Top auto lender says high car prices and long loans remain manageable

A top auto lender says borrowers are coping, even as median car payments hit $525 and 84-month loans reached a record share of new financing.

The strongest case that auto debt is still manageable comes from inside the lending business, but the household numbers tell a more complicated story. Capital One Auto President Sanjiv Yajnik said he is not overly concerned about rising vehicle prices, bigger loans and stretched terms, arguing that buyers are staying disciplined even as monthly costs climb.

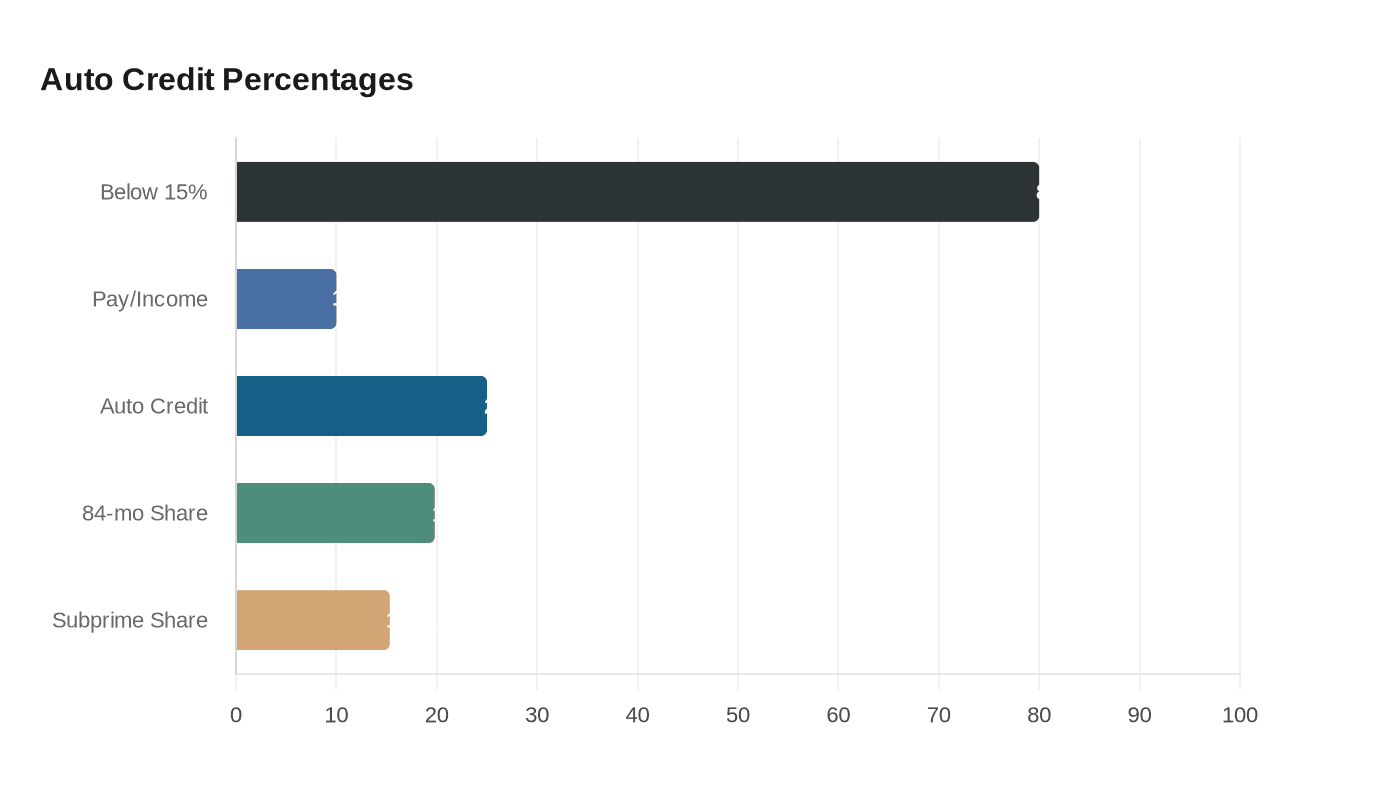

The problem is the cost of that discipline keeps rising. Median monthly car payments have jumped from $390 in 2019 to $525, and Capital One Auto says the payment-to-income ratio has stayed near 10% since then. The lender says 80% of financed car buyers are still below the widely used 15% payment-to-income threshold, suggesting many households are reaching for longer loans to keep the monthly bill within range.

That picture, however, sits alongside a market that is showing clear stress. The Federal Reserve said auto-loan delinquency rates rose substantially above pre-pandemic levels by the end of 2023, after falling to historical lows during the pandemic. Auto loans now account for about 25% of consumer credit, making weakness in the sector more consequential for household balance sheets and lenders alike.

New York Fed researchers have found the strain is broadening. Delinquencies have been rising across credit-score bands and area income levels, with the problems concentrated in loans from non-captive auto finance companies. That suggests the pressure is not limited to one corner of the market or to the lowest-credit borrowers.

At the same time, borrowers have been leaning harder on long terms. Edmunds said 84-month loans hit an all-time high in the first quarter of 2025, accounting for 19.8% of new-vehicle financing, up from 15.8% a year earlier and 13.4% in the first quarter of 2019. Longer terms can lower the monthly payment, but they also leave buyers exposed to negative equity for longer if the vehicle depreciates faster than the loan balance falls.

Other industry data point to persistent affordability pressure. Cox Automotive said new-vehicle affordability remained stable in August 2025 despite higher prices, though its index assumes a 72-month fixed-rate loan. Experian said the average new-vehicle loan amount rose to $43,582 in the fourth quarter of 2025, the average monthly payment climbed to $767, and subprime borrowers accounted for 15.31% of total vehicle financing, the highest share since 2021.

For lenders, those numbers can look manageable. For households, they reflect a market where cars are still essential, but increasingly financed on terms that push risk further down the road.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?