U.S. Drillers Trim Rig Fleet, Oil Rigs Fall to Four Year Low

U.S. energy companies reduced the number of active oil and gas rigs this week to the lowest level since September, signaling a continued pullback in drilling activity that could shape supply months ahead. The shift matters for fuel markets, regional oilfield jobs and corporate investment plans as producers emphasize shareholder returns and debt reduction over rapid growth.

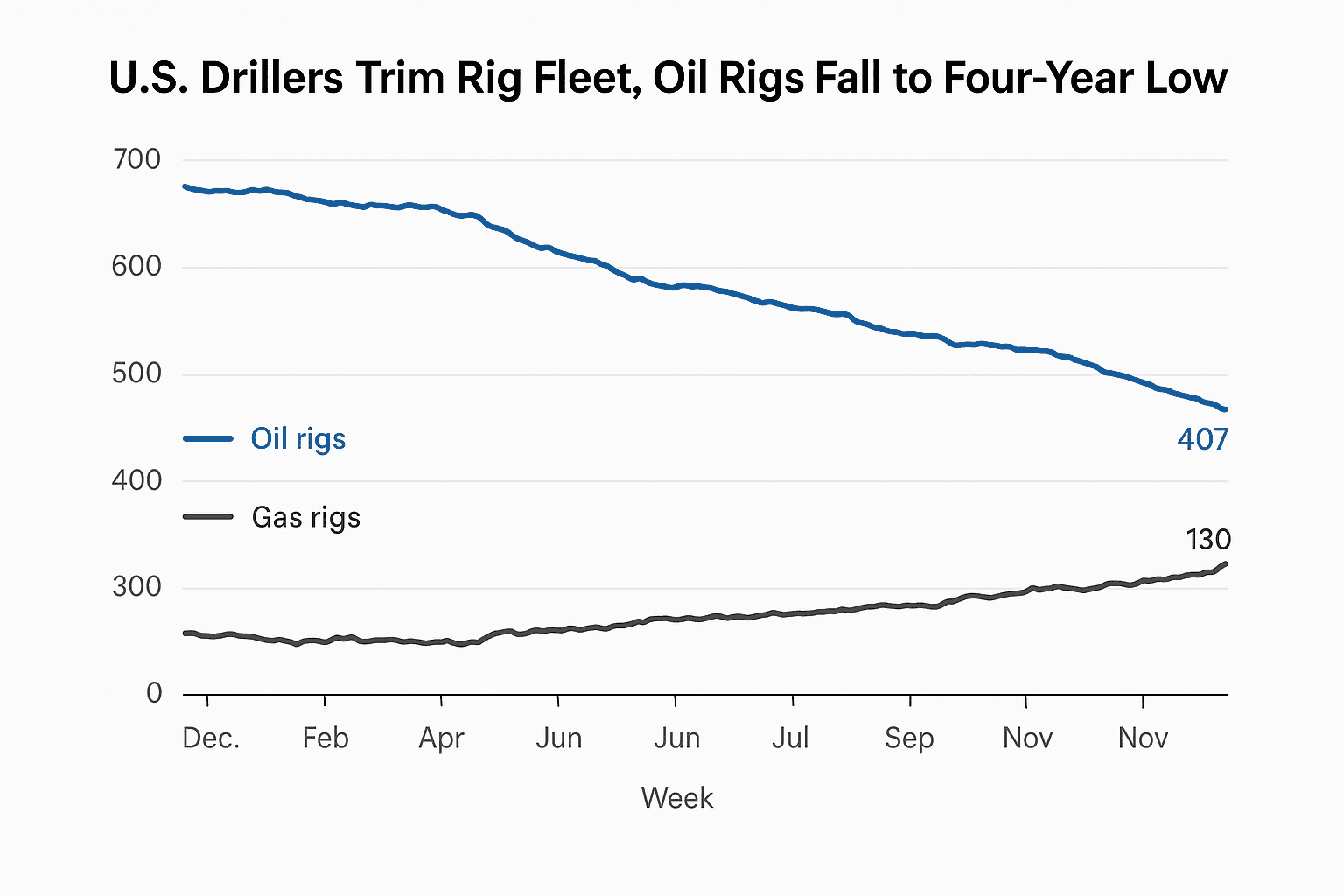

U.S. energy firms trimmed operating oil and gas rigs in the week ending November 26, lowering the total rig count to 544, Baker Hughes reported on November 27. The weekly tally is the lowest aggregate figure since September and comes as oil directed activity slipped while gas drilling edged higher.

Oil rigs declined by 12 to 407, reaching a level not seen in four years for that component of the index. Gas rigs rose by 3 to 130, the highest gas rig count since July 2023. Baker Hughes released the report early because of the U.S. Thanksgiving holiday, and market participants regard the data as a closely watched short term indicator of potential changes in future U.S. production.

The contrasting moves in oil and gas drilling underline a longer running trend across the U.S. energy sector. Since the shale boom, producers have increasingly balanced growth ambitions with capital discipline. In recent years many companies have shifted the focus of free cash flow toward shareholder returns and debt reduction rather than aggressive expansions of drilling fleets. That strategic shift helps explain why a declining rig count does not automatically translate into sharply lower output in the short run. Productivity gains in well completions and higher initial production per rig have allowed overall output to remain resilient even as rig totals ebb.

Still, a sustained drop in active oil rigs reduces the pipeline of future supply coming online and can have implications for prices several months out. The weekly Baker Hughes count is a leading indicator for market watchers because wells typically take weeks to months to be completed and brought into full production. Lower drilling activity coupled with seasonal refinery maintenance and winter demand for distillates and heating fuels could tighten balances if international supplies do not compensate.

For the oilfield services sector and local communities that rely on drilling, fewer rigs generally mean reduced activity for drilling crews, equipment suppliers and service contractors. Employment and regional economic activity in key U.S. shale basins often move with rig counts, though the link has weakened as service firms have reorganized and automation has increased per rig productivity.

Policymakers and investors will watch coming weeks for whether the decline in oil rigs is temporary or marks a new plateau in U.S. drilling. If capital discipline persists, the industry may deliver steadier returns for shareholders while slowing the acceleration of U.S. crude output that once weighed on global prices. Conversely, an unexpected rise in crude prices or geopolitical shocks could prompt a rapid reversal as companies deploy rigs to capture higher margins.

The Baker Hughes snapshot for the week to November 26 therefore serves as a barometer both of current activity and of industry strategy heading into 2026. Observers will be monitoring rig trends alongside production data, inventories and price movements to assess how U.S. supply dynamics affect global energy markets.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?