Mortgage Rates Drop Sharply, Hitting 6.22% for 30-Year Fixed Loans

The 30-year fixed mortgage rate fell to 6.22%, shedding a quarter point in just five days and reversing a month of rate increases driven by tariff fears and the Iran conflict.

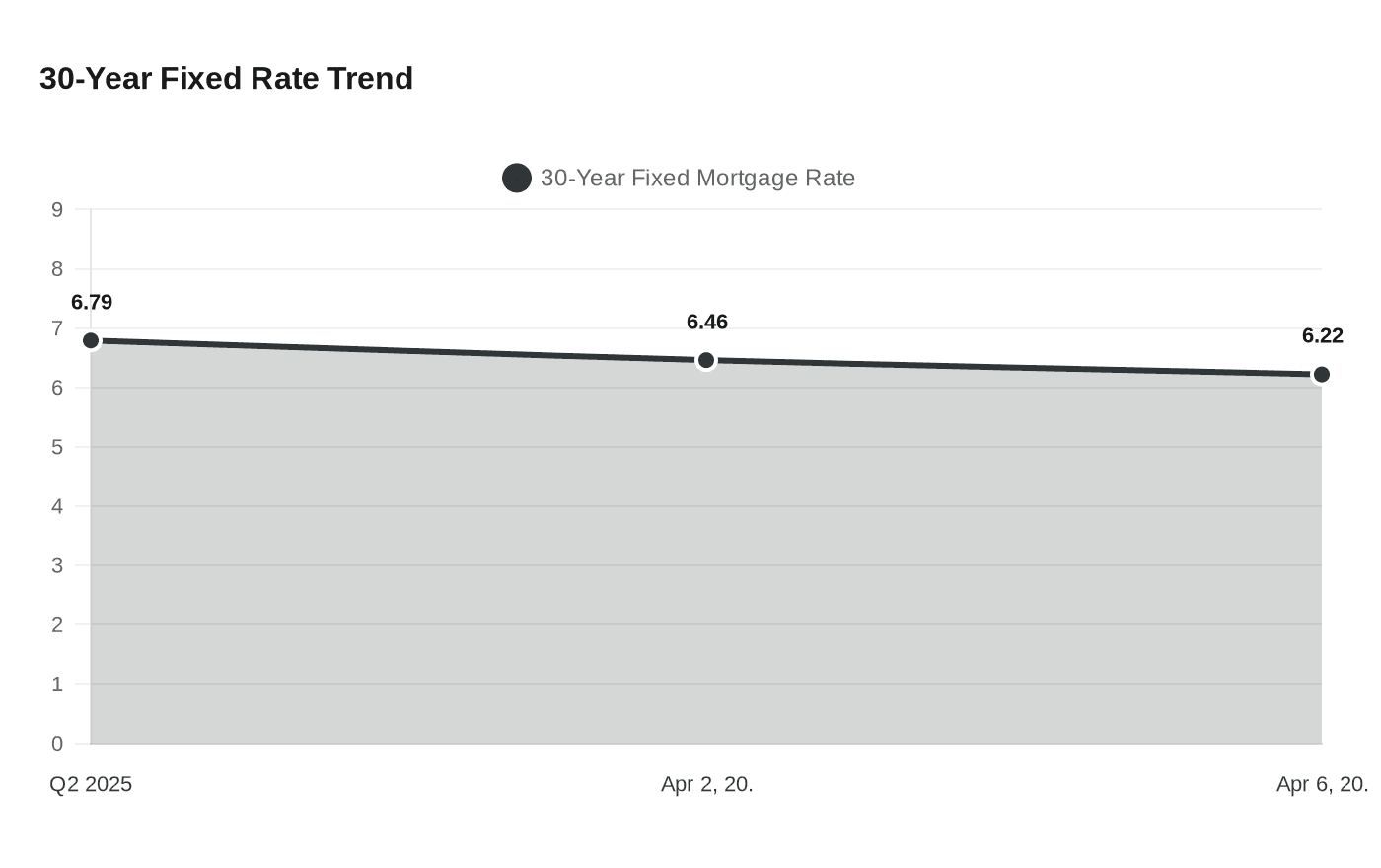

The 30-year fixed mortgage rate shed a quarter of a percentage point in five days, landing at 6.22% on April 6 per Zillow's lender marketplace. The reversal unwound a month of steady increases that had carried rates roughly half a percentage point higher through March, driven by inflation fears tied to the U.S.-Iran conflict and escalating trade policy uncertainty.

The previous Freddie Mac Primary Mortgage Market Survey, released April 2, had placed the 30-year fixed rate at 6.46%, up from 6.38% the week before. The 15-year fixed rate fell to 5.72% on Zillow, down 18 basis points over the same five-day span. Bankrate, drawing from a broader lender pool, placed the 30-year fixed rate at 6.50% with the 30-year refinance rate at 6.68%. Zillow noted rates "inched lower this week as an upbeat jobs report bumped the bond market slightly higher," easing the flight-to-safety pressure that had rattled Treasury yields throughout March.

The rate environment remains shaped by forces that could quickly reverse those gains. The Federal Reserve held its benchmark at 3.50%–3.75% at its March 18 meeting, the second pause of 2026, after three cuts in late 2025. Fed Chair Jerome Powell indicated officials expect only one additional quarter-point cut this year, citing tariff-driven uncertainty and the ongoing Iran conflict. He acknowledged the oil price surge might prove a "one-time" effect but added: "I wouldn't say there is a conviction that this is going through quickly."

Tariff policy is creating contradictory pressures in the bond market. Inflation fears push 10-year Treasury yields, and therefore mortgage rates, higher; recession fears trigger the opposite reaction, sending investors into Treasuries and lowering yields. Morningstar Senior U.S. Economist Preston Caldwell projected tariffs could add 1.3 percentage points to inflation in 2026 