When does medical debt survive death? What spouses need to know

Death can stop a bill, but not a collector's pressure. Spouses need to know when a debt belongs to the estate, and when it is not legally theirs at all.

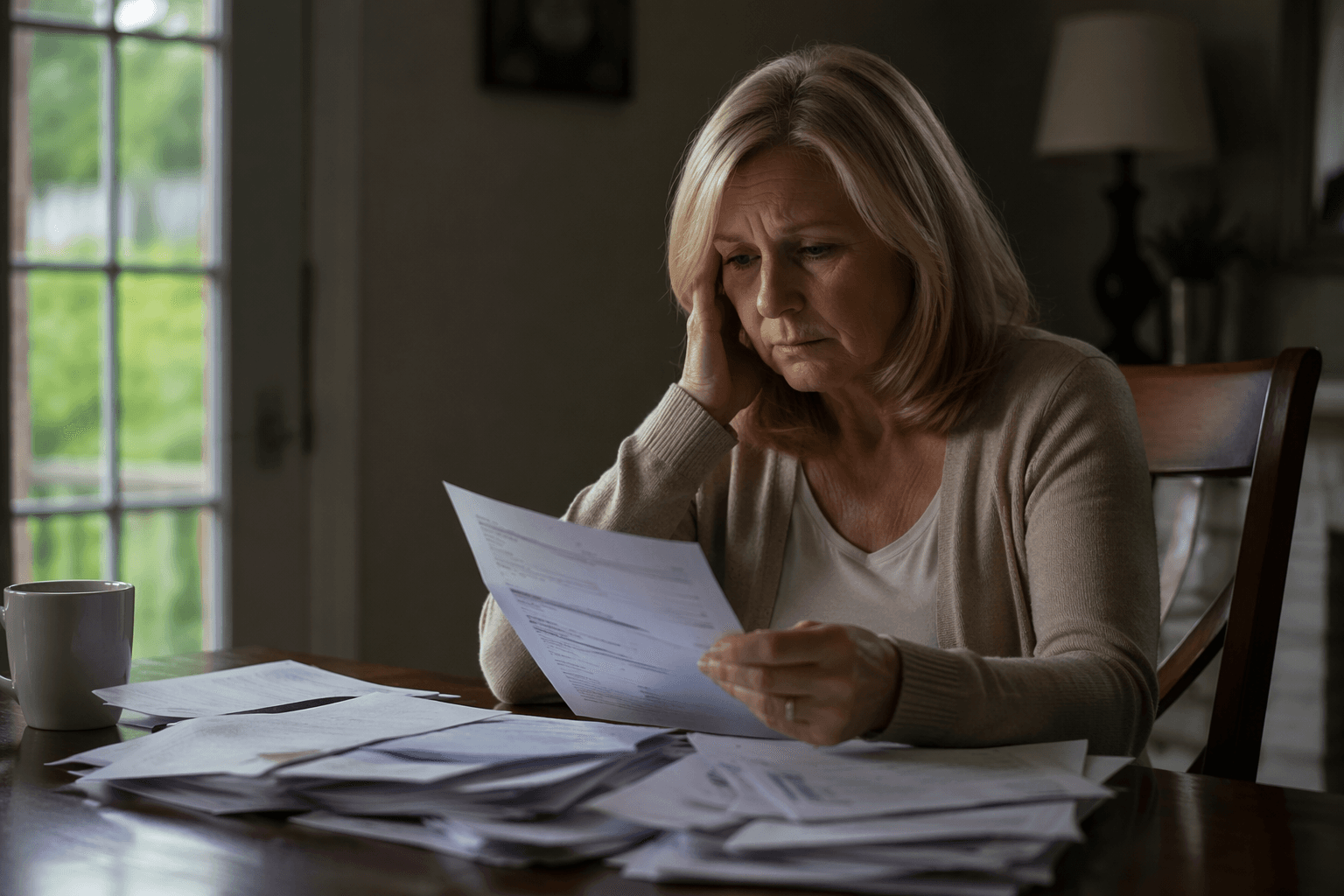

New surviving spouses with unpaid bills report an average of $28,749 in unpaid medical bills, compared with $15,785 among the rest of the population, CFPB data show. Death does not automatically make a spouse or adult child responsible for what was owed. In most cases, a deceased person’s money and property are supposed to be used first, and if there is no money or property in the estate, the debts usually go unpaid. Collectors may still push for payment even when the law does not make a survivor personally liable.

