Producers at PGA Awards warn consolidation could cost jobs, test 30-film pledge

Producers at the PGA Awards voiced fear and skepticism over Paramount-Skydance’s $110 billion Warner Bros. acquisition, citing job risk and doubts about delivering 30 theatrical films a year.

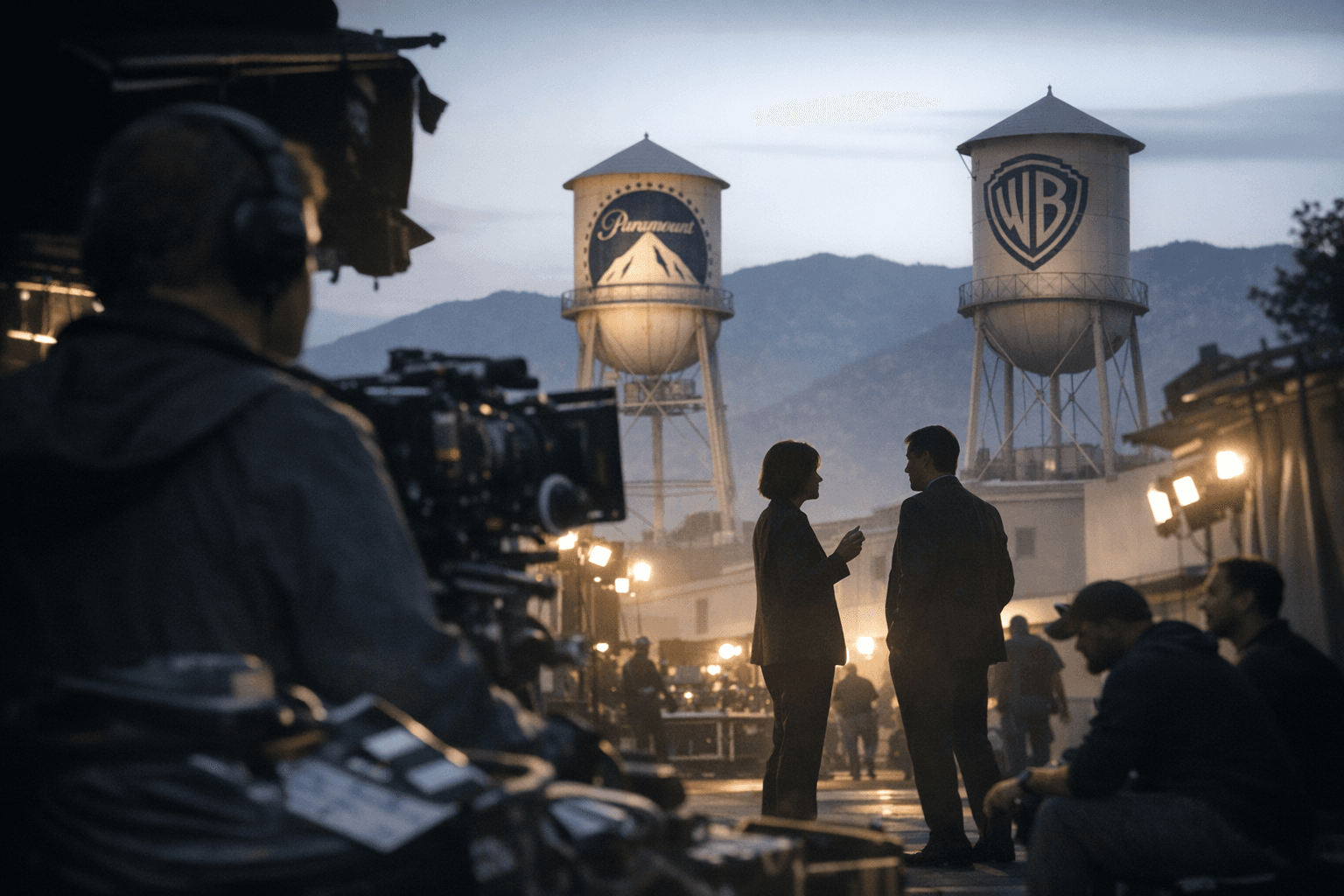

Producers on the red carpet at the Producers Guild of America Awards in Los Angeles voiced a mix of fear, skepticism and guarded hope after Paramount Skydance agreed to acquire Warner Bros. Discovery in a $110 billion deal reached on a Friday following Netflix’s decision to back out of a bid. The comments put industry labor and theatrical strategy under immediate scrutiny as executives promise a larger release slate.

Several top producers said the consolidation removes a major standalone buyer from the marketplace and risks job losses across development, production and marketing. “It’s sad that a lot of people will lose their jobs, but David Ellison loves movies and will make a lot of movies, which is a good thing,” Jerry Bruckheimer wrote in a public post that producers referenced on the carpet, coupling concern about employment with cautious optimism about output under the new controlling owner.

The most specific anchor in the conversation is a pledge tied to David Ellison’s leadership: a plan to release 30 theatrical films a year from the combined operation. Some producers embraced the numeric target as a sign the studio will continue prioritizing cinemas. Others questioned whether a single leader can realistically oversee that volume while preserving quality and managerial bandwidth.

“If [Ellison] keeps Warners separate from Paramount, it’s conceivably possible,” said Roven, whose credits include about a dozen Batman and Superman movies at Warner Bros. “I just think it’s going to be challenging depending on how dominate of a presence a guy at the top – and David is on the top – is going to be because he’s not going to have time to actually get granular on 30 movies. I don't think. Maybe his is that brilliant. I don't know.”

Jason Blum, this year’s Milestone Award recipient at the PGAs, pushed back on alarms about consolidation, calling the concerns “an overblown thing about the consolidation.” He noted the industry has absorbed major shifts before, pointing to the era a decade ago when Netflix, Amazon and Apple were ramping up film and television activity and reshaping business models.

Mike Farah, a producer and PGA Awards event co-chair, declined to take a firm position while the picture is still forming, saying he wants “to give people time to figure it out.” Mara Brock Akil was among other producers who weighed in without offering direct quotes on the red carpet.

The transaction’s business mechanics and scale, $110 billion and the withdrawal of a previous bidder, sharpen market stakes. Removing an independent buyer compresses options for talent and distributors, potentially increasing negotiating leverage for a combined studio but also concentrating risk for exhibitors and independent producers who rely on multiple buyers to sell projects. The threat of layoffs cited by producers would have ripple effects across craft guilds, regional production hubs and studio support services.

For theaters and financiers, the prize of a larger theatrical slate could be offset by greater release clustering and ownership-driven distribution choices. The industry will be watching whether the new owner keeps Warner and Paramount operations sufficiently separate to sustain creative diversity and whether the 30-films-a-year target translates into more mid-budget theatrical projects or simply a larger slate of franchise and tentpole releases.

Producers’ red carpet reactions underscore a moment of transition: a major consolidation has been sealed, quantitative promises are on the table, and the industry must now weigh how those choices will affect jobs, theaters and the economics of making movies.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?