Rough-Polished Price Dislocation Hits Mid-Market, Pressuring Diamond Miners

Paul Zimnisky warns a decade‑high size-based rough-polished price dislocation is squeezing miners that rely on a healthy mid-market for production economics.

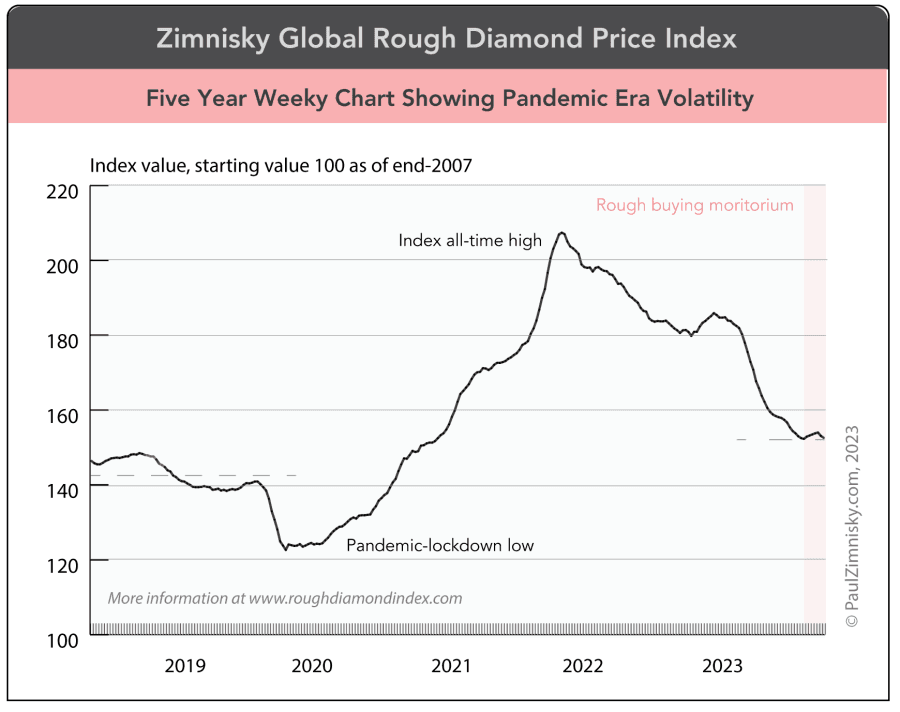

Paul Zimnisky wrote in his March 2026 commentary, published February 27, 2026, that “rough diamond prices by size category are displaying the clearest dislocation in at least a decade which is pressuring miners that depend on a healthy mid-market to support production economics.” The March issue lists detailed analyses — rough versus polished price analysis; rough price analysis by size; man-made versus natural price analysis; upstream excess inventory and mid-stream inventory analysis; and global supply/demand forecast — and notes company updates for De Beers, LVMH and Pandora.

Market moves this month underline Zimnisky’s point. Rapaport’s weekly bulletin dated March 5, 2026 opened with “US-Israel-Iran war shakes sentiment. Iranian attacks on Dubai disrupt global rough and polished trade.” Rapaport reported Dubai and Israeli diamond exchanges were “essentially closed; imports and exports frozen,” that rough tenders had moved to Antwerp, and that Hong Kong shows reflected a market split with “steady trading in 3 ct.+ goods despite low traffic. Buyers few but serious.” Rapaport’s price notes capture the bifurcation by size: “Feb. 1 ct. RAPI -1.3%;” while RAPI was up for 0.30 ct., 0.50 ct. and 3 ct. diamonds, and “prices of 5 ct.+ rough increase at tenders.”

Retail and polishing-house behavior is tilting the other way for large stones. Archit Mohanty at CaratX wrote on February 27, 2026 that “2 Carat+ Rounds and Ovals: There is a notable surge in demand for larger center stones,” and that retailers are showing “bullish sentiment at the retail level” by buying inventory directly rather than relying on memo. CaratX explicitly links that buying pattern to rising rough prices “specifically for material that will yield 2 carat+ polished goods,” even as mid-market classes show weakness.

Beyond price and demand dynamics, governance and structural risks are on the table. Sergey Goryainov in Rough-polished on December 17, 2025 warned that “should De Beers become a state-owned company, its further development will be entirely determined by the easily predictable motivation of the managerial elites of African states,” adding that “the change of ownership of De Beers may become the fourth fundamental factor accelerating the decline of the diamond market in 2026.” Zimnisky’s inclusion of De Beers in company updates in the March issue makes that hypothetical risk a live consideration for miners and buyers.

The backdrop remains large but uneven. IntelMarketResearch published March 3, 2026 values the global diamond (rough, polished & jewelry) market at USD 92.4 billion in 2025 and projects growth from USD 97.8 billion in 2026 to USD 142.6 billion by 2034, at a 5.7% CAGR. Even with long-term expansion forecast, the present size-by-size dislocation and operational shocks — exchange closures in Dubai and Israel, tender relocations to Antwerp, Feb. 1 ct. RAPI down 1.3% — place immediate pressure on miners whose unit costs and tender economics depend on steady mid-market demand.

For companies and producers that lean on mid-market sales to finance open-pit and underground plans, this is a planning inflection. Zimnisky’s March commentary packages the data and company updates that will matter to buyers and producers; past issues of State of the Diamond Market are available for purchase for US$150 each, and can be ordered by emailing or calling +1-917-806-4555.

Know something we missed? Have a correction or additional information?

Submit a Tip