U.S. 30-year mortgage rate dips below 6% for first time in over three years

30-year fixed mortgage rates fell below 6% on Feb. 26, 2026, easing monthly costs for buyers and likely lifting refinance demand after years of high borrowing costs.

The average U.S. 30-year fixed mortgage rate fell below 6 percent on Feb. 26, 2026, marking the first time borrowers have seen that threshold breached in more than three years and offering near-term relief for homebuyers and homeowners weighing refinances. The move reduces monthly borrowing costs for new buyers and makes previously unaffordable price tiers more reachable, potentially nudging housing demand upward after a lengthy period of tight affordability.

The decline follows a pullback in longer-term Treasury yields and a recent cooling of inflation measures that has eased pressure on borrowing costs. Mortgage-backed securities, which set a floor for consumer borrowing, rallied as investors shifted away from safe-haven Treasuries and priced in lower rate expectations. The downshift in mortgage rates reverses a multiyear trend of rising home loan costs that pushed the 30-year rate above 7 percent at various points in 2022 and 2023, constraining demand and shrinking home-purchase activity.

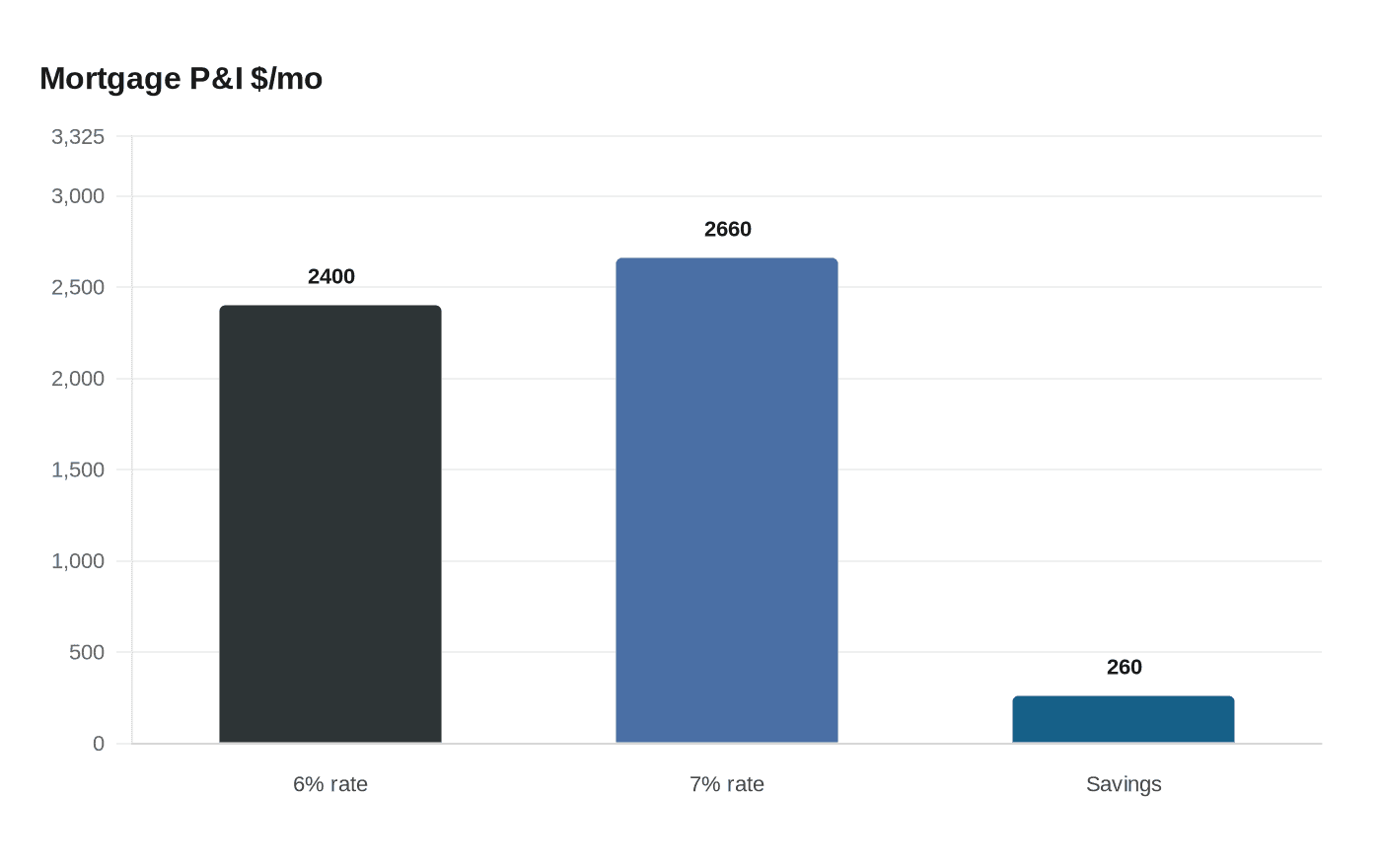

Lower mortgage rates have an immediate arithmetic effect on affordability. As a rule of thumb, a one percentage point drop in the 30-year rate expands a buyer's purchasing power by roughly 10 percent. That translates into meaningful monthly savings: for example, a 30-year loan of $400,000 at 6 percent carries a principal-and-interest payment of about $2,400 a month, compared with roughly $2,660 at 7 percent, a reduction of roughly $260 monthly for the same loan size. For prospective buyers who were on the margin, those savings can be decisive, increasing the pool of qualified borrowers and supporting a pickup in mortgage applications.

Lenders and mortgage servicers typically see activity respond within days to weeks when rates move decisively lower. Refinance applications, in particular, tend to rise when borrowers can lower monthly payments or shorten loan terms; purchase applications follow as affordability improves and buyers re-enter the market. Real estate brokers and some homebuilder indicators are likely to register stronger traffic and demand in coming months if rates remain below 6 percent.

But the longer-term impact depends on supply and local market dynamics. U.S. housing inventory has remained constrained in many metros after years of underbuilding, and price adjustments that would amplify demand are unlikely where inventory is tight. Economists caution that lower rates can boost demand without immediately increasing supply, which can sustain upward pressure on prices in seller-favored markets while easing affordability in areas with softer demand.

Policy context will be watched closely. The Federal Reserve's stance on short-term policy rates, and incoming inflation and employment data, will influence Treasury yields and, by extension, mortgage pricing. Market participants will be monitoring forthcoming economic prints and Fed communications to gauge whether this dip is the start of a sustained easing trend or a temporary reprieve.

For millions of households, the sub-6 percent threshold is tangible: lower monthly payments, expanded search bands, and renewed consideration of homeownership or refinancing. How much that translates into higher sales, stronger construction, or a rebalancing of regional markets will depend on the durability of rates below 6 percent and the pace at which builders and sellers respond.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?