Many Americans lack a plan for retirement income, surveys find

Only 44% of Americans say they have a retirement income plan, even as 63% fear outliving their money. Many retirees are already drawing down savings without a strategy.

Americans have spent decades being told to save for retirement, but a growing body of survey data shows a far less discussed problem: how to turn those savings into income that lasts. Fewer than half of Americans, 44%, say they currently have a plan for how they will take income in retirement, and 45% worry about how to best take distributions from retirement savings, according to Allianz Life.

That gap matters because the stakes are no longer just about accumulation. In Allianz Life’s survey of 1,000 U.S. adults age 25 and older, fielded online in February and March 2024 among households meeting income or asset thresholds, 63% said they worry more about running out of money than about death. Another 35% said putting part of their savings into a product that provides lifetime income payments was a top solution, a sign that many households are looking for guardrails as they shift from saving to spending.

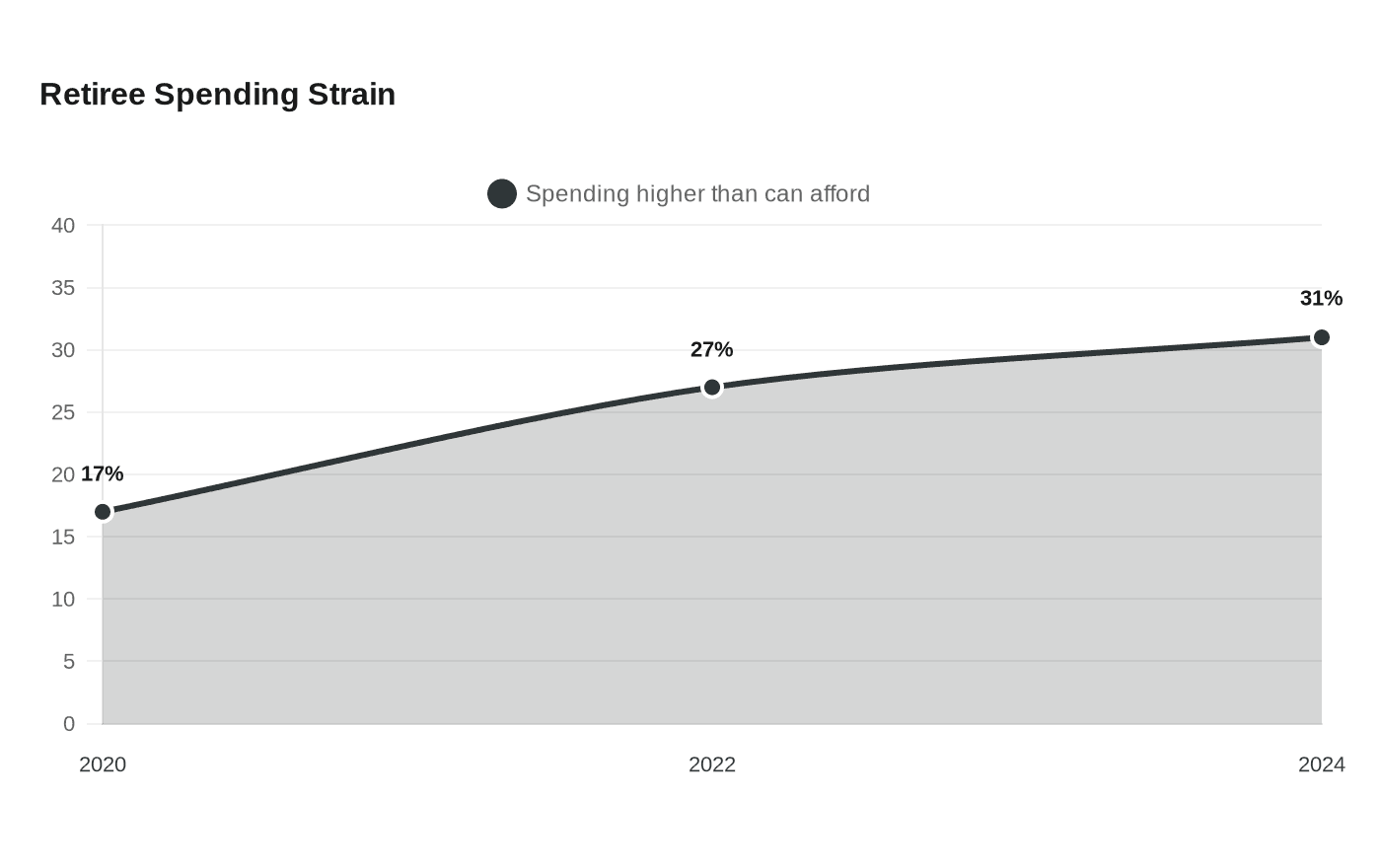

The anxiety is showing up in retirement behavior. The Employee Benefit Research Institute found that 31% of retirees said their spending was much higher or a little higher than they can afford in 2024, up from 27% in 2022 and 17% in 2020. EBRI also found that 59% of retirees had only three months of emergency savings, down from 69% in 2022, and 36% said they had experienced unexpected spending needs since retirement. Among people who left work earlier than planned, 38% cited health problems or disability, while 23% pointed to company changes such as downsizing, closure or reorganization.

Many retirees are still improvising. IRALOGIX reported that 49% of retirees forego a formal withdrawal strategy and take money as needed, while only 22% use a systematic fixed-percentage drawdown approach. The company said the biggest challenge was understanding the range of withdrawal options available. That uncertainty leaves households exposed to overspending in early retirement, underspending that limits quality of life, taxes that can erode withdrawals and market shocks that can hit hardest when balances are falling.

The pressure extends well before retirement. AARP said in April 2024 that 20% of adults age 50 and older had no retirement savings, 61% worried they would not have enough money in retirement and nearly 57 million people lacked access to a workplace retirement plan. AARP also said Americans are 15 times more likely to save when they have access to a workplace plan. Goldman Sachs Asset Management said housing, healthcare, debt service and caregiving are swallowing a larger share of income, creating what it called a “Financial Vortex.” The retirement conversation is moving beyond how much people save and toward how they will spend it, protect it and make it last.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip