Smaller UPI players seek curbs on PhonePe, Google Pay dominance

Smaller UPI rivals pressed India’s payments regulator to rein in PhonePe and Google Pay as the two apps controlled more than 80% of transaction volume.

India’s UPI market, the world’s largest open digital payments network, has become a duel over who controls the rails of everyday commerce. Smaller players are now pushing the National Payments Corporation of India to act, arguing that PhonePe and Google Pay have turned dominance into an almost locked-in advantage.

MobiKwik, Super.money, Amazon Pay and CRED were set to meet NPCI in Mumbai on Thursday, April 30, 2026, to press for curbs on the market leaders’ user-acquisition tactics, tighter monetization rules and changes designed to widen merchant access. The gathering came as Amazon and Meta stepped up their own fintech ambitions in India, adding commercial and political weight to a broader challenge against the UPI duopoly.

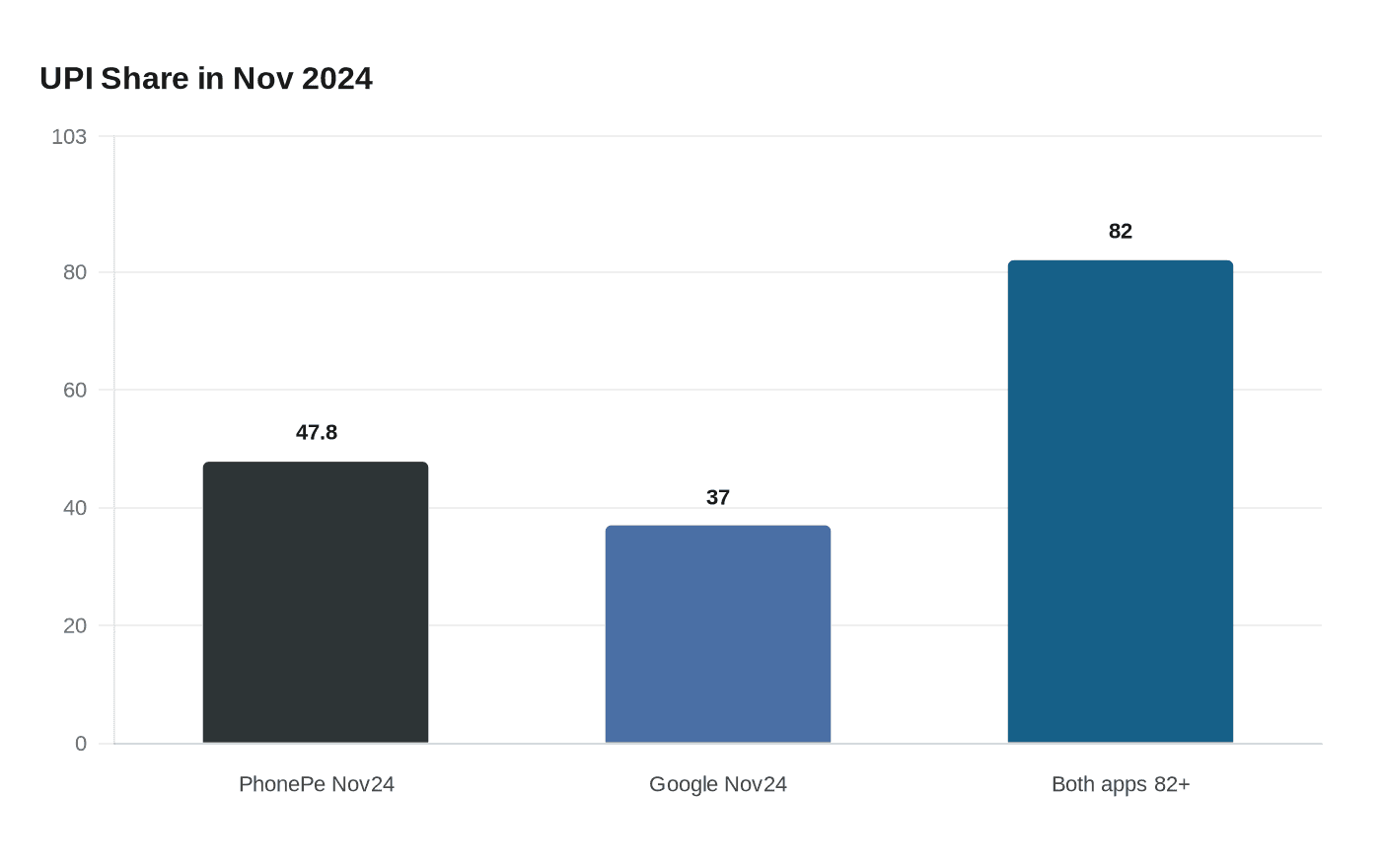

The scale of that concentration is stark. PhonePe and Google Pay together accounted for more than 82% of UPI transactions in June 2025. Regulatory data showed that in November 2024, PhonePe held 47.8% of UPI payments and Google Pay held 37%, giving the two apps a combined 13.1 billion transactions in that month alone. For smaller third-party app providers, those numbers are not just a market share problem but a warning that distribution, data and merchant relationships are becoming harder to dislodge.

NPCI has already acknowledged the risk. In November 2020, it announced a 30% cap on the UPI transaction share of any single third-party application provider, or TPAP, but the rule still has not been enforced. NPCI later pushed the compliance deadline out to December 31, 2026, leaving the largest apps free to keep expanding while rivals waited for the cap to bite. That delay has become central to the complaints now being carried into the regulator’s Mumbai headquarters.

The pressure intensified after the India Fintech Foundation told the finance ministry and the Reserve Bank of India in October 2025 that more than 80% of UPI transaction volume was controlled by just two TPAPs. The foundation warned that such concentration could create both competition and systemic-risk concerns, a rare sign that market structure itself, not just pricing or innovation, is now being treated as a policy problem.

Any move by NPCI would reach well beyond India’s fintech incumbents. For merchants, it could alter the bargaining power behind fees, incentives and checkout placement. For consumers, it could shape which apps dominate bill payments, transfers and rewards. For competition policy, it would turn India’s UPI framework into a test case for whether a fast-growing digital payment system can stay open without settling into a private duopoly.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)