alone. Meanwhile, Danish pension fund AkademikerPension announced plans to sell its U.S. Treasury holdings by end of April. Raymond Robertson, professor of trade, economics and public policy at Texas A&M University, warned that a broader foreign bondholder selloff could "bring about higher monthly payments for home loans."

The cost difference between recent rate levels is tangible. A $300,000 30-year loan at 6.22% carried a principal-and-interest payment of approximately $1,835 per month; at 6.46%, the same loan cost $1,892. On a $400,000 loan at 6.46%, monthly payments reached roughly $2,507.

Zillow Senior Economist Kara Ng noted that the rate increases seen in recent weeks "have already wiped out about 30% of the affordability gains achieved earlier this year," when the 30-year fixed briefly fell below 6% in late February, its lowest reading in more than three and a half years. Housing market data reflected that strain: the National Association of Realtors reported existing home sales fell 5.2% in February, while Redfin found 46% more sellers than buyers nationally, the widest gap since 2013, with Miami, Nashville, and Austin among the most imbalanced markets.

Forecasters diverged on the year-end trajectory. The Mortgage Bankers Association expected the 30-year rate to hold near 6.30% through most of 2026, while Fannie Mae projected a dip below 6% by year-end and an average of roughly 5.6%–5.7% in 2027. TD Cowen offered the bullish case: a 10-year Treasury yield retreat to 3.5% by December could pull 30-year fixed mortgages toward 5.25%.

Stephen Kates, CFP and financial analyst at Bankrate, captured the tension facing buyers and policymakers alike, calling the current environment one where "there is no shortage of confusing narratives" placing the Fed "in a difficult position." With the 30-year rate averaging 6.64% one year ago and 6.79% in the second quarter of 2025, today's reading sits below both benchmarks. Whether it holds there depends heavily on whether trade and geopolitical tensions find any resolution before summer.

Know something we missed? Have a correction or additional information?

Submit a Tip