Protected Income Does Not Always Shield Your Bank Account From Freezes

Certain income may be off-limits to creditors, yet your bank account can still be frozen if a debt collector wins a court judgment against you.

Certain types of income may be off-limits to creditors, but that doesn't mean your bank account is safe. It's a distinction that catches countless consumers off guard: just because federal law designates your Social Security checks, veterans benefits, or disability payments as protected doesn't mean the account holding those funds is automatically immune to a freeze. Understanding where the protection ends and the vulnerability begins can be the difference between a manageable legal dispute and a financial crisis.

How a bank levy actually works

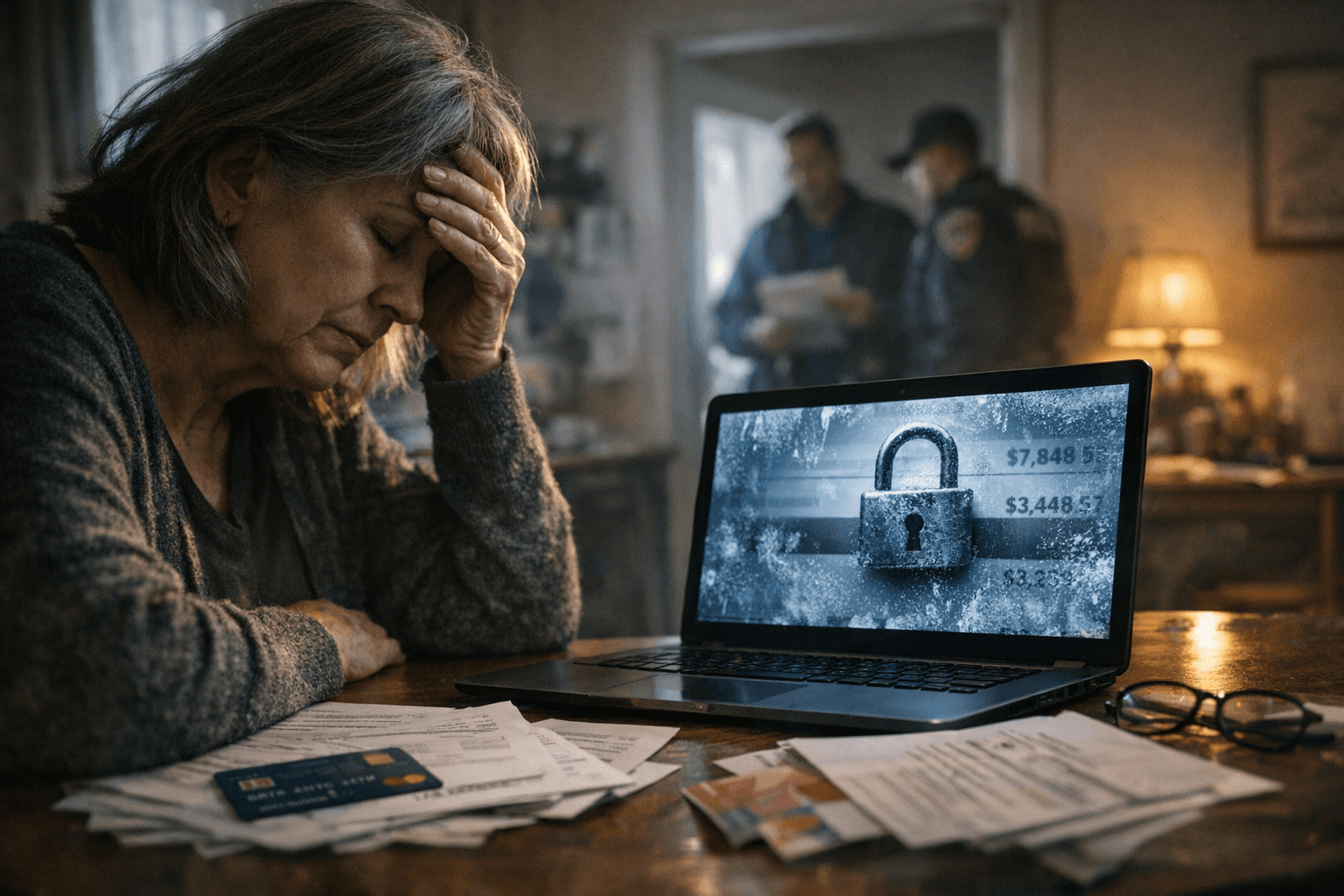

The legal mechanism that makes this possible is a bank levy. If a creditor wins a lawsuit for unpaid debt, they may be able to place a levy on your bank account, which allows them to freeze or seize funds to cover what you owe. The process moves quickly once a judgment is in hand. Once the bank receives the legal order, it may freeze funds in the account to prevent withdrawals while the debt collection process moves forward.

