Scotland Charts Its Own Course on Income Tax and Social Security

Scotland's six-band income tax system and £28.20-a-week child payment put it on a starkly different fiscal path from England, with a May 2026 election forcing a reckoning on who pays and who gains.

The arithmetic is simple, and that is precisely why it has become so politically charged. A nurse earning £29,800, the Scottish median, pays around £5 less in income tax each year in Scotland than she would if she lived across the border in England. But a secondary-school head teacher on £80,000 pays roughly £2,332 more. Those two numbers, sitting alongside a near-universal child payment worth £28.20 per week that simply does not exist south of the border, define the most consequential fiscal experiment in the United Kingdom today. With a Scottish Parliament election set for 7 May 2026, voters are being asked, implicitly if not always explicitly, whether the model is worth keeping.

A Six-Band System Unlike Anywhere Else in Britain

Scotland's power to set its own income tax rates and bands for earned income dates to the Scotland Act 2016, but the divergence from the rest of the UK accelerated sharply over the following decade. Where England, Wales, and Northern Ireland operate a three-band structure, Scotland now runs six distinct bands, each calibrated to shift the burden upward through the earnings distribution.

For the 2025-26 tax year the structure looks like this:

- Starter rate: 19% on earnings from £12,571 to £15,397

- Basic rate: 20% on £15,398 to £27,491

- Intermediate rate: 21% on £27,492 to £43,662

- Higher rate: 42% on £43,663 to £75,000

- Advanced rate: 45% on £75,001 to £125,140

- Top rate: 48% on income above £125,140

The contrast with the rest of the UK is stark at the upper end. In England, the higher rate of 40% does not begin until earnings exceed £50,270. In Scotland, the 42% higher rate bites at £43,663, meaning any worker earning above that threshold enters a steeper tax band more than £6,600 sooner. The Scottish Government's own December 2024 Budget confirmed the Higher, Advanced, and Top rate thresholds will remain frozen until the end of this parliamentary term in 2026-27, deepening the divergence as wages rise with inflation.

