SEC ends defense of climate disclosure rules after court challenges

The SEC’s retreat leaves a stalled climate rule in limbo, raising the risk that investors still won’t get standardized data on emissions, weather damage and legal exposure.

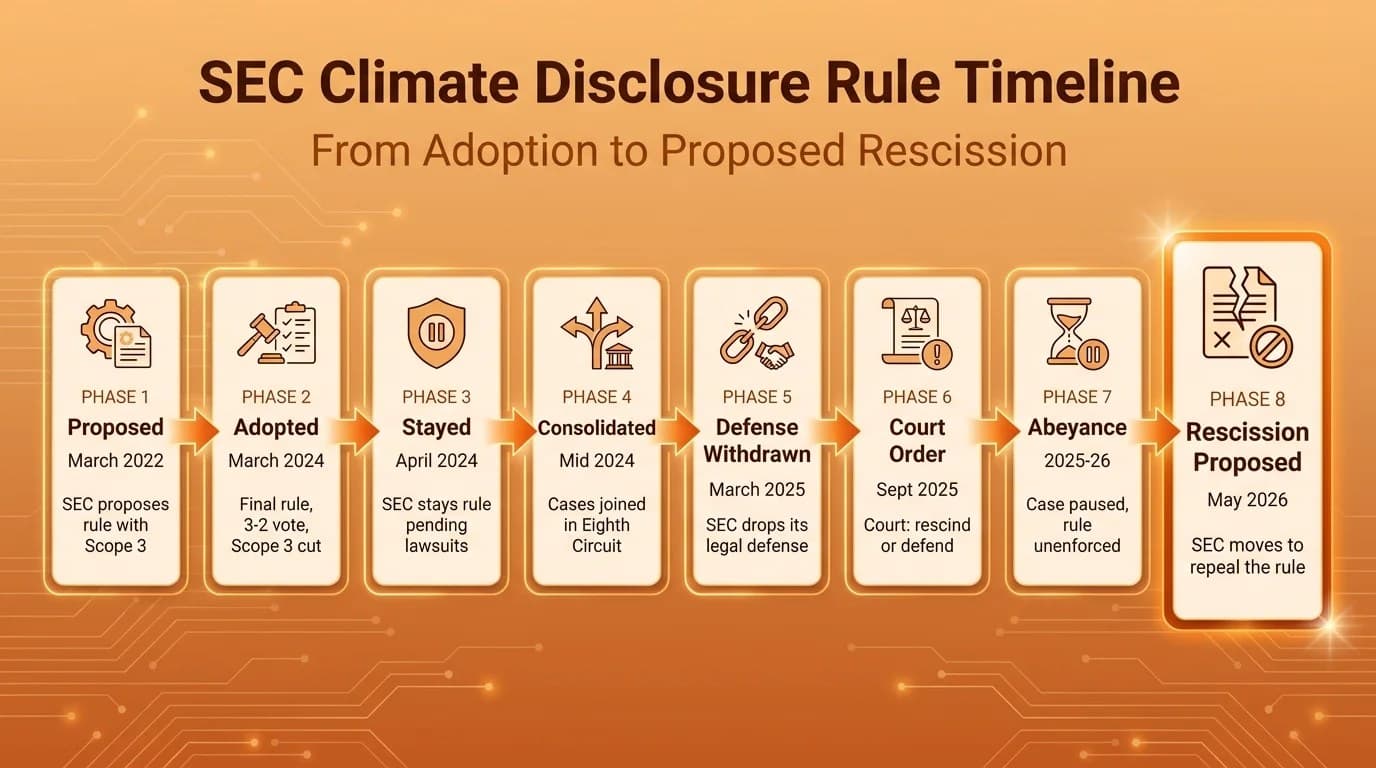

The Securities and Exchange Commission has walked away from defending the climate disclosure rules it adopted just 13 months earlier, leaving one of the agency’s most contested post-crisis rulemakings in legal limbo. On March 27, 2025, the commission voted to end its defense and directed staff to notify the U.S. Court of Appeals for the Eighth Circuit that SEC counsel were no longer authorized to advance the arguments in the agency’s brief.

That retreat matters far beyond the courtroom. The rule would have required publicly traded companies to tell investors whether they faced significant climate-related risks, and for some larger registrants to phase in disclosure of Scope 1 and Scope 2 greenhouse gas emissions. It also would have required attestation for some emissions data and financial-statement disclosures tied to severe weather events and other natural conditions. For shareholders, pension funds and other large asset owners, the point of the rule was simple: comparable information that could be used to price physical damage, legal exposure and transition risk across companies and sectors.

The rule itself had a short and turbulent life. The SEC proposed it on March 21, 2022, and adopted the final package on March 6, 2024. Petitions for review were filed within days, and the commission stayed effectiveness on March 15, 2024 while the challenges moved into the Eighth Circuit. The final rules were set to become effective on May 28, 2024, but the stay kept them from taking effect. By 2025, the litigation was still active, including cases consolidated under Iowa v. SEC and challenges brought by Liberty Energy Inc. and Nomad Proppant Services LLC.

At the center of the dispute was a basic question about what belongs in securities disclosure. Gary Gensler said the rules were meant to provide investors with “consistent, comparable, decision-useful information.” Supporters argued climate risks can materially affect a company’s operations, business strategy and financial condition, making them squarely an investor-information issue. Mark T. Uyeda, who voted to end the defense, called the rules “costly and unnecessarily intrusive,” while Hester M. Peirce argued existing disclosure requirements were enough and that Congress, not the SEC, should mandate climate reporting.

Caroline A. Crenshaw opposed the retreat, saying the commission was walking away from the rule. The outcome now leaves markets without a federal standard that could have forced companies to disclose more clearly how climate change might hit earnings, assets and long-term value.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?