What debt usually does after someone dies

The basic rule is straightforward: debts are paid from the estate, not from the pockets of every relative who answers the phone. Survivors are generally not personally responsible for a deceased person’s debts unless they co-signed, hold a joint account, live in a community property state, or fall under another legal exception, such as a state necessaries statute for healthcare. Adult children are not automatically on the hook simply because they are children of the person who died.

A collection notice can arrive quickly after a death, but estate rules still control who may be pursued and what property can be reached. If the estate has no money or property, the debt usually remains unpaid rather than shifting to the nearest grieving relative.

Why surviving spouses get targeted

The Consumer Financial Protection Bureau has warned that medical debt collectors may improperly pressure surviving spouses to pay unpaid medical bills that are not legally owed. Its advisory opinion on medical debt collection, applicable on January 2, 2025, says that conduct may violate state or federal law.

In CFPB data, the deceased spouse’s out-of-pocket spending nearly doubled in the four years before death, while the survivor’s own spending declined, a pattern that suggests some of the bills may belong to the spouse who died rather than to the widow or widower being contacted.

Surviving spouses are often grieving and may be unfamiliar with probate and debt-collection rules, which makes them easier targets for collection tactics that rely on confusion instead of legal authority. For families under stress, the message can sound urgent even when the collector has not shown that the debt is actually enforceable against the survivor.

The Medicaid exception that can reach an estate

There is one major category families should not overlook: Medicaid estate recovery. Federal law requires states to seek recovery from a Medicaid enrollee’s estate for certain benefits, including nursing facility services, home and community-based services, and related hospital and prescription drug services for people age 55 and older.

The 1993 Omnibus Budget Reconciliation Act created that estate-recovery requirement. Many families think of Medicaid as a program that ends when the person dies, but some costs can still come back through the estate. KFF puts Medicaid enrollment at 67.7 million people in February 2026.

Estate recovery is different from ordinary consumer debt collection. It does not mean every bill survives death, and it does not mean every relative is liable. It does mean families dealing with Medicaid, probate, and a home or other assets should pay close attention to what claims are actually being filed against the estate and which ones are just collection pressure.

What to do if a medical bill arrives after a death

When a collector calls or a statement arrives, the first step is to separate emotion from liability. The law turns on whose debt it is, whose name is on the account, and what kind of property exists in the estate. A survivor should not assume that a call, a letter, or even repeated demands prove personal responsibility.

1. Ask which person the bill is legally attributed to and whether the collector is claiming against the estate or against you personally.

2. Check whether you co-signed, share a joint account, or live in a community property state, because those facts can change the answer.

3. Look for any Medicaid-related claim, especially if the person who died was 55 or older and received nursing facility, home and community-based, hospital, or prescription drug services.

4. Keep records of every call, letter, and payment demand, because collectors can cross the line when they pressure surviving spouses without legal authority.

If the answer turns on probate, the estate file matters. If the estate has no money or property, the general rule is that the debt usually goes unpaid. That is often the point collectors do not emphasize when they contact a widow, widower, or adult child.

Why the broader medical-debt problem keeps showing up in households like this

KFF estimates that people in the United States owe at least $220 billion in medical debt, and its health-care-debt survey found that four in ten adults have some form of health care debt.

Urban Institute research found that 1 in 20 consumers had unpaid medical debt in collections on their credit reports in 2023, even after major credit bureaus removed medical collections under $500. By August 2024, Urban estimated that figure had fallen to about 4.1 percent, or roughly 9.7 million consumers nationwide, and it found that medical debt is the most common form of debt in collections in the United States.

Urban found that Colorado’s 2023 law excluding all medical debt from credit reports was associated with a drop to zero in the share of people with debt in collections there.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?