Majority of Japanese households expect prices to keep rising

A Bank of Japan survey shows most households anticipate continued inflation, a sign expectations may be sticking and complicating policy choices.

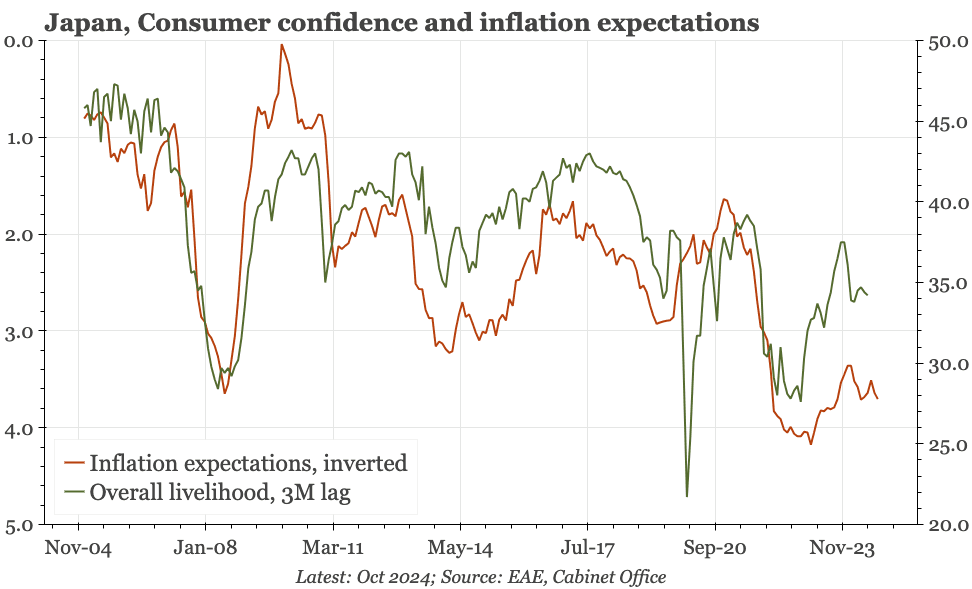

A Bank of Japan household survey released Monday found a large majority of Japanese households expect prices to continue rising over the coming years, reinforcing other evidence that inflation expectations are shifting upward and may be becoming entrenched. The BOJ’s published text noted only that "the share of households expecting higher prices one year ahead remained" and did not include the survey's final one-year-ahead percentage in the material supplied.

The survey outcome sits atop a growing body of research and statistical evidence that links recent price shocks to changes in public expectations. Japan’s all-items consumer price index rose 3.0 percent year-on-year in October 2025, according to the Japanese Center for Economic Research, a pace below the 4.3 percent peak in January 2023 but still above the BOJ’s 2 percent target. JCER also reports that among worker households with two or more persons, nominal consumption rose faster than the CPI in 2024–2025, implying real consumption gains for that group even as prices climbed.

The BOJ itself attributes part of the shift in expectations to households’ past experiences with inflation. In its analysis the central bank emphasizes that lower experienced inflation over decades, especially among younger generations who lived mostly through deflationary conditions, historically kept expectations subdued. The BOJ cites theoretical frameworks including the sticky-information hypothesis and adaptive learning models to explain how information and experience filter into forecasts of future prices, and notes that the link between experienced inflation and expectations can weaken in periods of high volatility.

Academic research at the household level sharpens the policy implications. A June 2024 paper by Hibiki Ichiue, Maiko Koga, Tatsushi Okuda and Tatsuya Ozaki finds that lower-income households pay less attention to the central bank and form inflation expectations more from what they observe in prices than from policy communication. The authors build a rational inattention model showing that households facing idiosyncratic income risk and borrowing constraints gain less from acquiring information about future inflation because they are less able to adjust spending. That heterogeneity matters for monetary policy: if lower-income households do not internalize central-bank signals, the transmission of policy through expectations and spending may be uneven.

Several macro shocks since 2022 help explain why norms about prices appear to be shifting. A spike in resource prices linked to the war in Ukraine and a rapid depreciation of the yen in 2022 - from roughly 110 to nearly 150 at one point, a drop of almost 40 yen - pushed import costs and consumer prices higher and may have altered public perceptions of what is normal. Analysts assembled in commentary and interviews expect inflation to ease toward about 2 percent after the end of 2025, aided in part by the scheduled abolition of a gasoline tax surcharge, but they flag upside risks. A stronger-than-expected US economy that prevents Federal Reserve rate cuts could keep the dollar strong and the yen weak, sustaining imported inflation, and movements in crude oil prices remain a key uncertainty.

For the BOJ, the survey offers confirmation that public expectations have shifted materially. That shift, combined with income-related differences in attention and spending responses, presents a complex backdrop for policy: entrenched expectations could make it easier to achieve price stability at higher levels, but uneven attention and exposure across households complicate assessments of how monetary moves will affect real activity and distributional outcomes.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?