"Few financial situations feel more urgent than discovering you can't access the funds in your own bank account," CBS News noted in its coverage of bank account freezes. For many borrowers, the first instinct is to assume the bank made a mistake or that the account was flagged for fraud. But in some cases, the freeze may be the result of a debt collector enforcing a court judgment against you. If a creditor has placed a levy on your bank account, it usually means they obtained a court judgment related to your unpaid debt.

Where protected income protection actually stops

Federal law does shield certain income streams from garnishment. Benefits received via direct deposit from programs such as Social Security, Supplemental Security Income (SSI), veterans' benefits, and federal civil service retirement programs carry specific legal protections. According to the Consumer Financial Protection Bureau (CFPB), when a bank receives a court order to garnish money in an account, it must review the account's deposit history to determine whether federal benefits were directly deposited within the prior two months. If so, the bank is required to automatically protect two months' worth of those directly deposited benefits before freezing any funds.

The critical word here is "directly." The CFPB is explicit: "the key to making sure your federal benefits are legally protected from being frozen or garnished is to use direct deposit." If you receive a federal benefit by paper check and then deposit it yourself, the bank does not have the same obligation to shield those funds. In that scenario, your entire account balance could be frozen, and you would need to go to court to demonstrate that the money comes from a protected source. SSI carries even stricter protections and remains shielded from garnishment even to pay certain government debts or court-ordered support obligations, according to CFPB guidance.

State law adds another layer of complexity. Many states provide additional exemptions that can protect wages or minimum account balances from garnishment, but those rules vary significantly by jurisdiction. A bank levy typically freezes an account for a period set by state law, often 10 to 21 days, during which you can file a claim of exemption. After that window closes, frozen funds can be released to the creditor if no successful challenge is filed.

What to do the moment your account is frozen

Knowing what to do quickly can make a major difference in how the issue unfolds. The first step, as CBS News advises, is to confirm the reason for the freeze. Contact your bank directly and ask whether a levy or garnishment order has been received. Request a copy of any court order or legal notice associated with the action. This tells you whether you are dealing with a creditor levy, a government debt collection action, or something else entirely.

Once you have confirmed the source, assess whether any funds in the account are potentially exempt. If federally protected benefits have been directly deposited, notify the bank, the court, and the party seeking garnishment immediately. The CFPB recommends documenting the source of your funds clearly for any court hearing, because it is essential that a judge understands your income's origin before deciding whether money should be turned over to the debt collector.

If state law provides additional exemptions, you may be able to file a formal claim of exemption during the freeze window to have protected funds released. Consulting a consumer law attorney as soon as possible is advisable, particularly if the freeze creates immediate hardship covering essential expenses.

Pre-judgment settlement versus post-judgment emergency relief

The marketplace for debt relief services draws a sharp distinction between pre-judgment options and post-judgment emergencies, and choosing the wrong type of firm at the wrong time can cost you.

National Debt Relief markets itself as the largest debt settlement company in the country, claiming over $1 billion in settled debt, an A+ BBB rating, and more than 550,000 clients. The firm says it is strongest on general unsecured debts including credit cards, personal loans, medical bills, and lines of credit above $7,500. However, National Debt Relief explicitly does not handle bank account freezes, restraining notices, or judgment defense. The firm does not file court motions or challenge levies. If your account is already frozen and you need emergency legal action, it is not the right fit. The firm's own positioning makes this clear: it is most useful for borrowers who want to settle unsecured debt before it escalates to a judgment and a freeze.

For businesses or individuals already facing a frozen account and needing emergency legal intervention, attorney-led firms occupy a different position. Delancey Street, which focuses exclusively on business and merchant cash advance (MCA) debt, describes itself as attorney-led, with over $100 million in total settled debt. The firm advertises a typical resolution timeline of 2 to 8 weeks for a single MCA, and its stated focus is on business owners with a frozen bank account who need emergency legal action and a negotiated settlement to prevent future freezes. These are company-stated claims and should be verified independently, but the distinction in service scope is meaningful: resolving a pre-existing freeze requires legal representation capable of challenging or negotiating around a court judgment, which standard debt-settlement firms are not designed to provide.

The broader lesson

The gap between having protected income and having a protected bank account is real, consequential, and widely misunderstood. Federal law builds safeguards around certain income sources, but those safeguards are not self-executing. They depend on how you receive your benefits, how quickly you respond to a freeze, whether you actively file for exemption, and whether the relevant court understands the nature of your funds. Treating a court judgment as a problem to address before it becomes a levy, rather than after, remains the most reliable way to keep your account accessible.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?