Why Black homeownership remains far below White rates in every major U.S. city

Across the 50 largest metros, just 43.6% of Black householders own homes versus 70.3% of White householders, driven by income, credit and decades of discrimination.

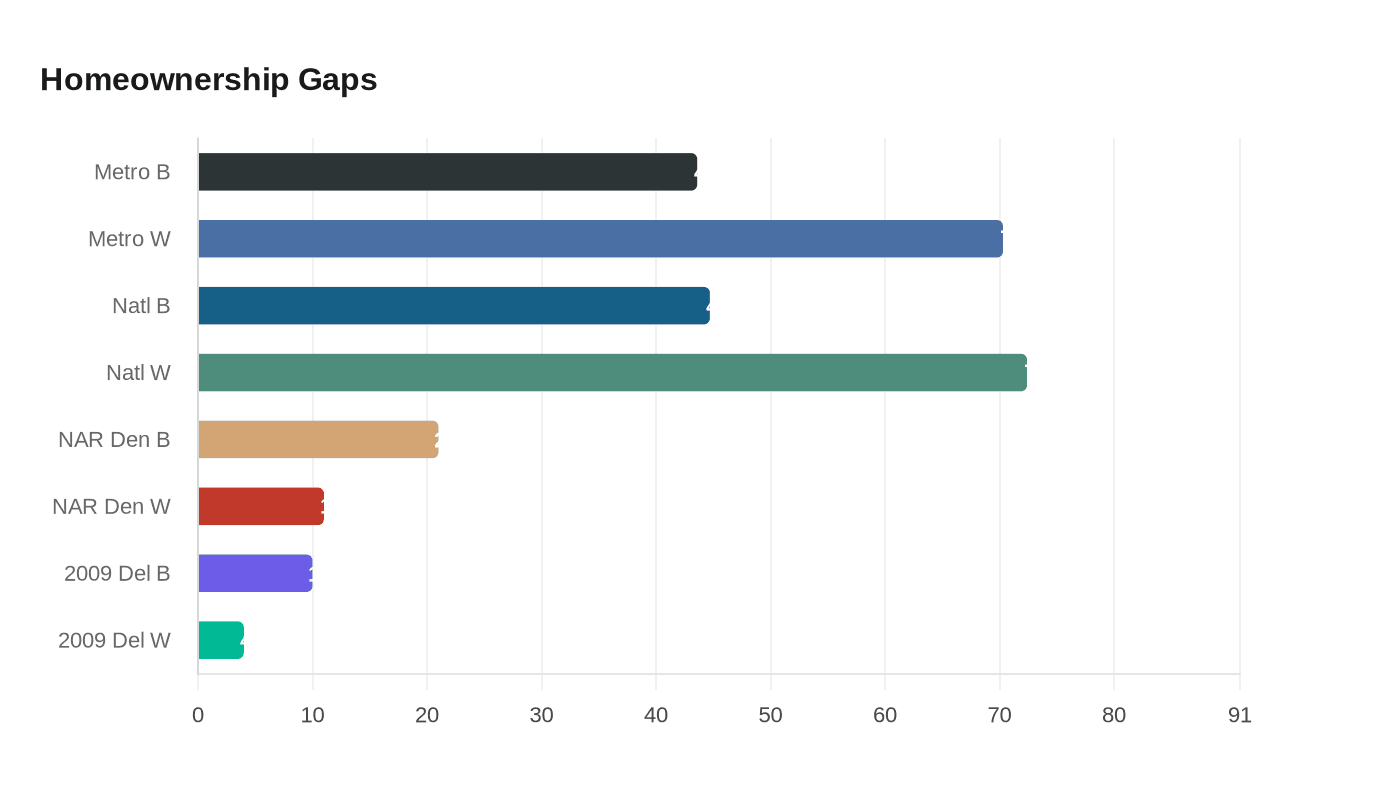

Across the 50 largest U.S. metropolitan areas, 43.6% of Black householders own homes compared with 70.3% of White householders, a gap that research shows is rooted in persistent economic disparities and long histories of exclusion. National snapshots echo the divide: the National Association of Realtors reports a 2023 Black homeownership rate of 44.7% versus 72.4% for White householders.

"Homeownership, which is so central to the American Dream, remains an unequal and financially frustrating experience for Black families," one source summarized. The numerical drivers are stark. LendingTree finds median household income in 2024 was $56,020 for Black households and $88,010 for White households, a $31,990 shortfall that shrinks the size of mortgages Black buyers can pursue. Matt Schulz, LendingTree's chief consumer finance analyst, said, "Without sufficient income and decent credit, getting a home can be a major challenge, and Black Americans still trail well behind white Americans and other groups in those areas." He added, "That combination of lower income and lower credit scores almost certainly lowers the ceiling on the size of mortgages that they are able to get."

Credit gaps and denial rates compound the income shortfall. Average credit scores cited in recent analyses run about 627 for Black applicants versus 727 for White applicants, below the 670 threshold commonly defined as good credit. Mortgage denial rates track that gap: Ballardbrief reported a nationwide Black denial rate twice that of Whites, 24% versus 12%, while NAR data for 2023 shows Black applicants denied at 21% versus 11% for White applicants. Those higher denial rates cut off pathways to purchase and to build home equity.

The housing market crash of 2007 to 2009 amplified these differences. Black homeowners were more likely to have carried subprime loans into the crisis, producing higher foreclosure and delinquency rates and deeper equity losses: delinquency in 2009 affected about one in 10 Black homeowners versus one in 25 White homeowners, and Ballardbrief records home equity declines from 2007 to 2009 of 12% for Black households versus 9% for White households. Local analyses show the effects are uneven but durable. The Federal Reserve Bank of Philadelphia found the city’s Black homeownership rate has fallen over recent decades and that the local gap was slightly wider in 2019 than it was 30 years earlier.

Discrimination and ancillary costs remain material barriers. NAR’s 2023 snapshot reports Black buyers were the most likely to report discrimination during the transaction, with 47% saying they experienced some mistreatment and 5% reporting race-based discrimination. Black homeowners also face higher housing cost burdens in 39 states and pay marginally higher median homeowners insurance in 2023, at $1,360 versus $1,310 for White homeowners.

Local dynamics matter. Analyses using American Community Survey data show the Black-White homeownership gap can be larger in smaller and midsize cities than in large metros, and migration patterns since the 2010s have shifted where gaps widen or narrow. Researchers point to enduring structural causes: redlining, racial steering, predatory lending and unequal credit access.

For markets and policy, the implications are clear. The persistent gap depresses Black household wealth, narrows housing market demand, and concentrates risk in neighborhoods that weather downturns worse. LocalHousingSolutions notes opportunities for cities to help households of color not only purchase homes but also stay in them. Closing the gap will require coordinated action on credit access, affordable mortgage products, stronger enforcement of fair lending and targeted support for repairs and insurance costs so that ownership translates into stable wealth creation.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?