UK Consumer Borrowing Surges by Largest Monthly Rise Since 2023

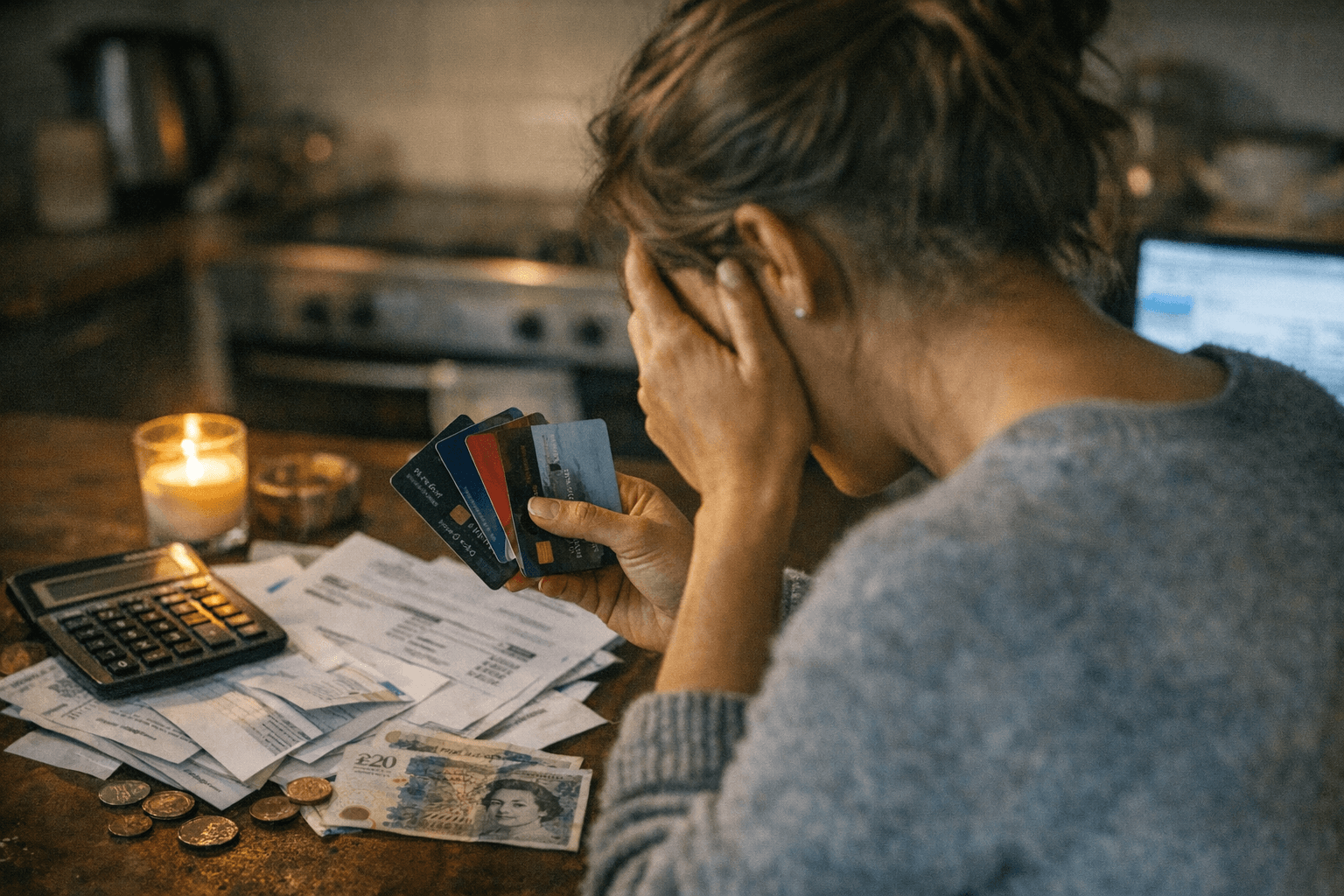

British household borrowing climbed sharply in November as consumer credit increased by a net £2.08 billion, pushing annual consumer credit growth to 8.1%. The acceleration, led in part by a jump in credit-card debt, tightens the squeeze on household finances and complicates the Bank of England’s policy calculus.

British consumers increased their use of unsecured credit in November, with Bank of England figures showing net consumer credit rose by £2.08 billion that month, the largest single-month gain since November 2023. The rise pushed the annual growth rate for consumer credit to 8.1 percent, a pace that exceeded economists’ forecasts and signals renewed appetite for borrowing despite stretched household budgets.

A breakdown of the figures showed that credit-card borrowing was a key contributor to the acceleration. Annual growth in credit-card debt rose from 10.9 percent in October to 12.1 percent in November, the strongest monthly rate since January 2024. The shift toward higher-cost, revolving forms of credit is notable because credit-card rates are typically variable and move quickly with market conditions, creating vulnerability for borrowers if interest rates remain elevated.

The November surge follows earlier upward pressure on borrowing. A social-media post on LinkedIn cited August figures showing net consumer borrowing of £1.692 billion and unsecured borrowing up 7.1 percent year-on-year, along with a mortgage-approval figure of roughly 64,680. The post also asserted that since September 2024 some lenders have allowed first-time buyers to borrow up to six times income with a 5 percent deposit and that one building society recorded 23,000 applicants for such a product. Those claims reflect potential shifts in lending supply and product design, but they require direct verification from lenders and regulators before being treated as confirmed trends.

The return to stronger consumer borrowing comes as households face a persistent cost-of-living squeeze. Elevated energy and food prices have eroded real incomes in recent years, and many households have drawn on savings buffers or increased borrowing to smooth spending. Rising unsecured borrowing rates are a warning sign: they tend to amplify downside risks to consumption when credit conditions tighten or when unemployment rises.

For the Bank of England, the data present a nuanced challenge. On one hand, stronger consumer demand financed by credit can sustain near-term economic activity and delay the onset of sharper slowdowns. On the other hand, growing reliance on higher-cost unsecured credit can increase financial fragility and sustain inflationary pressure if demand outpaces supply. The central bank must weigh these dynamics as it assesses the path of monetary policy, particularly given the lagged effects of rate changes on consumer borrowing costs and the mortgage market.

Market implications are immediate: higher-than-expected borrowing growth could influence sterling and government bond markets as investors reassess inflation persistence and the likely stance of policy. For households and policymakers alike, the trend underlines the importance of monitoring both the composition of credit growth and the terms on which it is being extended. Follow-up verification of lender-level product changes and mortgage-approval trends will be crucial to determine whether the November uptick represents a one-off adjustment or the start of a sustained shift in household financing behavior.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?