What the Numbers Mean for Real Households

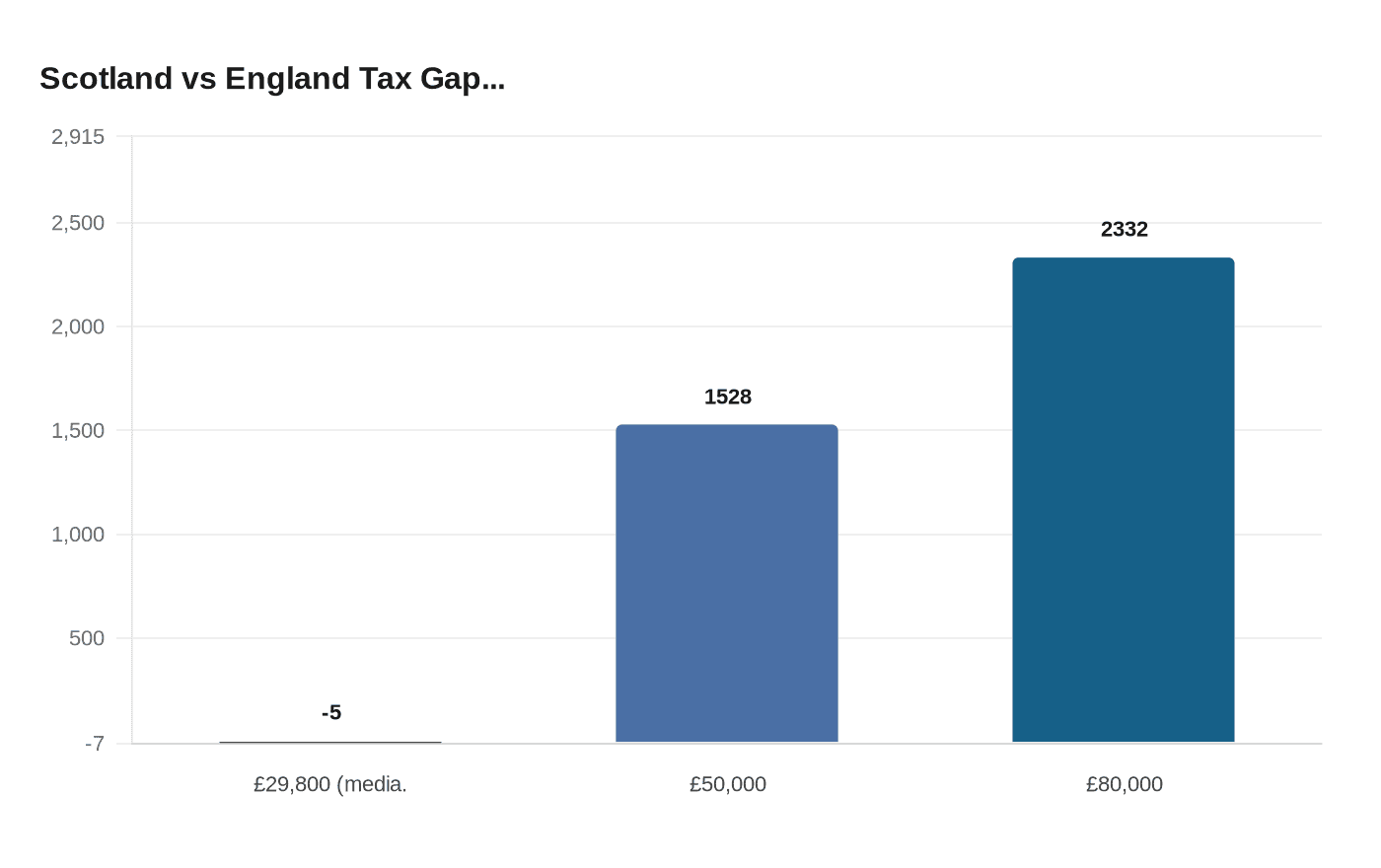

The Scottish Government and the independent Scottish Fiscal Commission have been explicit that the six-band model is built around a distributional bargain: the majority of workers pay a little less, while a minority of higher earners subsidise expanded public services and benefits. According to the Scottish Government's own 2025-26 factsheet, those earning less than around £33,500, expected to cover approximately 55% of all Scottish taxpayers, pay slightly less income tax than an equivalent worker in England. At the median income of £29,800, that saving amounts to £5 a year.

The maths shifts decisively above the intermediate band threshold. A worker on £50,000, calculated against the official 2025-26 bands, pays around £9,014 in Scottish income tax compared with roughly £7,486 under the UK-wide system, a premium of approximately £1,528. At £80,000, the gap widens to around £2,332 per year. These are not trivial sums; for a dual-income professional household where both partners earn above £43,662, the combined extra annual tax bill can exceed £4,600, a figure that features increasingly in conversations about whether Scotland risks losing mobile, high-earning workers to other parts of the UK.

For lower earners, the 2025-26 Budget brought genuine relief. The Starter rate band was widened by 22.6% and the Basic rate band by 6.6%, increasing the thresholds at which workers enter the Basic and Intermediate rates by 3.5%, well ahead of the September 2024 Consumer Price Index reading of 1.7%. The Scottish Government committed that no taxpayer would pay more in 2026-27 than they paid on the same income in 2025-26.

Scotland's Welfare Architecture: The Scottish Child Payment

While income tax gets the headlines, Scotland's most striking social policy departure is the Scottish Child Payment, a benefit with no direct equivalent anywhere else in the UK. Initially introduced at £10 per week for each child under the age of six, the payment has been raised to £28.20 per week and the eligibility age has been extended to children under 16. By September 2025, more than 322,000 children were benefiting from the payment, with over £1.3 billion issued to more than 241,000 parents and carers since the scheme launched.

The cumulative effect on a family's finances over a childhood is dramatic. According to Scottish Government figures, the Scottish Child Payment and other family payments delivered through Social Security Scotland could be worth around £25,000 by a child's 16th birthday, compared with less than £2,000 through equivalent UK-wide support in England and Wales. The Institute for Fiscal Studies projects the payment will reduce child poverty by around 50,000 children in 2026-27, and the Scottish Government estimates it will keep 40,000 children out of relative poverty in 2025-26. Scotland's child poverty rate is already measurably lower than the rest of the UK, though the IFS has noted that the Government's own ambitious 2030 statutory targets are set to be missed.

The payment sits within a broader welfare architecture that has grown significantly since the Scotland Act 2016 devolved around 15% of social security spending. Social Security Scotland's total budget for 2025-26 reached £7.0 billion, comprising £6.7 billion in benefit expenditure and £320.6 million in operating costs. The agency also administers Carer Support Payment, the Young Carer Grant for 16 to 18-year-olds, Best Start Grant, and, from March 2025, the newly introduced Scottish Adult Disability Living Allowance for older adults transferring from the UK's Department for Work and Pensions.

The Fiscal Pressure Underneath

The progressive tax model and expanded welfare commitments generate a structural tension that has become harder to paper over as the decade progresses. Scotland's devolved social security spending consistently runs ahead of the block grant adjustment it receives from the UK Treasury, the funding mechanism designed to keep Scotland's settlement neutral relative to England. Analysis by the Scottish Parliament Information Centre estimates that additional spending above that adjustment, which stood at around £0.5 billion in 2022-23, is forecast to reach £1.3 billion by 2027-28 before stabilising at around negative £1.5 billion as an annual pressure on the Scottish Budget.

The Institute for Fiscal Studies' assessment of Scotland's Tax Strategy, published alongside the 2025-26 Budget, acknowledged the strategy as a welcome framework while cautioning that some actual tax policy choices appeared disconnected from any coherent long-run plan. Fiscal drag, the process by which frozen thresholds pull more taxpayers into higher bands as wages rise, continues to work silently in the background. The frozen Higher, Advanced, and Top rate thresholds mean that as Scottish wages grow, a growing share of the workforce crosses into bands where they pay significantly more than comparable workers in England, tightening the squeeze on the professional and managerial class.

The Election as a Referendum on Fiscal Identity

The Scottish Parliament election on 7 May 2026 arrives at a moment when both the benefits and the costs of this experiment are measurable. SNP leader and First Minister John Swinney has committed to further uprating the Scottish Child Payment in line with inflation and has signalled plans to extend it further. Opposition parties have differing positions on whether the higher-rate tax premium is justified and sustainable, and whether the two-child limit, which Scotland has indicated it may seek to mitigate at substantial cost, represents a spending priority that can be funded without further widening the tax gap.

Scotland has effectively conducted a live experiment in whether a higher-tax, higher-benefit model can coexist within a broader UK fiscal framework that does not share those priorities. The results so far are genuinely mixed: child poverty metrics have improved, the majority of workers pay marginally less, and a distinct social contract is emerging. The unresolved question is whether the minority of higher earners who fund that contract will remain patient, and whether a block grant settlement calibrated to UK-wide spending choices can carry the weight of an increasingly divergent welfare state.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip