file Form 1042 for 2025 Using MeF

The IRS alert dated February 20, 2026 requires qualified intermediaries, withholding foreign partnerships, and withholding foreign trusts to e-file Form 1042 for tax year 2025 through the Modernized E‑File (MeF) platform; IRS Notice 2024‑26 relief has expired.

The U.S. tax authority (IRS) on February 20, 2026, issued an alert, reminding certain qualified intermediaries (QIs), withholding foreign partnerships (WPs), and withholding foreign trusts (WTs) of the requirement to electronically file Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons, for tax year 2025 through the Modernized E‑File (MeF) platform. The alert makes clear that the administrative relief previously provided under IRS Notice 2024‑26, which had temporarily exempted certain withholding agents from the Form 1042 electronic filing requirement, has expired.

KPMG’s TaxNewsFlash United States index lists an advisory titled “United States: Electronic filing requirement for Form 1042 for tax year 2025” on March 3, 2026 and references a March 2026 report prepared by KPMG US that expands on the alert. The KPMG excerpt includes the firm’s Circular 230 disclaimer and the 2026 copyright boilerplate identifying KPMG LLP as a Delaware limited liability partnership and part of the KPMG global organization.

The e‑file mandate follows a regulatory trend dating back to final regulations issued as T.D. 9972. KPMG’s February 21, 2023 TaxNewsFlash United States No. 2023‑062 summarized those final regulations and stated, “The final regulations require filers to aggregate across return types to determine whether a filer meets the 10‑return threshold and is thus, required to file electronically.” The 2023 advisory also tied applicability dates for business forms such as Form 1120 and Form 1065 to calendar years beginning after December 31, 2023, signaling a phased expansion of mandatory electronic filing across multiple return types.

Practically, the February 20, 2026 alert names the Modernized E‑File platform as the required route for Form 1042 submissions for tax year 2025. KPMG’s materials reconcile variants in terminology across its advisories - one excerpt used the phrase “qualifying intermediaries,” while another used “qualified intermediaries (QIs)” - but both point to the same categories of withholding agents now subject to the MeF requirement. KPMG’s March 2026 report is cited by the firm for further guidance, though the provided excerpt omits the report’s full text and link.

KPMG’s archive also shows the firm’s longer history of urging electronic filing in employer-tax contexts. In a Taxnotes summary of a February 10, 2000 submission by Harry L. Gutman and C. Elizabeth Wagner of KPMG, the authors wrote that “Many employers that might take advantage of the credits aren't doing so, Gutman and Wagner say, because the current certification requirements are so onerous,” and that “Electronic filing of Forms 8850 would significantly ease the burden on employers.”

With IRS Notice 2024‑26 expired and the February 20, 2026 alert in place, QIs, WPs, and WTs responsible for Form 1042 for tax year 2025 must transmit those returns electronically via MeF. Firms handling U.S. source income of foreign persons should review KPMG’s March 2026 analysis and the IRS alert to confirm MeF enrollment and any remaining technical or timing details.

Know something we missed? Have a correction or additional information?

Submit a Tip